Downloaded 90 times

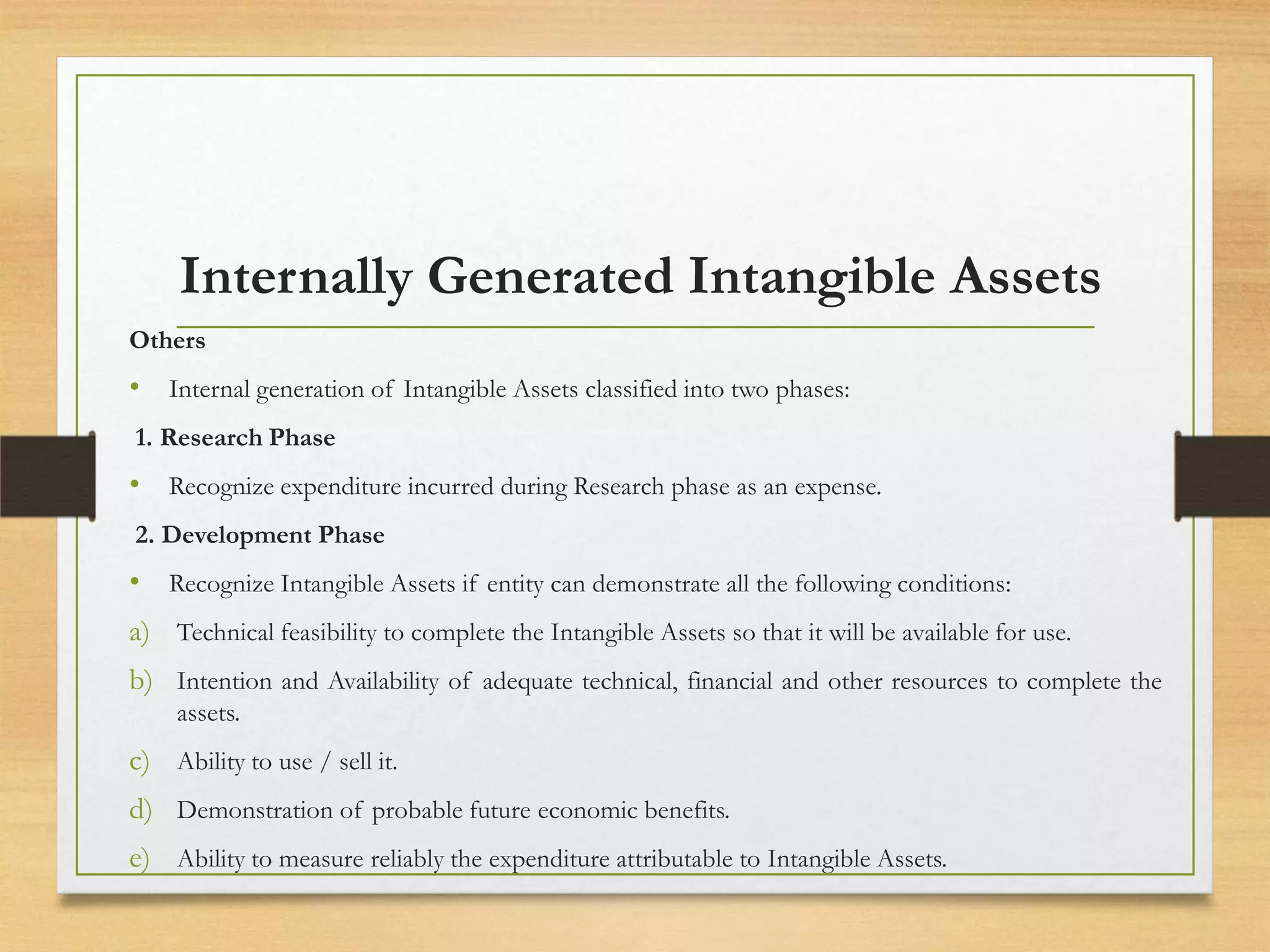

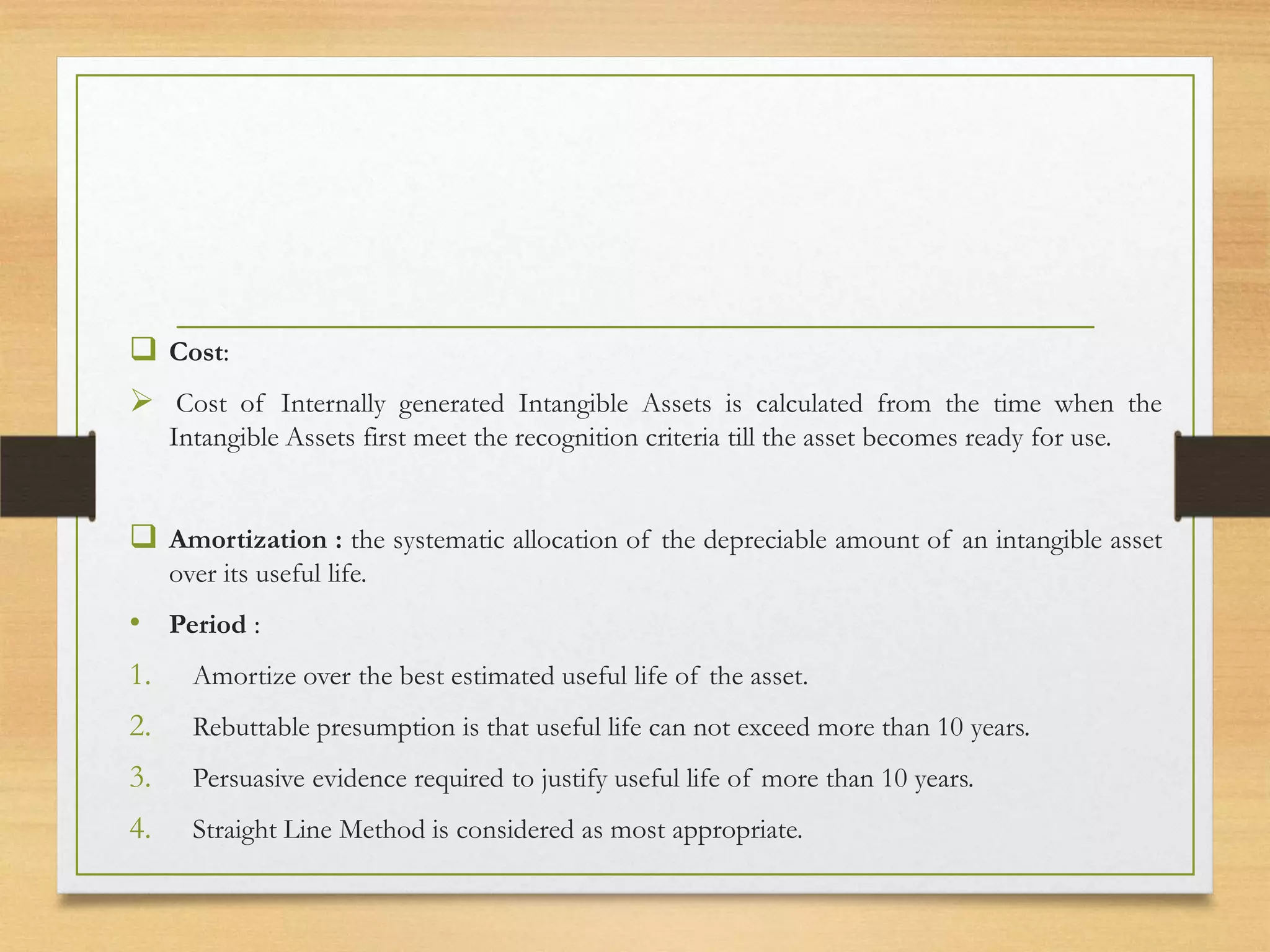

This document outlines Accounting Standard 26 regarding the accounting treatment for intangible assets in India. Key points include: - The standard defines intangible assets and provides examples such as goodwill, research and development expenses, patents, and copyrights. - Intangible assets must meet certain recognition criteria to be recorded, including being identifiable, lacking physical substance, and providing future economic benefits. - Internally generated intangible assets are classified as research or development phases, with development costs capitalized if certain conditions are met. - Intangible assets are initially measured at cost and amortized over their estimated useful lives not to exceed 10 years, generally using the straight-line method.

![Brennan, Niamh and Connell, Brenda [2000] Intellectual Capital: Current Issue...](https://cdn.slidesharecdn.com/ss_thumbnails/0410brennanconnellintellectualcapitalcurrentissuesandpolicyimplications-121116102513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)