INTANGIBLE

ASSETS – What

itis?

An intangible asset is an asset that is not physical in

nature, such as a patent, brand, trademark, or

copyright and Goodwill.

Businesses can create or acquire intangible assets.

An intangible asset can be considered indefinite (a

brand name, for example) or definite, like a legal

agreement or contract.

Since intangible assets have no shape or form, they

cannot be held or manipulated.

3.

Types of IntangibleAssets

Intangible asset is one that

has no physical form.

These assets are generally

considered long-term whose

value increases over time

and very critical to the long-

term success of the business.

INTANGIBLE ASSETS CAN BE

CLASSIFIED INTO TWO TYPES.

Indefinite: This type of

intangible asset stays with

the holder as long as it

continues to operate, such

as a brand name.

Definite: This type is restricted

to a limited time. A legal

agreement to operate under

another company's patent

with no plans of extending

the agreement is considered

a definite intangible asset.

4.

Types of

Intangible

Assets

Themost common types of intangible

assets—notably

brands, goodwill, and intellectual

property.

Brands

The brand is something that sets one

business apart from another.

This may come in the form of a logo,

symbol, or brand name.

Businesses commonly use marketing,

design techniques, and advertising to

come up with their brands.

This allows consumers to easily identify a

particular company.

Example: most people can easily identify

Apple (AAPL) just by seeing its logo.

5.

Types of IntangibleAssets

Goodwill

When one company purchases another, the intangible assets associated

with that transaction are considered goodwill.

When a company acquires another business, any amount that exceeds the

fair value of the target's net assets represents its goodwill.

If the amount is above the target’s book value then it results in positive

goodwill.

Anything below book value is negative goodwill.

6.

Types of IntangibleAssets

Intellectual property is a type of intangible asset that is legally protected.

This means it cannot be used by another business or individual unless authorized by

the owner.

Common forms of intellectual property include

Copy Rights.

Digital Assets.

Franchises.

Patents

Trade Marks

Trade Secrets.

7.

Valuation of IntangibleAssets

Need for Valuing Intangible Assets:

Many companies do not understand that their trademarks, designs and

other intangible property rights and assets are often more valuable than, for

example, their inventories.

It is not uncommon for a company’s intangible assets to be their single most

valuable asset and can be used to ensure financing of the company's

growth.

8.

Valuation of IntangibleAssets

valuation may become necessary when:

• You plan to license out an intangible asset and you want to get an estimate

of future license fees

• You plan to buy or sell a business. A valuation of the intangible assets can

then be helpful in achieving a better price.

• Getting an accurate valuation of your intangible assets is not always easy.

• How much is a trademark worth after years of marketing?

9.

Valuation of IntangibleAssets

Does your patent protect a technical solution where there is a good market

basis or is the invention superfluous?

A well-known trademark or a strong patent can be the true core of a

company.

All intangible assets are not valuable? If they do not help to create, maintain,

or increase cash flow, they may not have direct value.

The value of your assets may also change over time. For example, a patent

can protect a unique solution, but after some time other solutions may arise

that reduce the value of your patent.

10.

Valuation of IntangibleAssets

Trademarks generally increase in value the more well-known they become.

The value of intangible property rights depends on the circumstances of a

given time and place. It is important to analyze the intangible property right

based on its use, the market and competitors.

The valuation of intangible property rights is very important. A valuation

indicates whether a right is necessary or not

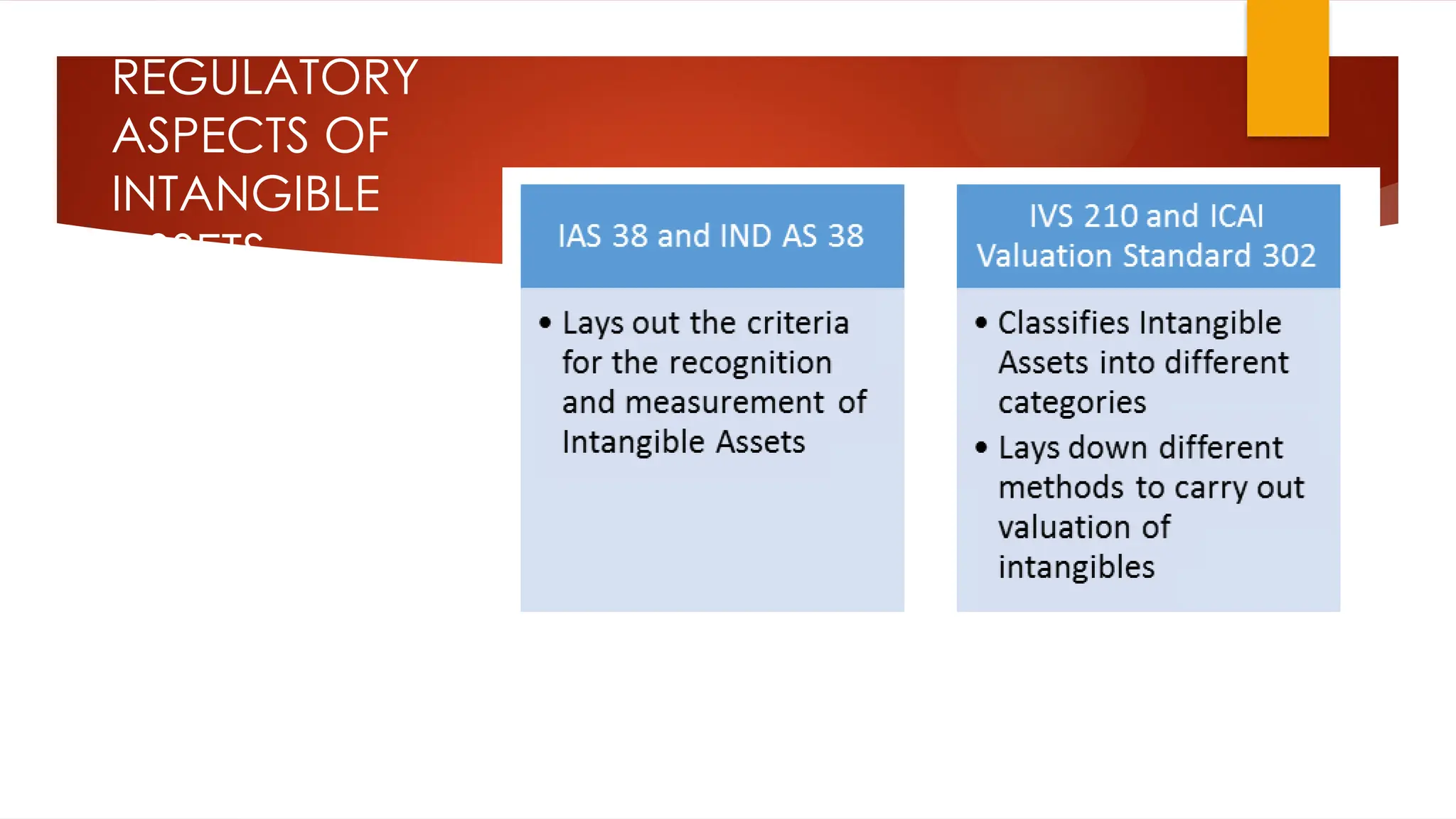

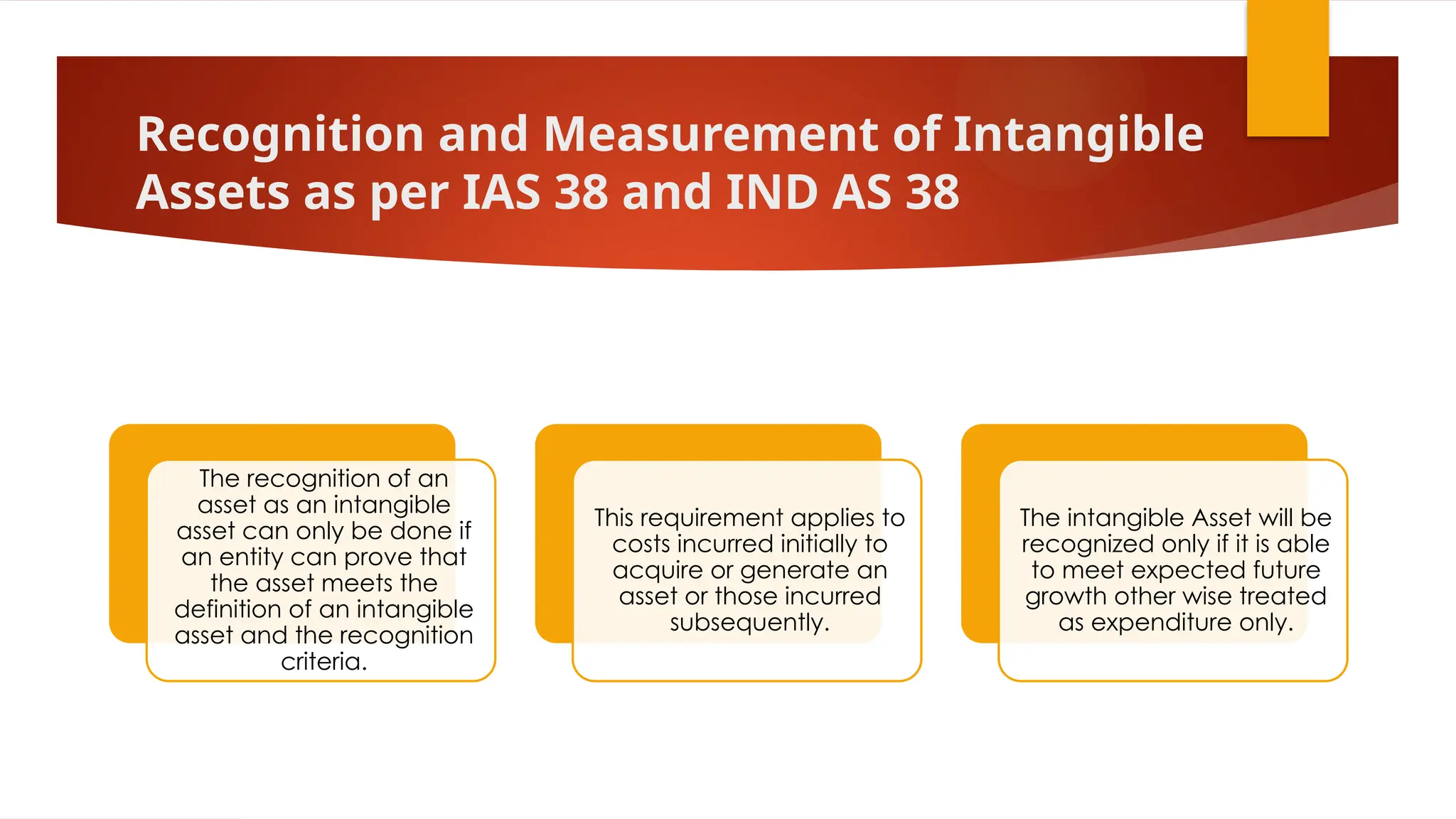

Recognition and Measurementof Intangible

Assets as per IAS 38 and IND AS 38

The recognition of an

asset as an intangible

asset can only be done if

an entity can prove that

the asset meets the

definition of an intangible

asset and the recognition

criteria.

This requirement applies to

costs incurred initially to

acquire or generate an

asset or those incurred

subsequently.

The intangible Asset will be

recognized only if it is able

to meet expected future

growth other wise treated

as expenditure only.

13.

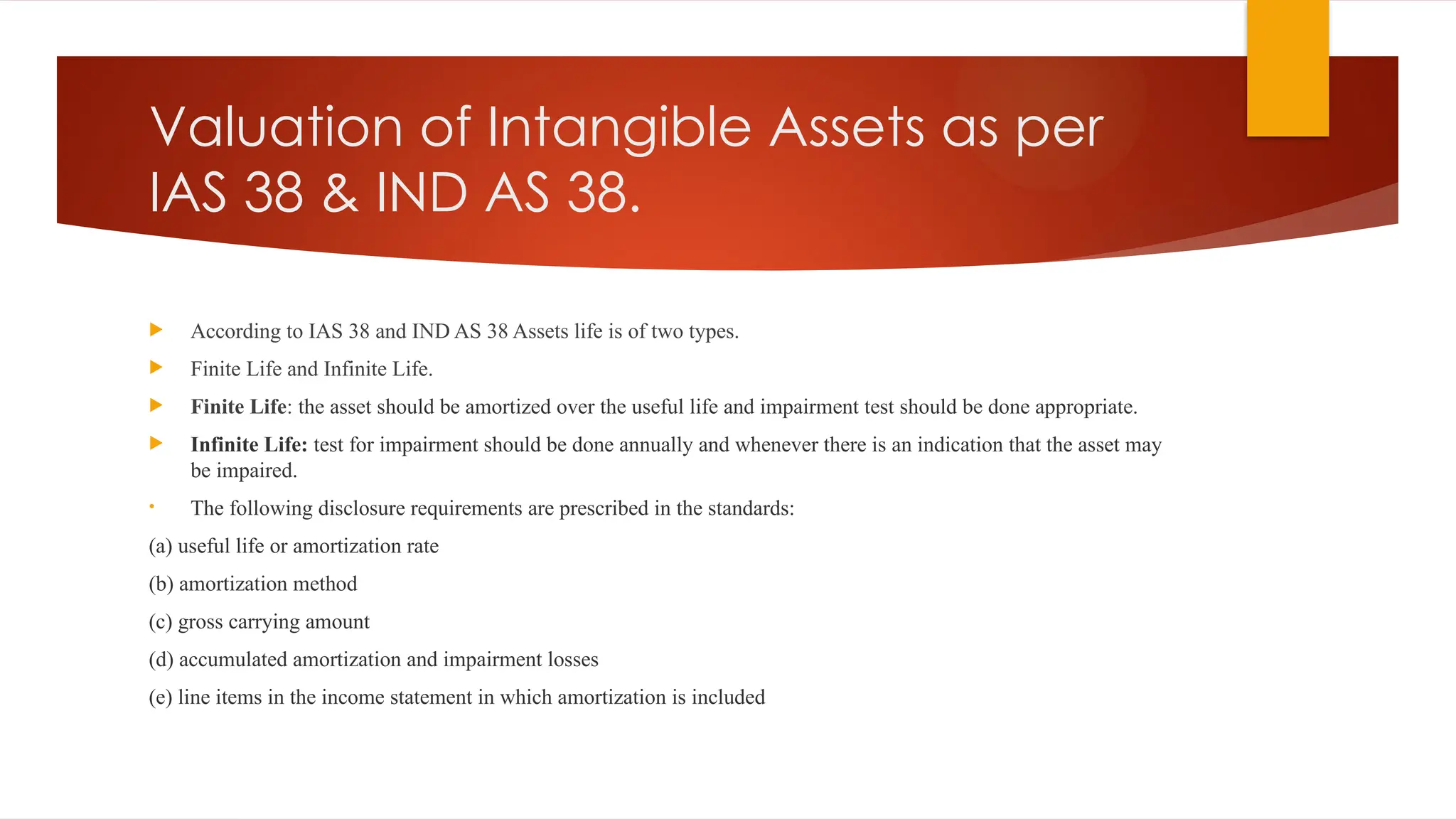

Valuation of IntangibleAssets as per

IAS 38 & IND AS 38.

According to IAS 38 and IND AS 38 Assets life is of two types.

Finite Life and Infinite Life.

Finite Life: the asset should be amortized over the useful life and impairment test should be done appropriate.

Infinite Life: test for impairment should be done annually and whenever there is an indication that the asset may

be impaired.

• The following disclosure requirements are prescribed in the standards:

(a) useful life or amortization rate

(b) amortization method

(c) gross carrying amount

(d) accumulated amortization and impairment losses

(e) line items in the income statement in which amortization is included

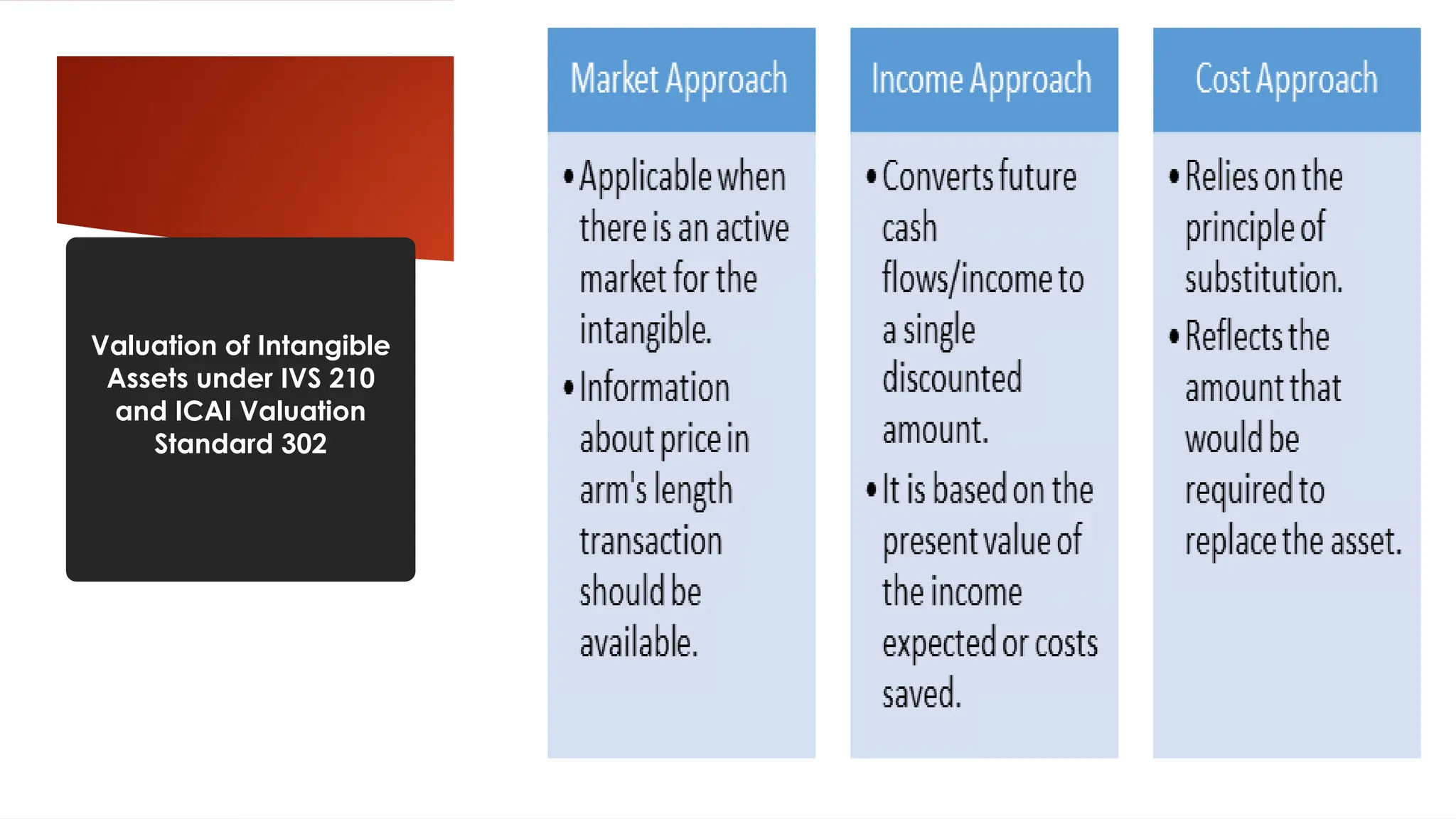

1. The CostApproach

A valuation according to this method is based on the costs required to

create an intangible asset

(or)

what it might cost to recreate or develop a similar product or service.

The method does not consider the current economic value of a product.

16.

1. The CostApproach

Common costs tend to be:

Labour, Material & Equipment, R&D, Development of prototype , Tests ,

Regulatory approvals, Application , Registration and granting of intangible

property rights.

This method assumes that a potential buyer can avoid these costs by

purchasing the intangible asset.

17.

Advantages of CostApproach

Time: By purchasing the asset, the buyer can avoid wasting time on research

and development.

Expenses: Should the buyer instead try to develop their own technology, the

buyer would need to spend at least this much.

Success: A buyer may not have succeeded in developing their own

technology.

Protection: A buyer may not be able to protect their own technology and

may also risk infringing on the rights of others.

This method is suitable for the business who are in the early stages.

18.

Draw backs ofCost Approach

Market potential of a business cannot be fully weighted , since focus is on

cost rather than profit.

This method does not consider future value and therefore a parameter on

which valuation is traditionally based is lost.

19.

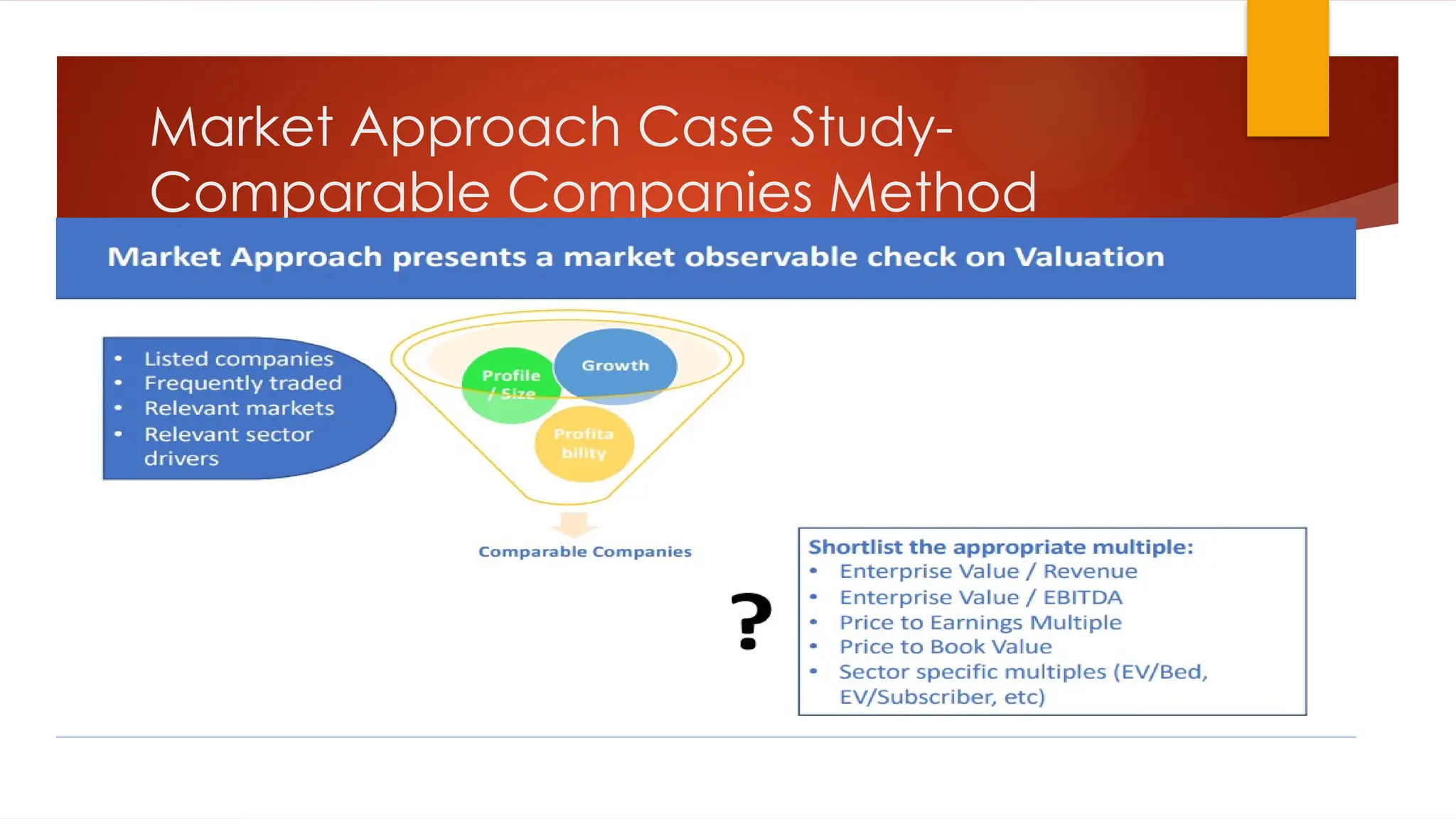

2. The MarketValue Approach

Basing the valuation of a product based on its performance on the market

can be a good approach when valuing intangible assets and rights.

Market valuation of intangible assets provides a good estimate of the value.

The problem with this method is that it can be difficult to find published

information on transfers of intangible property and rights, as they are often

confidential.

There are few transfers that are similar enough to provide a good

comparison.

20.

The Market ValueApproach

It is unlikely that this method would be used to evaluate patents. The value

of a patent is largely based on the uniqueness of the patent and therefore

comparable information is unlikely to be found.

Despite the difficulties, this method is objective and can provide companies

with a realistic analysis of the value of an intangible asset for both the

holder and the buyer.

21.

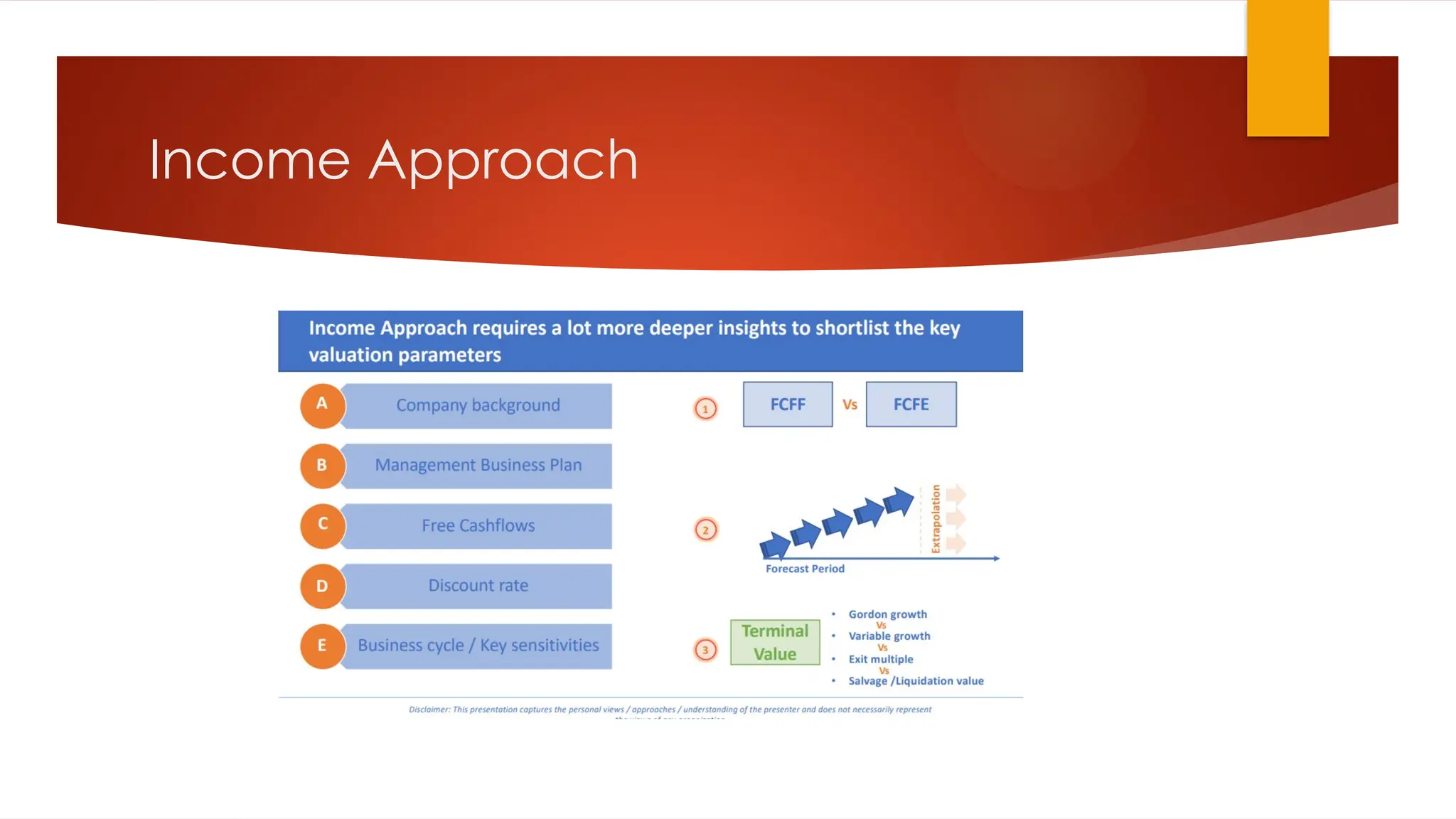

3.The Income Approach

This method focuses on the income that an intangible asset may generate in

the future.

The method considers both future income, which the right can generate

during its lifetime, as well as the costs of this.

Risk and financial costs are also factors that have an impact. The result of

this analysis is called "Net Present Value" or NPV.

This method of valuing intangible assets gives a potential buyer the

opportunity to consider an investment based on whether the NPV valuation

is positive or negative.

22.

The Income Approach

How ever it should be noted that Income or Economic Benefit method is

only an assessment of likely future events rather than actual outcomes.

Draw backs of Income Methods are

• It is difficult to estimate the economic life cycle of intangible assets.

• It is difficult to estimate income for years to come.

• Factors such as the strength of the intangible asset, the size of the potential

market, competition, changes in the economic climate and the cost of

registration and depending oneself against infringements of the right must

be considered.

23.

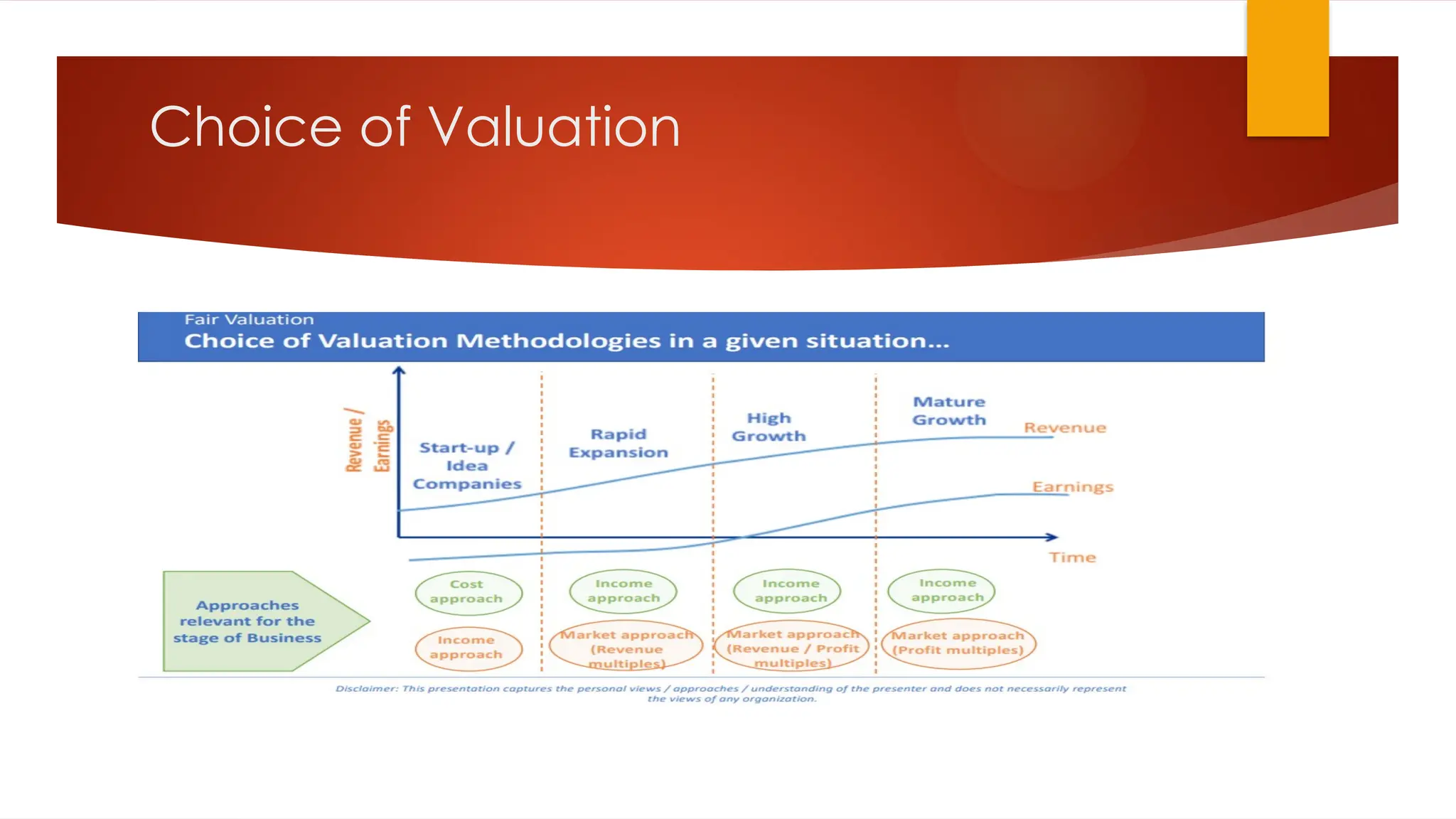

Valuation of IntangibleAssets

Owing to the unique nature of intangibles, the questions of how to value

intangible assets ultimately comes down to choosing the right method for

valuation.

The five primary valuation methods are based on the three approaches

described above – the market, income and cost approaches. While valuing a

particular intangible asset, one method will likely be more appropriate

compared to the others.

24.

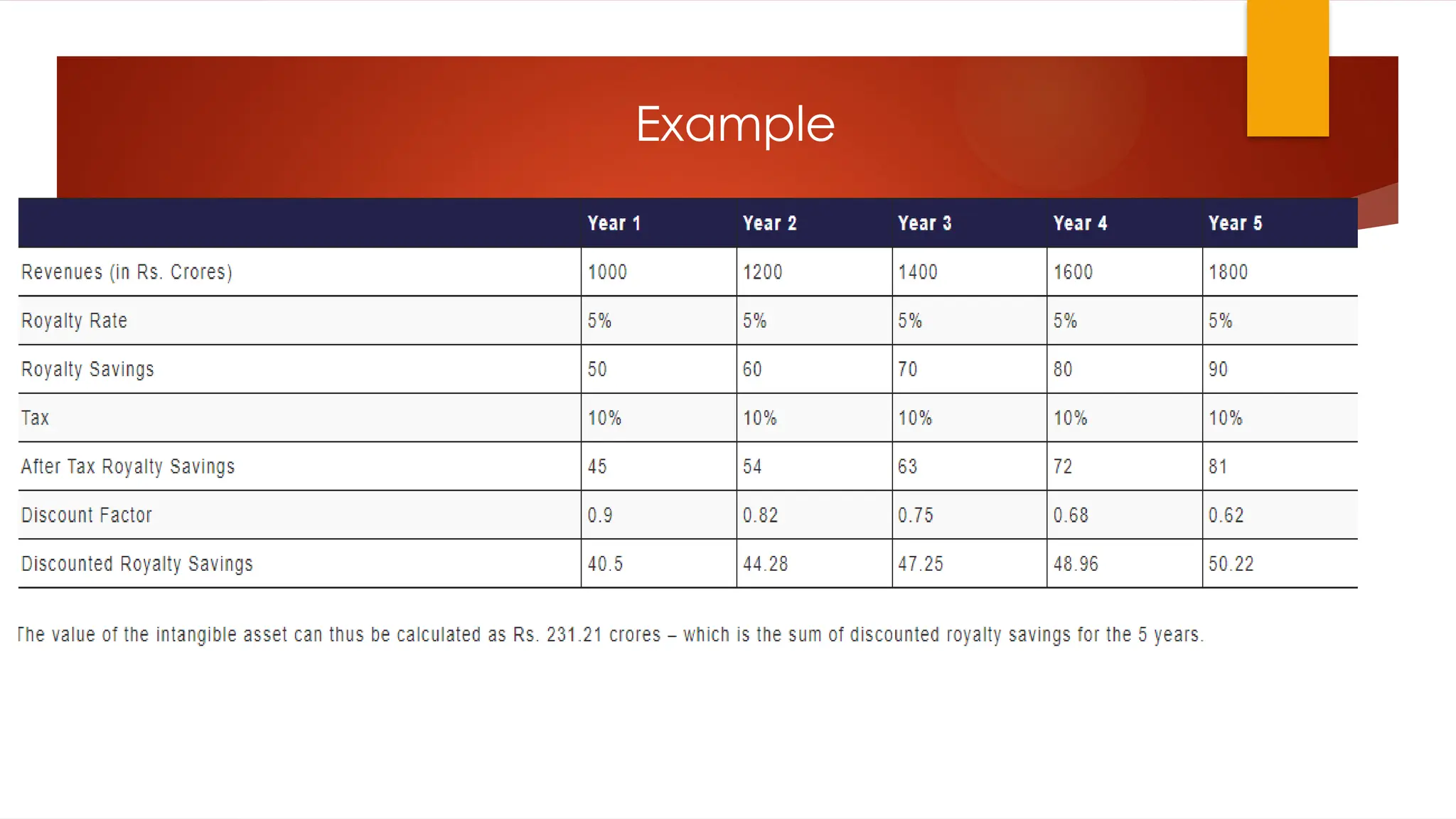

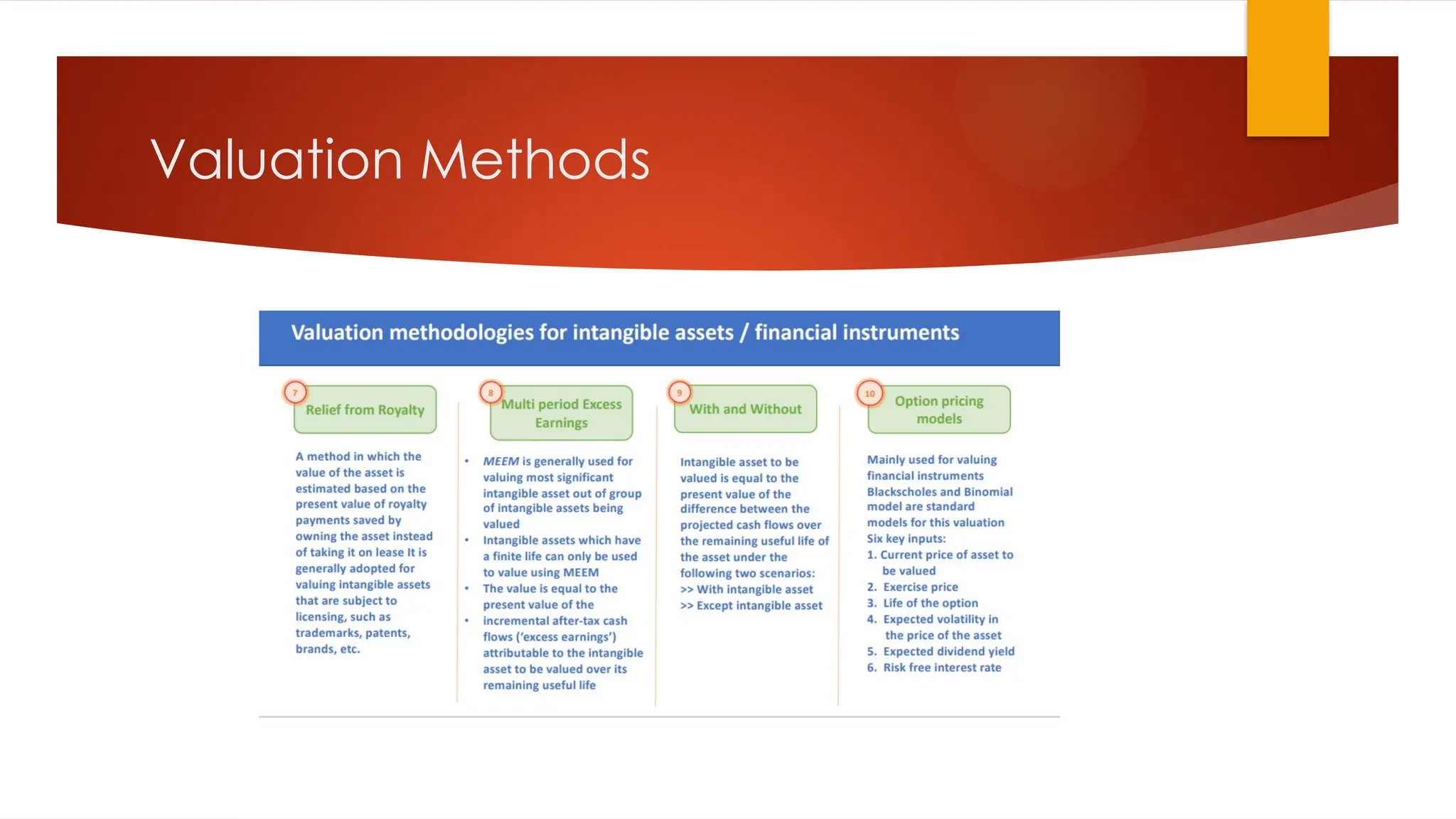

1) Relief

from

Royalty

Method

(RRM)

In thismethod, value is assigned to the

intangible asset based on approximate

royalty rates that would be saved by

owning the asset.

Because the asset is owned by the

Company, it doesn’t have to pay for the

use of the asset.

The RRM incorporates elements of both

the market (royalty rates for comparable

assets) and income (estimates of

revenue, growth, tax rates) approaches.

2) With andWithout Method (WWM)

The intangible asset’s value is determined by calculating the difference

between a discounted cash flow model for the enterprise with the asset and

a discounted cash flow model without the asset.

It should be noted that identification of incremental income and incremental

risk to business cost of capital excluding the capital is of paramount

importance here.

27.

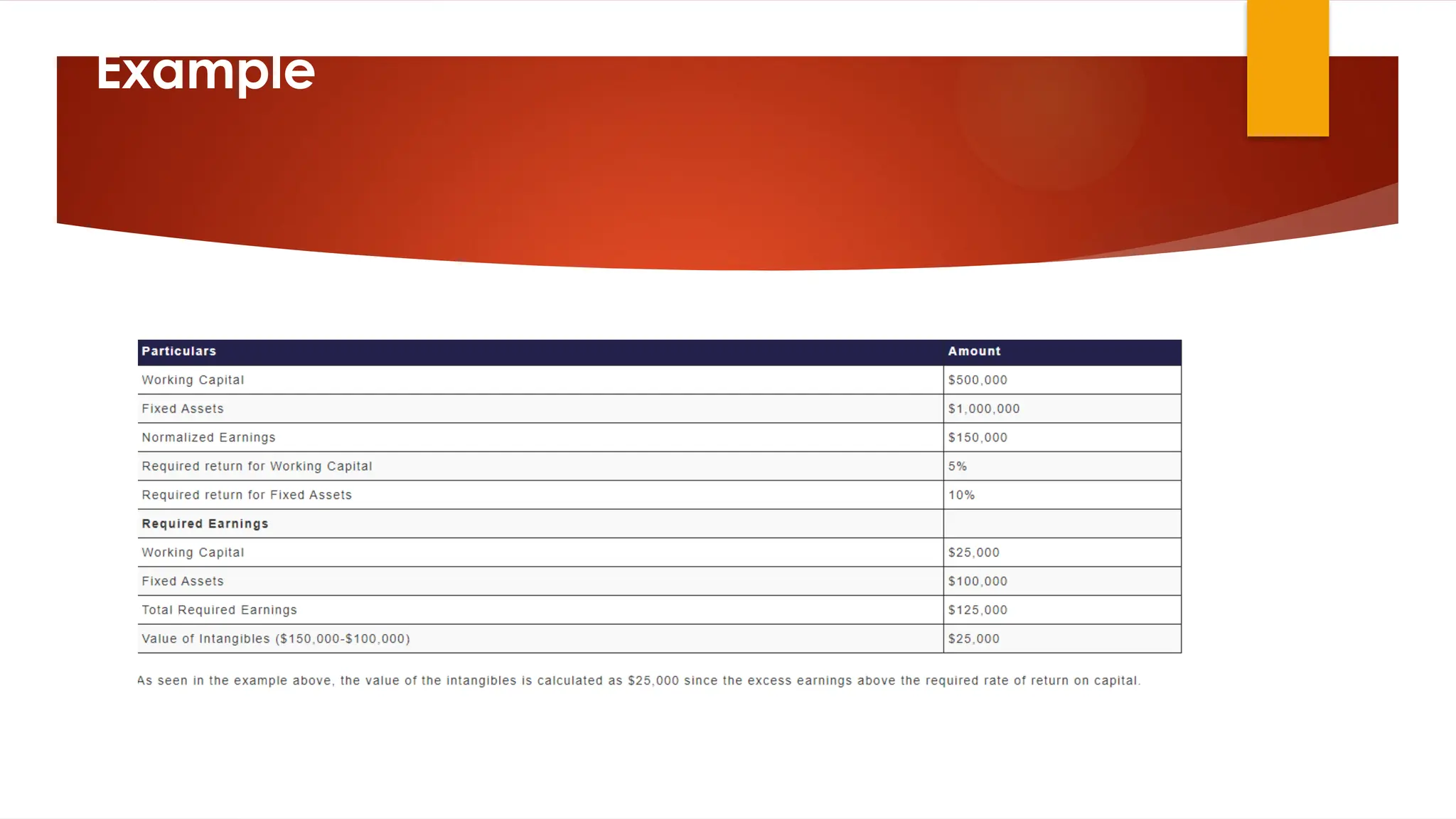

3) Multi-Period ExcessEarnings

Method (MPEEM)

The cash flows related to a particular intangible asset are discounted to

calculate the present value.

It is applied when the cash flows associated to a particular intangible asset

can be properly determined.

Software and customer relationships are examples of assets that can be

valued using MPEEM.

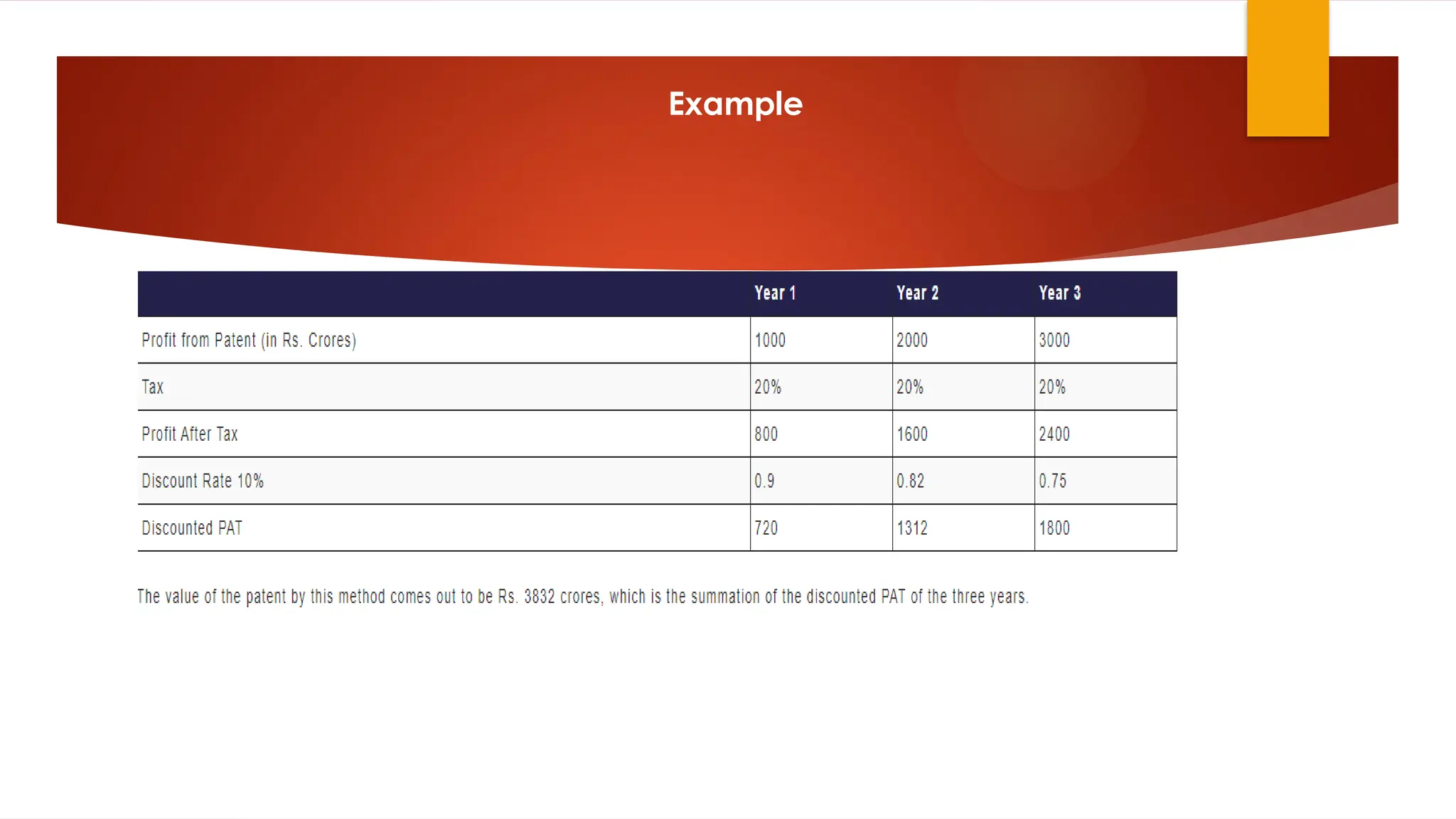

4) Real OptionPricing

This method is used to value intangible assets that are not presently

generating cash flows but are expected to do so in the future.

Undeveloped patent options are one example of an intangible asset that

may be valued using this method.

5) Replacement

Cost Method

Less

Obsolescence

The replacement cost method establishes

a value for the intangible based on the

amount is would cost the Company to

replace the asset.

Despite of all the guidance and standards

available for intangible valuations,

Intangible Valuations tends to be a highly

subjective activity.

The evolution and evaluation of the

intangible assets of a company is an

integral part of the analysis of a

company.

32.

Conclusion

Many technologyand service-based companies are heavily reliant on

intangible assets while performing their business functions, thereby giving

them immense importance currently.

The real challenge in intangible valuations lies in determining how much

portion of value is attributable to several tangible and intangible assets.

Therefore, it should be noted that the value is within the prescribed

framework under law while exercising structured and practical thinking in

relation to the benefit that can be derived from intangibles.

It is of no doubt that going forward, Companies that can accumulate and

harness Intangibles will be able to create more value.

![Brennan, Niamh and Connell, Brenda [2000] Intellectual Capital: Current Issue...](https://cdn.slidesharecdn.com/ss_thumbnails/0410brennanconnellintellectualcapitalcurrentissuesandpolicyimplications-121116102513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)