Downloaded 87 times

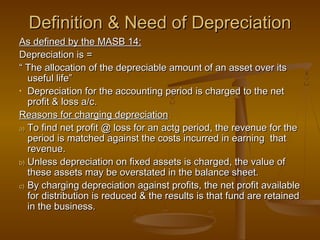

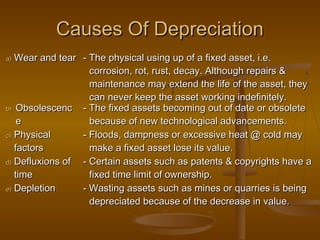

This chapter discusses depreciation of fixed assets, capital expenditures, and revenue expenditures. It defines depreciation and explains the need for and causes of depreciation. It also covers how to calculate and account for depreciation using different methods. The chapter distinguishes between capital expenditures, which increase asset value, and revenue expenditures, which are daily operating expenses. It explains how incorrectly treating expenditures can affect financial statements.