Download as PDF, PPTX

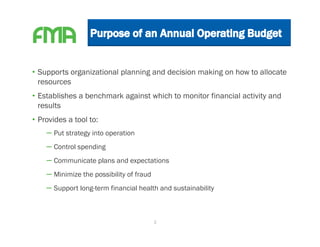

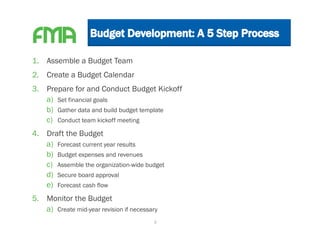

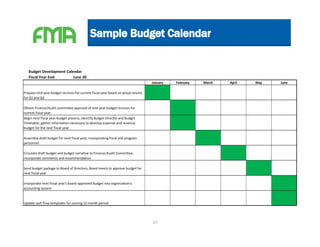

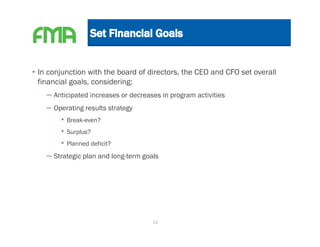

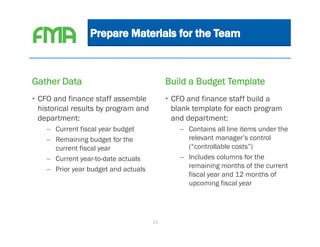

The document outlines a 5-step guide for developing an organizational budget: 1) Assemble a budget team, 2) Create a budget calendar, 3) Prepare for and conduct a budget kickoff meeting, 4) Draft the budget, and 5) Monitor the budget. It emphasizes a team decision-making approach and provides details for each step such as setting financial goals, building a budget template, forecasting expenses and revenues, monitoring variances, and creating mid-year revisions when needed. The overall process aims to support strategic planning, control spending, and ensure long-term financial sustainability.