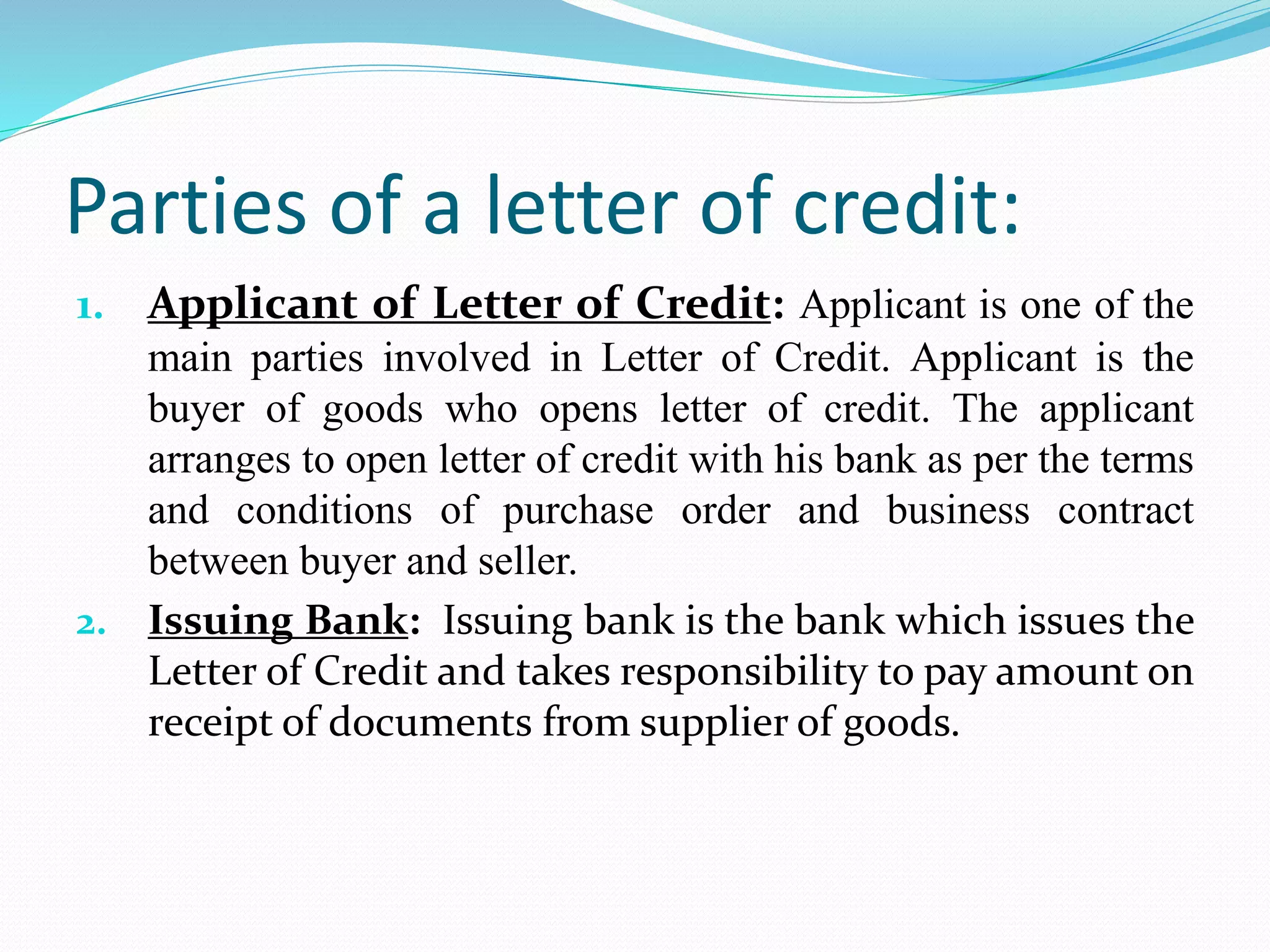

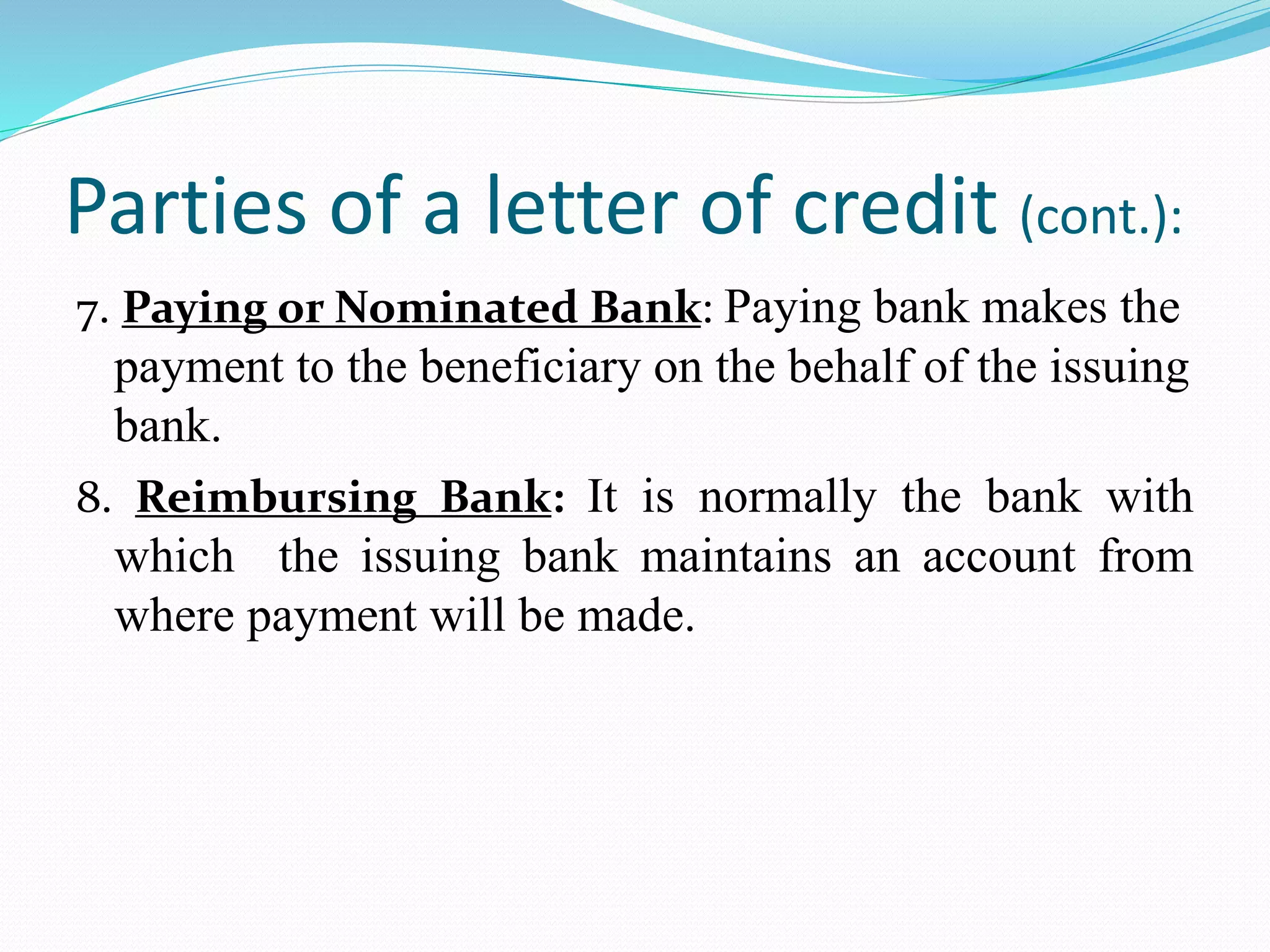

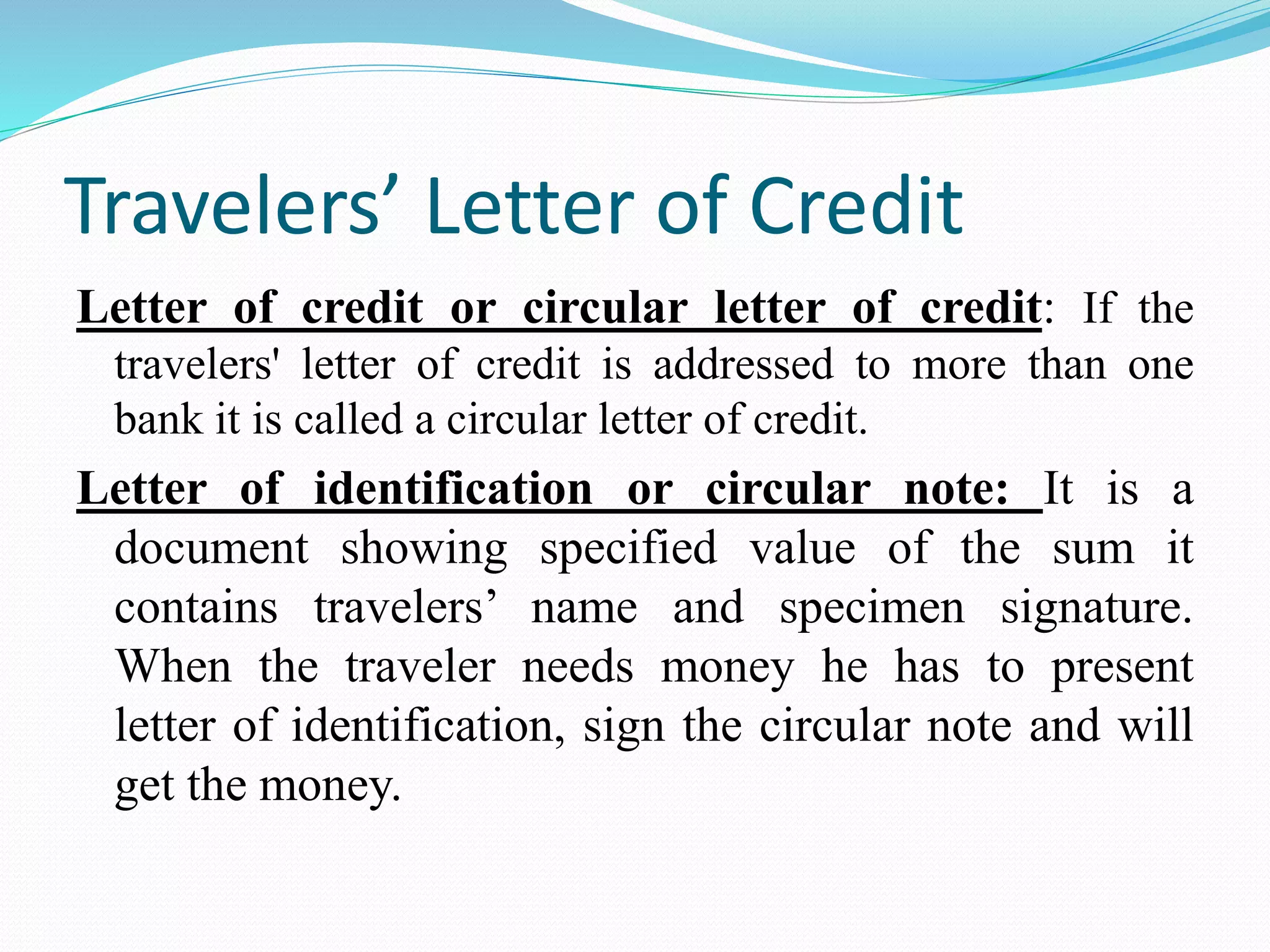

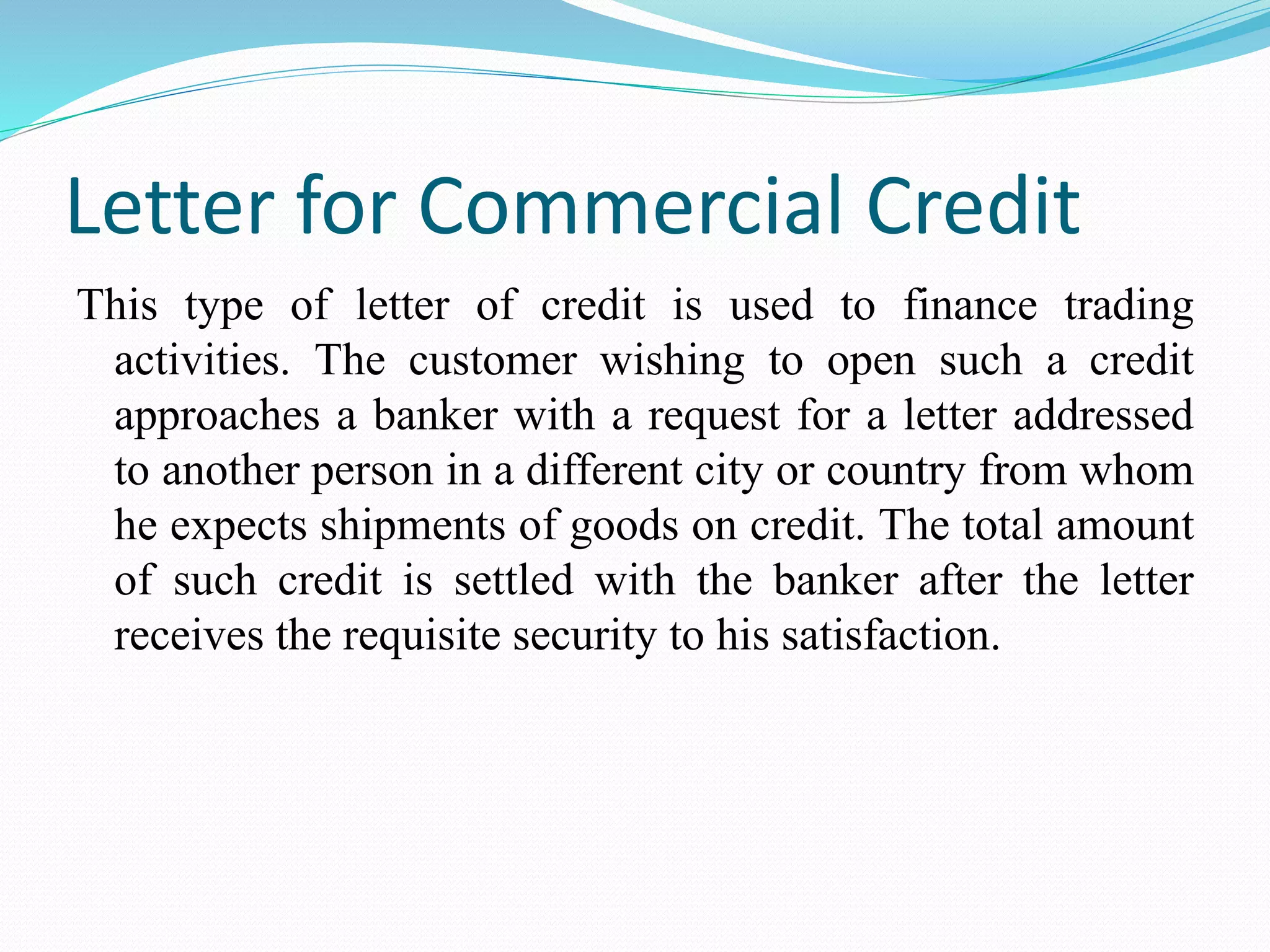

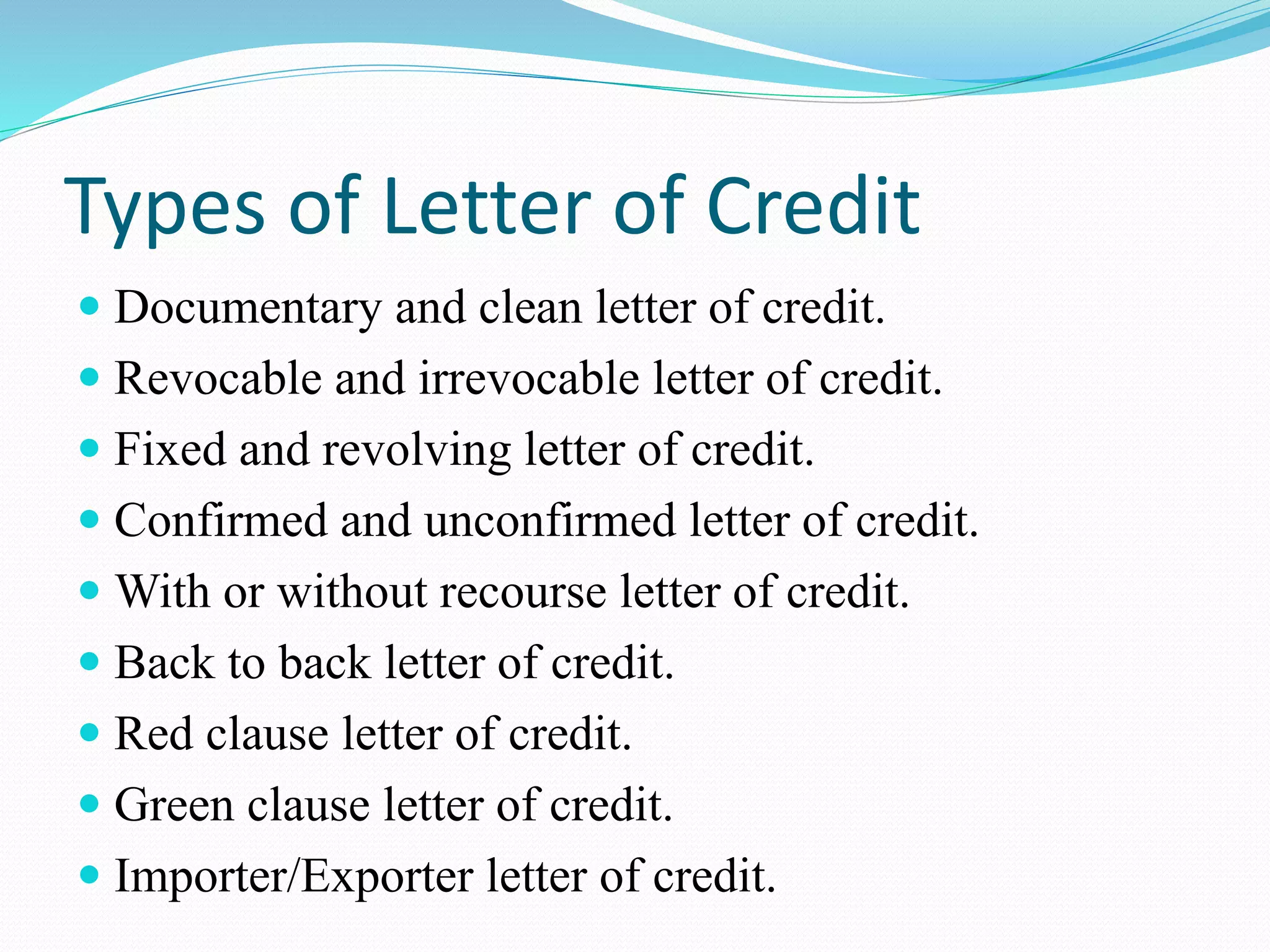

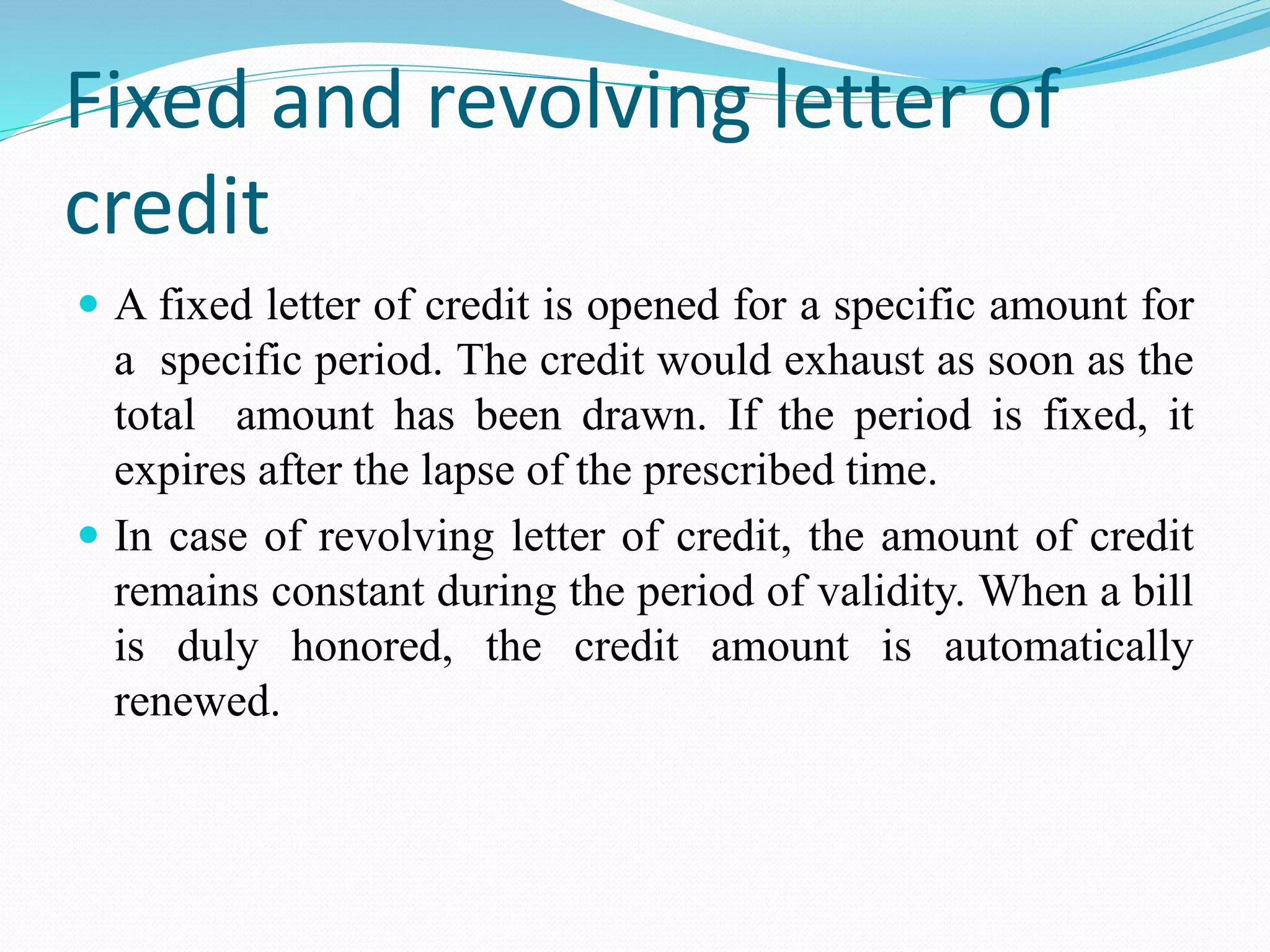

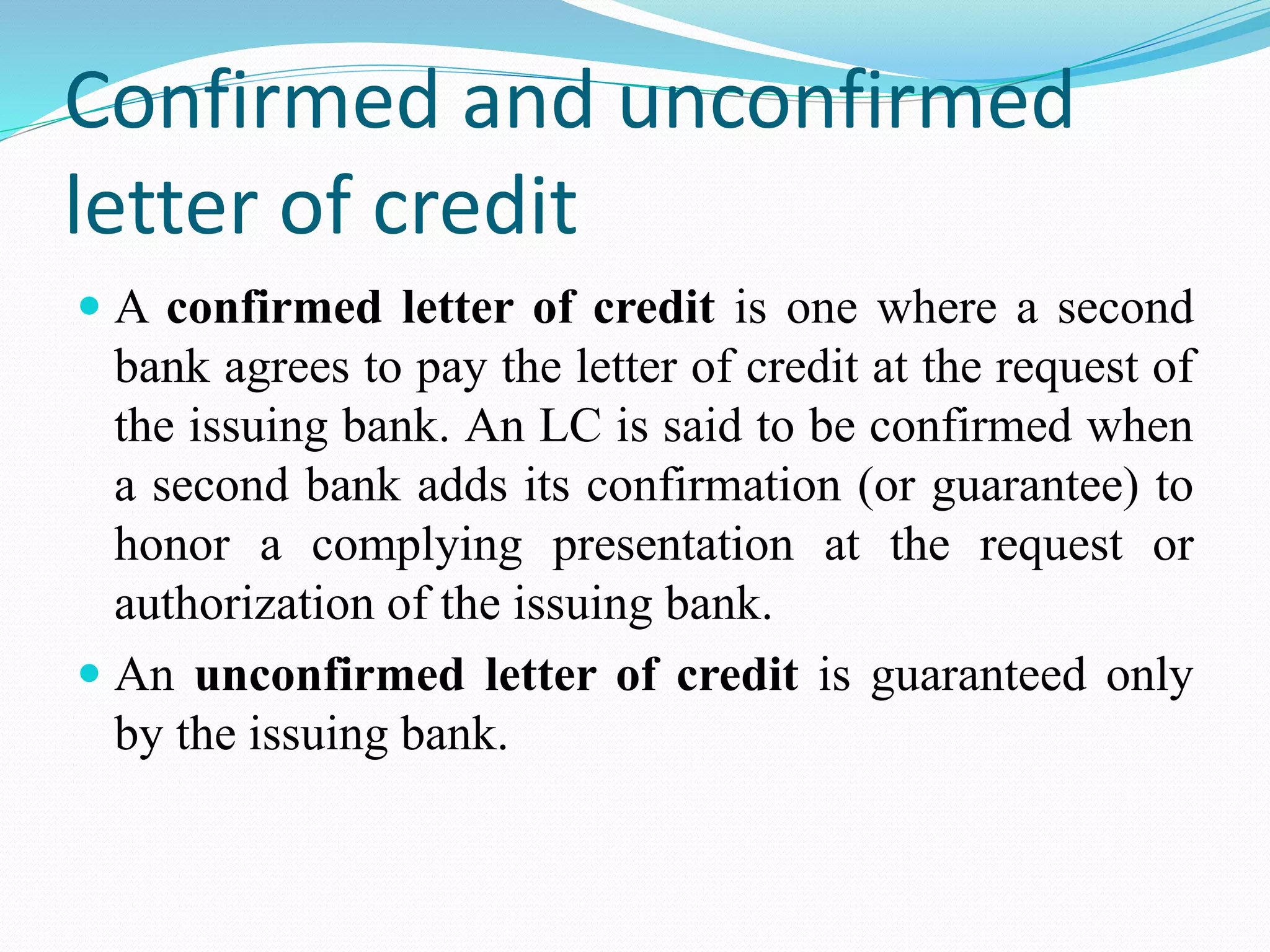

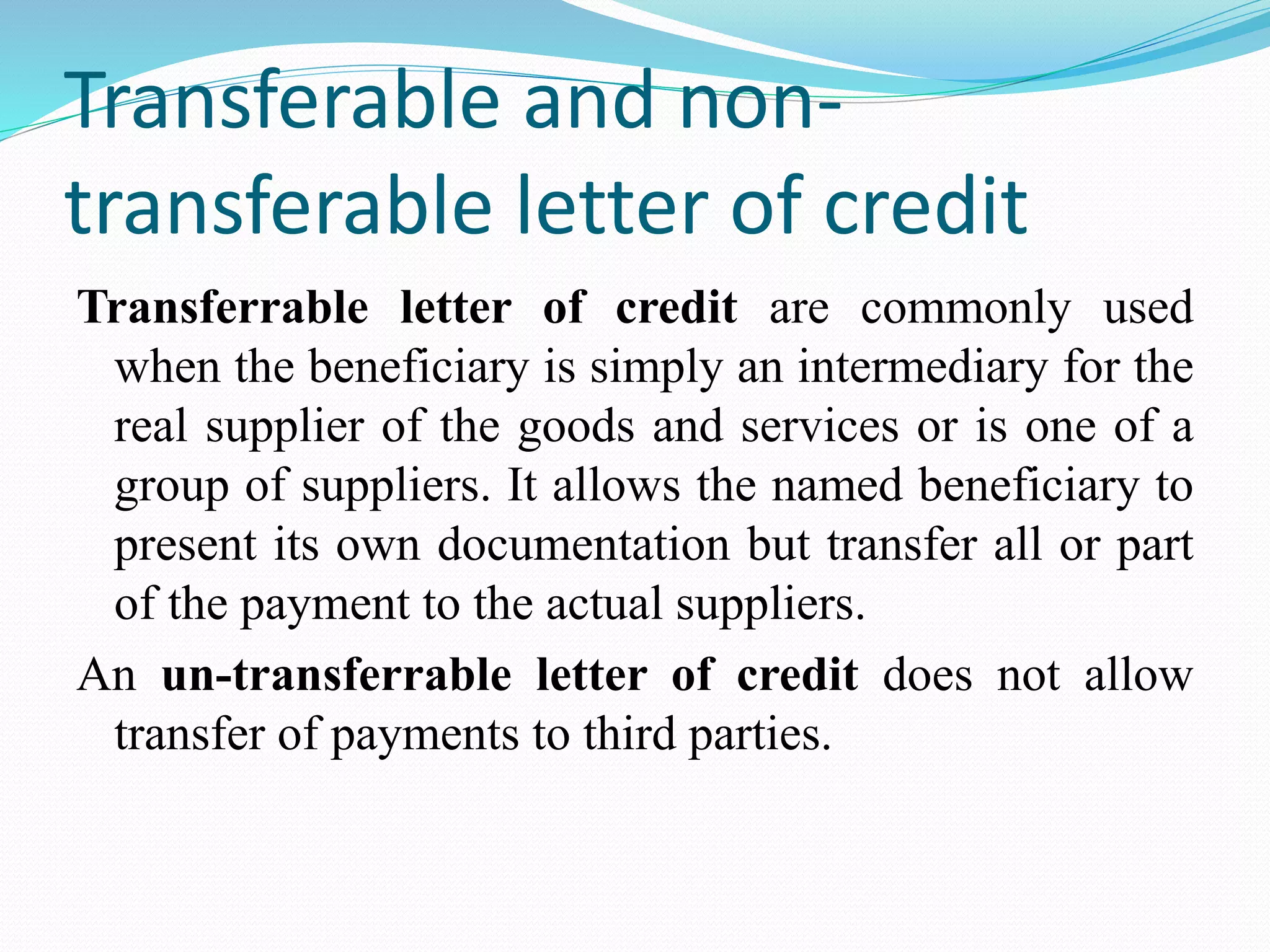

The document outlines various banking practices related to money transfer, including remittance business, types of instruments like bank drafts, letters of credit, and credit cards. It details the mechanics of internal and international transfers, highlighting the roles of banks in facilitating transactions and ensuring payment security. Additionally, it discusses the advantages and risks of using letters of credit and credit cards in commercial activities.