Download to read offline

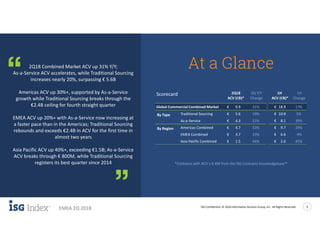

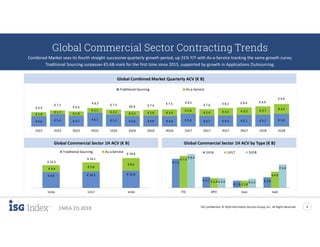

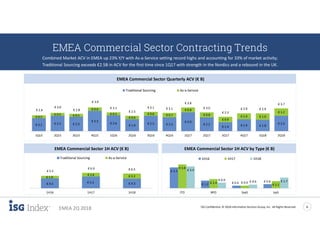

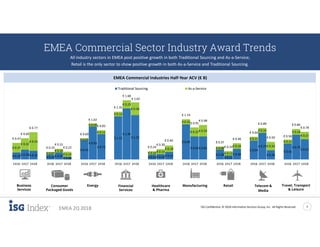

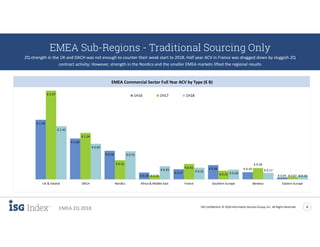

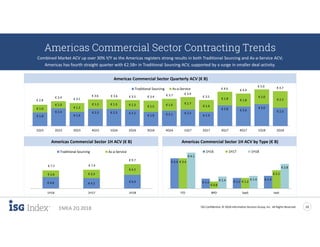

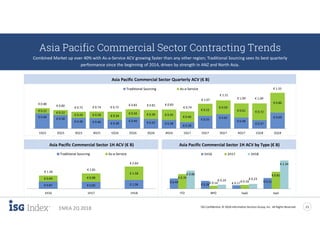

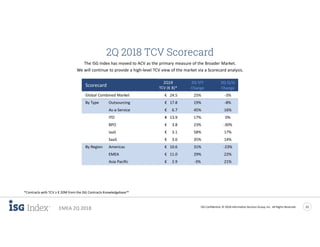

The ISG Index for the second quarter of 2018 reports significant growth in the global commercial contracting market, with an overall annual contract value (ACV) increase of 31% year-over-year. As-a-service ACV experienced a notable surge of 51%, surpassing traditional sourcing, which also grew by 19%. EMEA showed strong recovery trends, particularly in traditional sourcing, while the Asia Pacific region observed the highest growth at 40%.