Downloaded 62 times

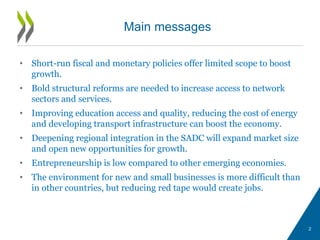

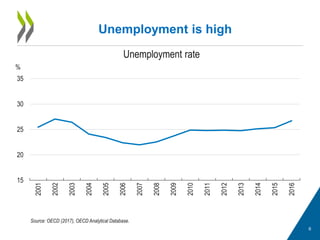

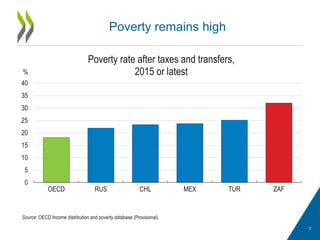

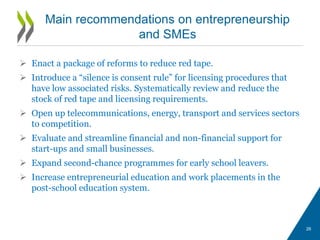

The document summarizes key findings from the 2017 OECD Economic Survey of South Africa. It finds that while short-term fiscal and monetary policies have limited scope to boost growth, bold structural reforms are needed in areas like network sectors, education, energy infrastructure, and regional integration. Unemployment remains high in South Africa and poverty reduction has been slow. The report recommends reforms such as improving education and vocational training, reducing red tape for businesses, opening up more sectors to competition, deepening regional integration within the SADC, and boosting entrepreneurship.