Download to read offline

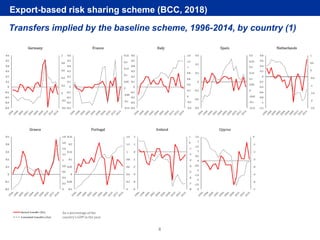

This document discusses the debate around using the EU budget for economic stabilization. It provides an overview of current proposals, including the European Investment Stabilization Function and a euro area budgetary instrument for competitiveness and convergence. Specific risk sharing schemes are examined, including one based on compensating countries for export shocks. While risk sharing and risk reduction can complement each other, combining them poses challenges around enforcement. There is academic agreement that a central fiscal capacity is needed, but political agreement remains divided due to moral hazard concerns. The current strategy is to establish a small instrument focused on convergence and competitiveness that could expand over time.