Downloaded 398 times

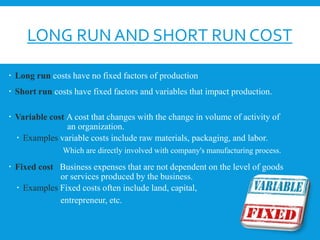

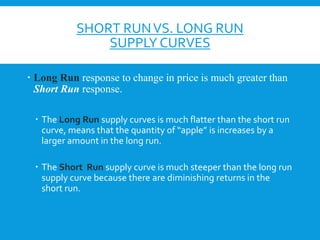

The document outlines the differences between short run and long run in production, emphasizing that the long run allows for all factors of production to be adjusted, whereas the short run has at least one fixed factor. It explains how demand and costs vary between the two time periods, with short run demand reacting immediately to changes and long run demand reflecting ultimate adjustments. Additionally, it discusses the characteristics of short run and long run supply curves, noting that the long run supply response to price changes is significantly greater.