Download to read offline

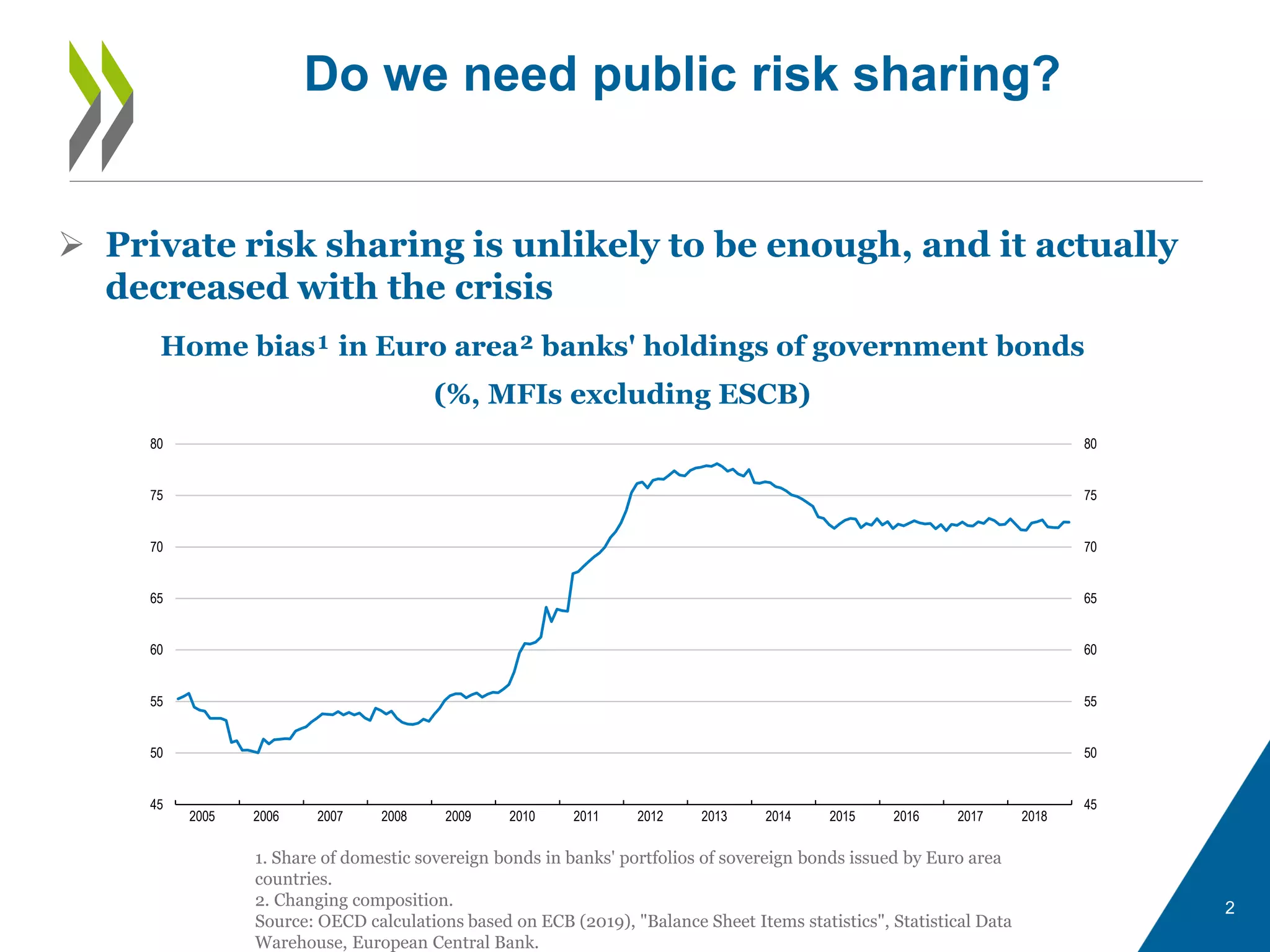

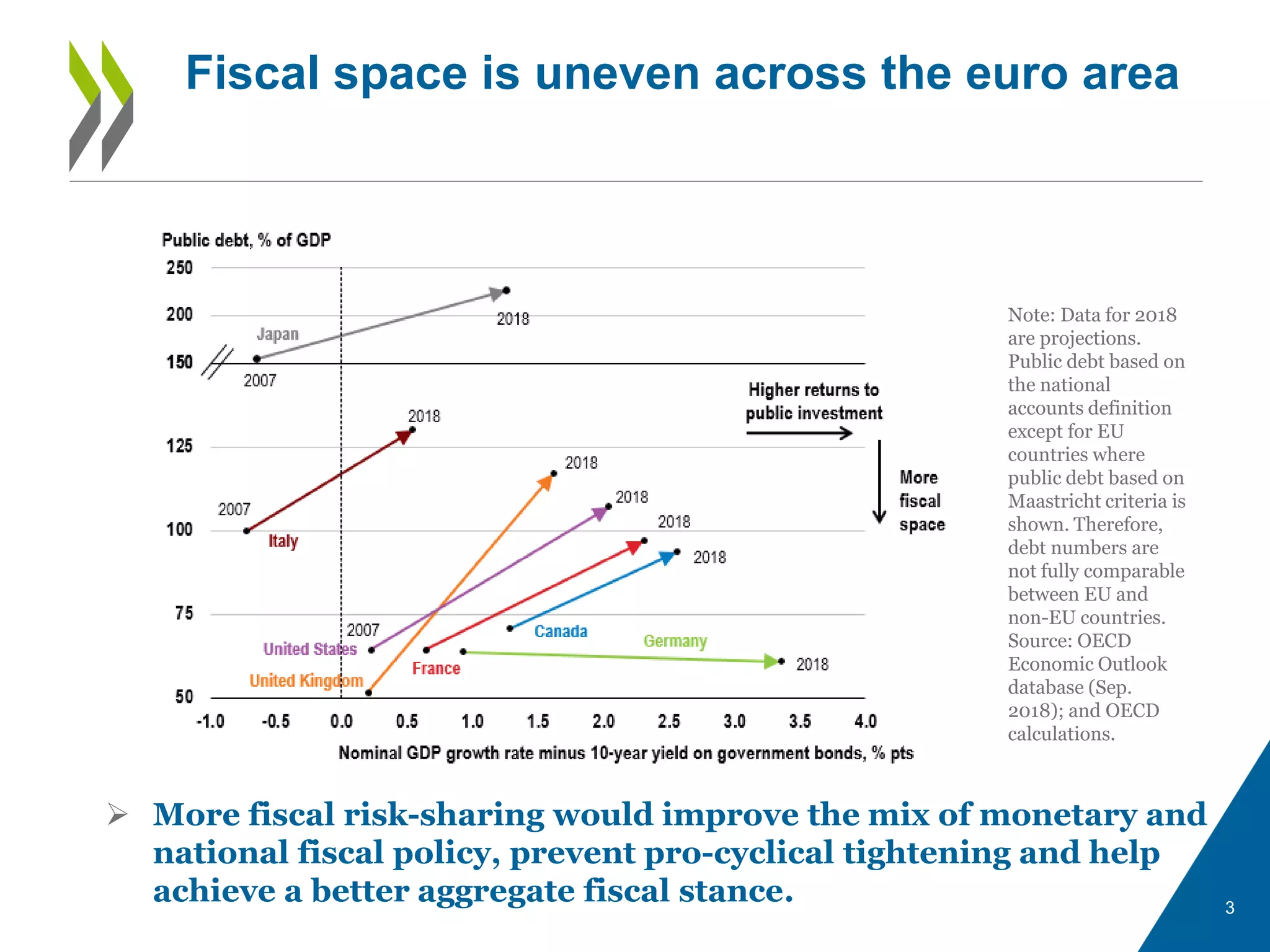

1) The EU needs a fiscal tool for crisis management as private risk sharing is low compared to other monetary unions and failure to stabilize the economic cycle leaves long lasting scars. 2) More fiscal risk-sharing would improve coordination of monetary and fiscal policy, prevent pro-cyclical tightening, and help achieve a better aggregate fiscal stance. 3) Reforming the EU fiscal rules and designing a common fiscal capacity together could combine risk reduction through better rules with risk sharing through a fiscal capacity to help stabilize economies.