Downloaded 12 times

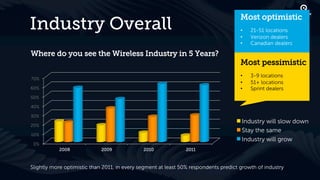

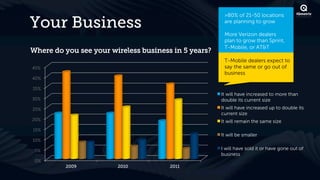

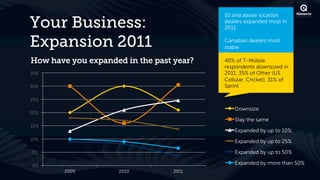

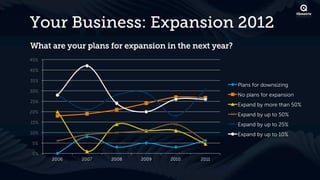

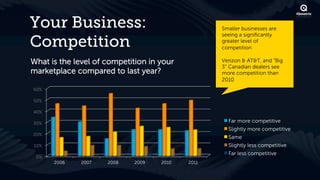

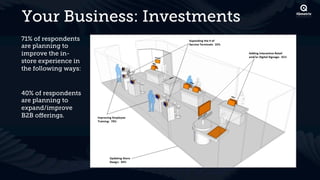

The document summarizes the findings of the 2011 State of Wireless Industry Survey, which received 158 responses. Key highlights include: - Respondents were optimistic about industry growth but less optimistic about their own businesses. Expansion plans have decreased. - Carriers remain the biggest competition. The pending AT&T acquisition of T-Mobile is seen as an increasing threat. - Optimism is driven by growth in diverse devices and increased data usage on new applications. - Over half of respondents expect their wireless businesses to grow in the next 5 years, with larger dealers and Verizon dealers being most optimistic.

![Wide Format Printers: A Hidden Profit Pool [Global Channel Partners Summit]](https://cdn.slidesharecdn.com/ss_thumbnails/no-4graphexpo-wideformatdealerpresentation-121012143035-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Slides] Make an App for That: Strategies for Winning Retail Mobile Strategie...](https://cdn.slidesharecdn.com/ss_thumbnails/agmakeanappforthatmar2012webinarv4-120302142747-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)