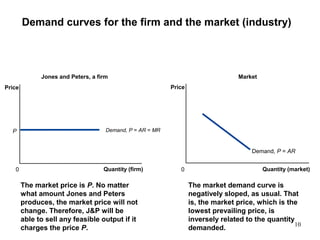

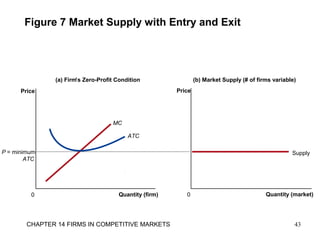

In a perfectly competitive market:

- Many buyers and sellers exist

- Firms are price takers and the actions of any single firm do not impact the market price

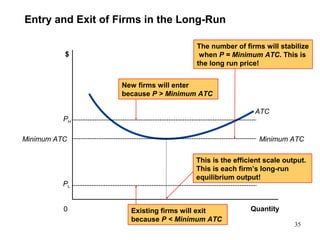

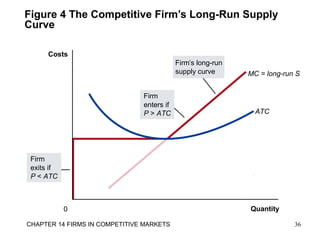

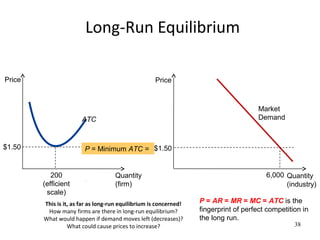

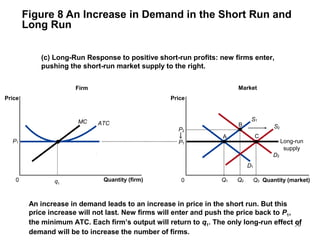

- In the long run, firms will enter or exit the market until price equals minimum average total cost and economic profit is zero.