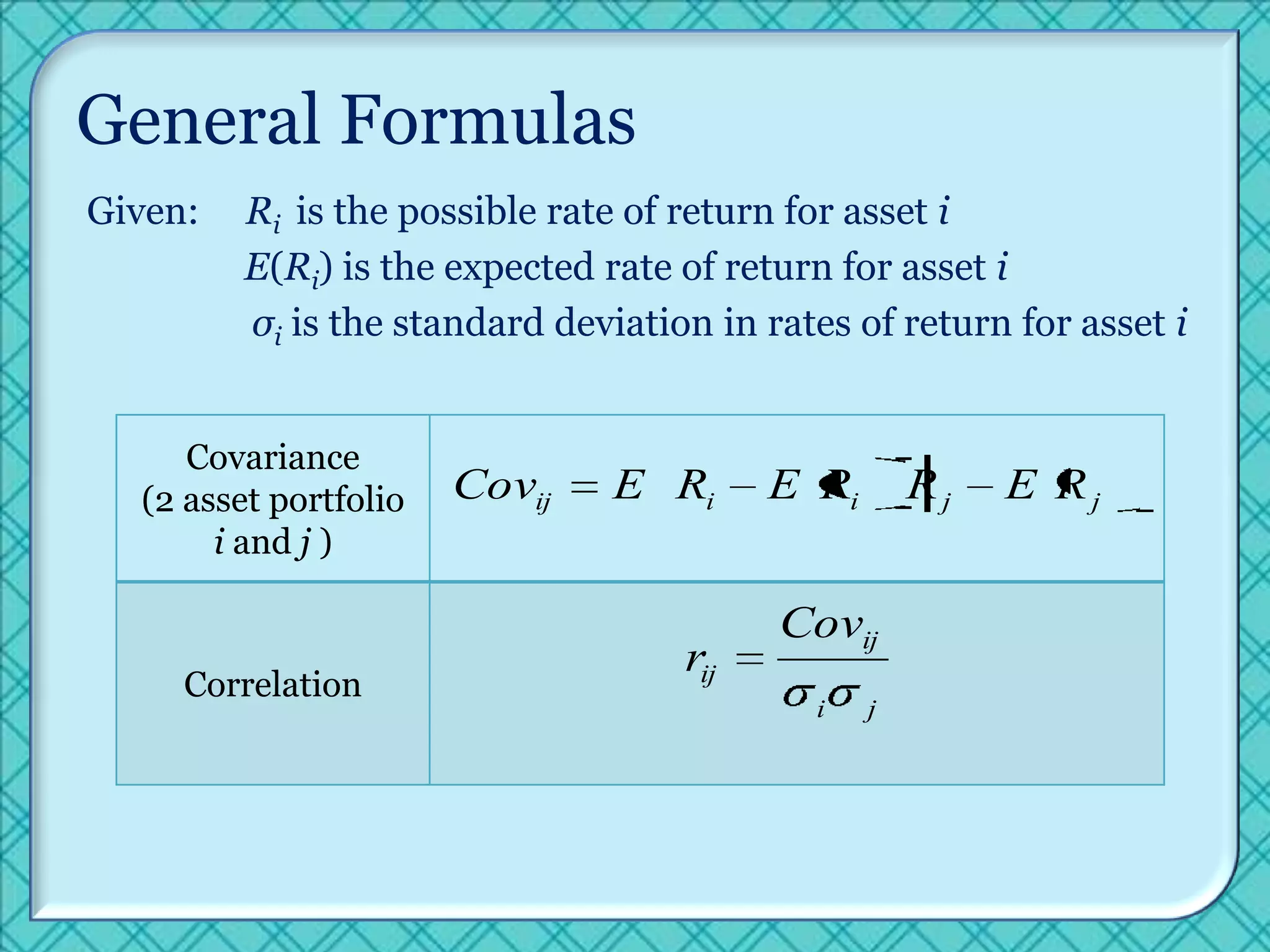

Modern Portfolio Theory provides a framework for constructing investment portfolios to maximize expected return based on a given level of market risk. It assumes investors aim to reduce risk through diversification among assets with low correlations. Markowitz models show how to combine assets to obtain an efficient portfolio with the highest return for a given risk. Mean-variance optimization identifies the portfolio on the efficient frontier with the best risk-return tradeoff. However, the theory relies on historical data and assumptions that may not always hold in real markets.