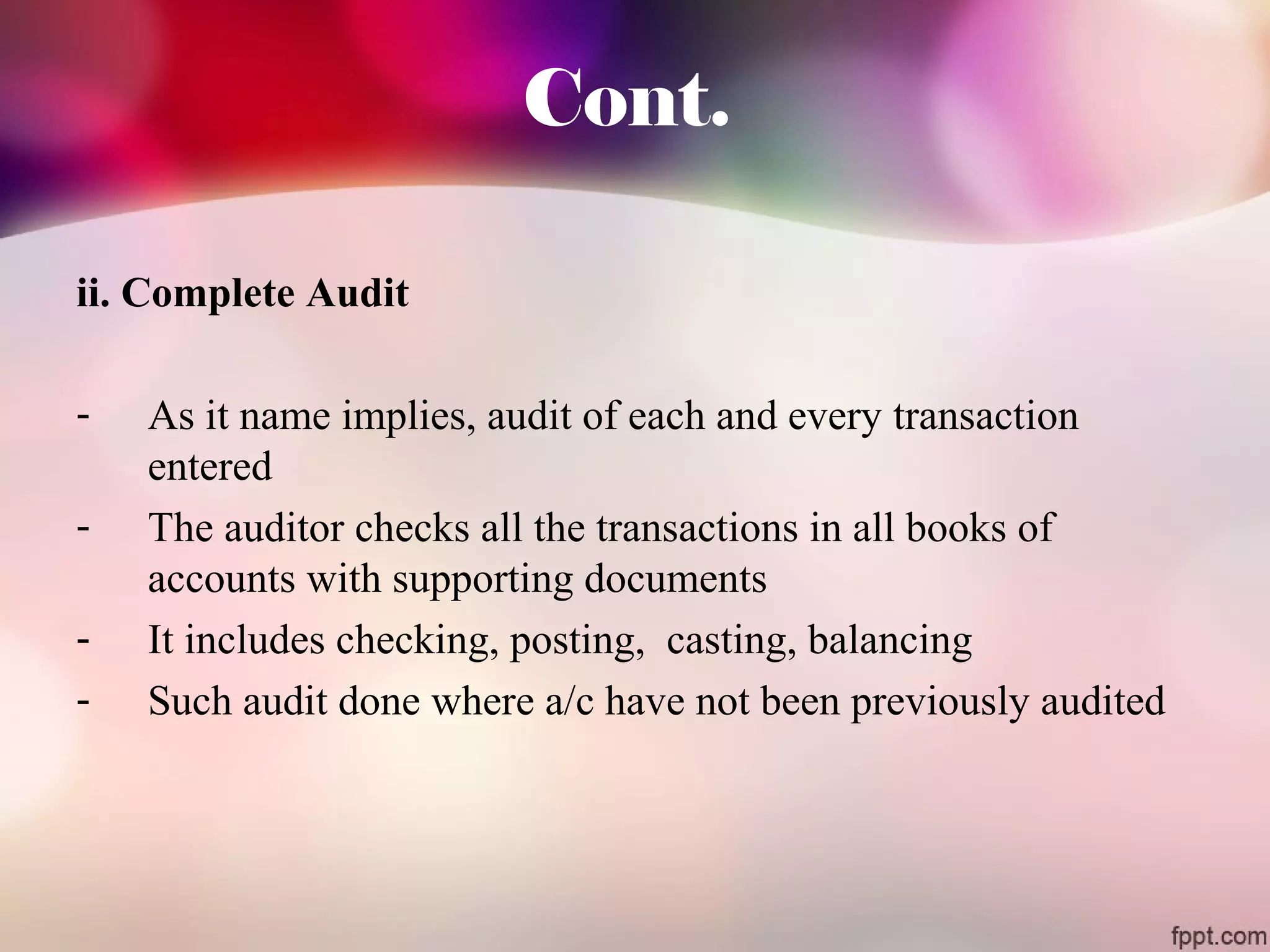

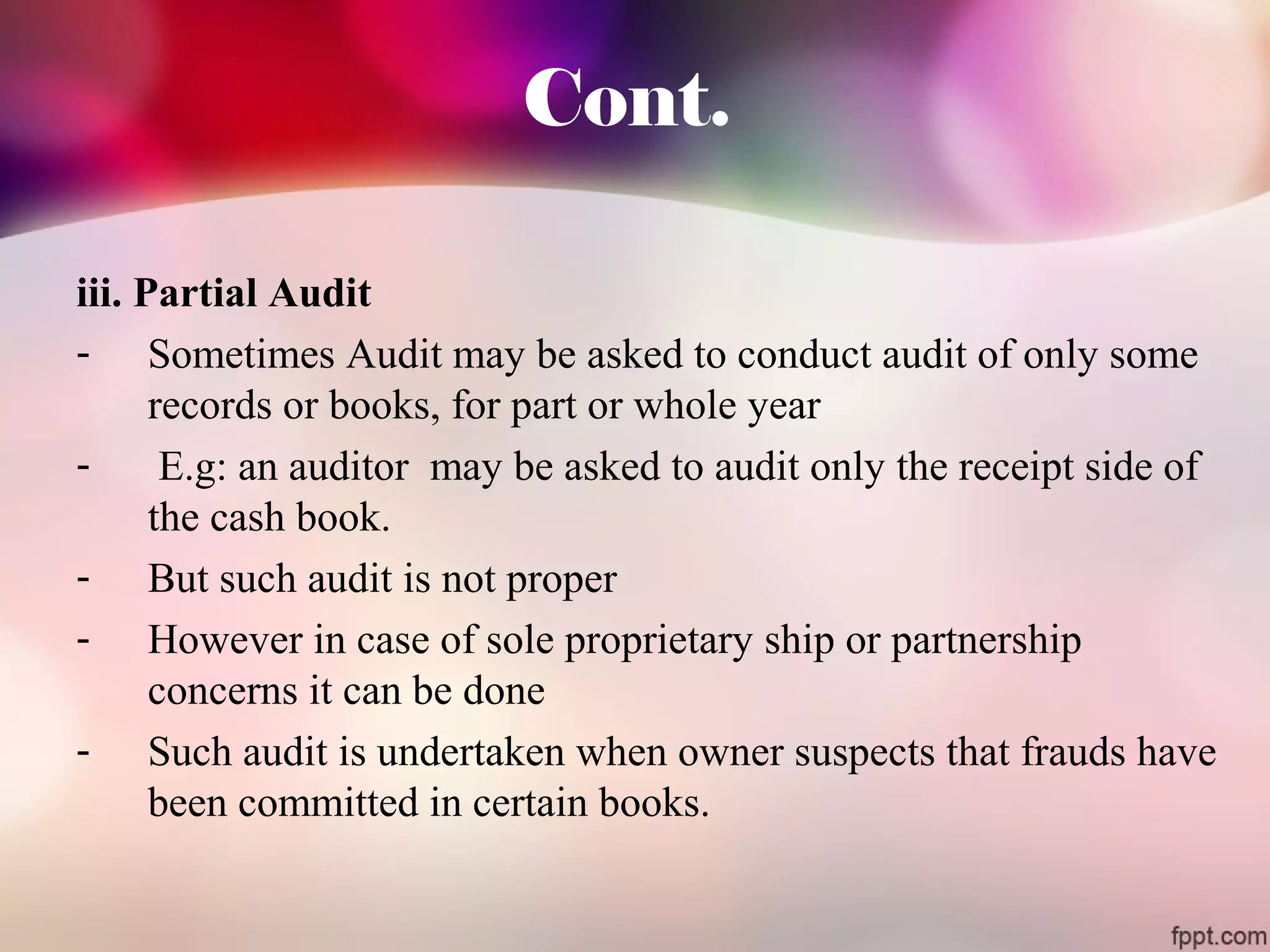

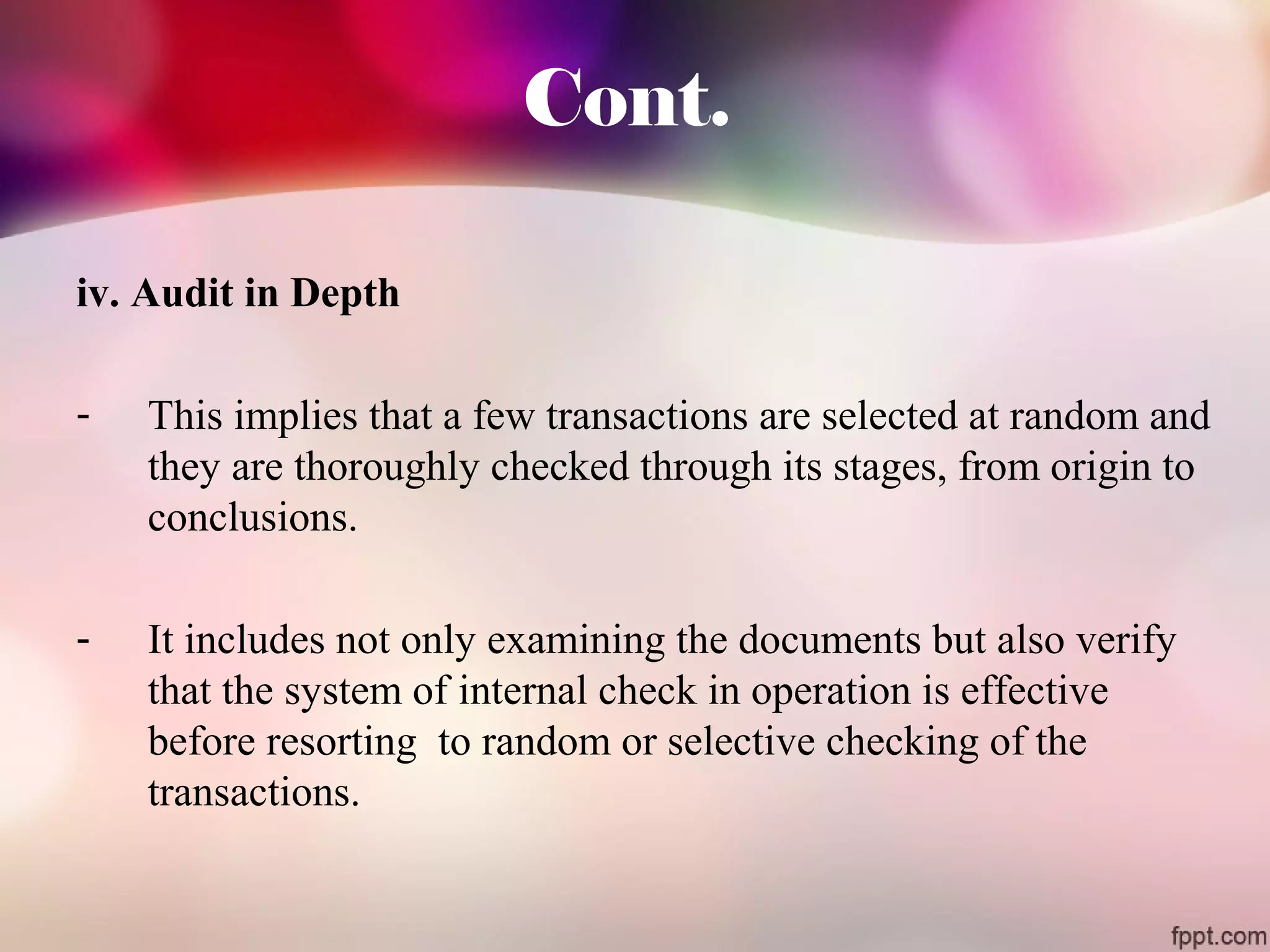

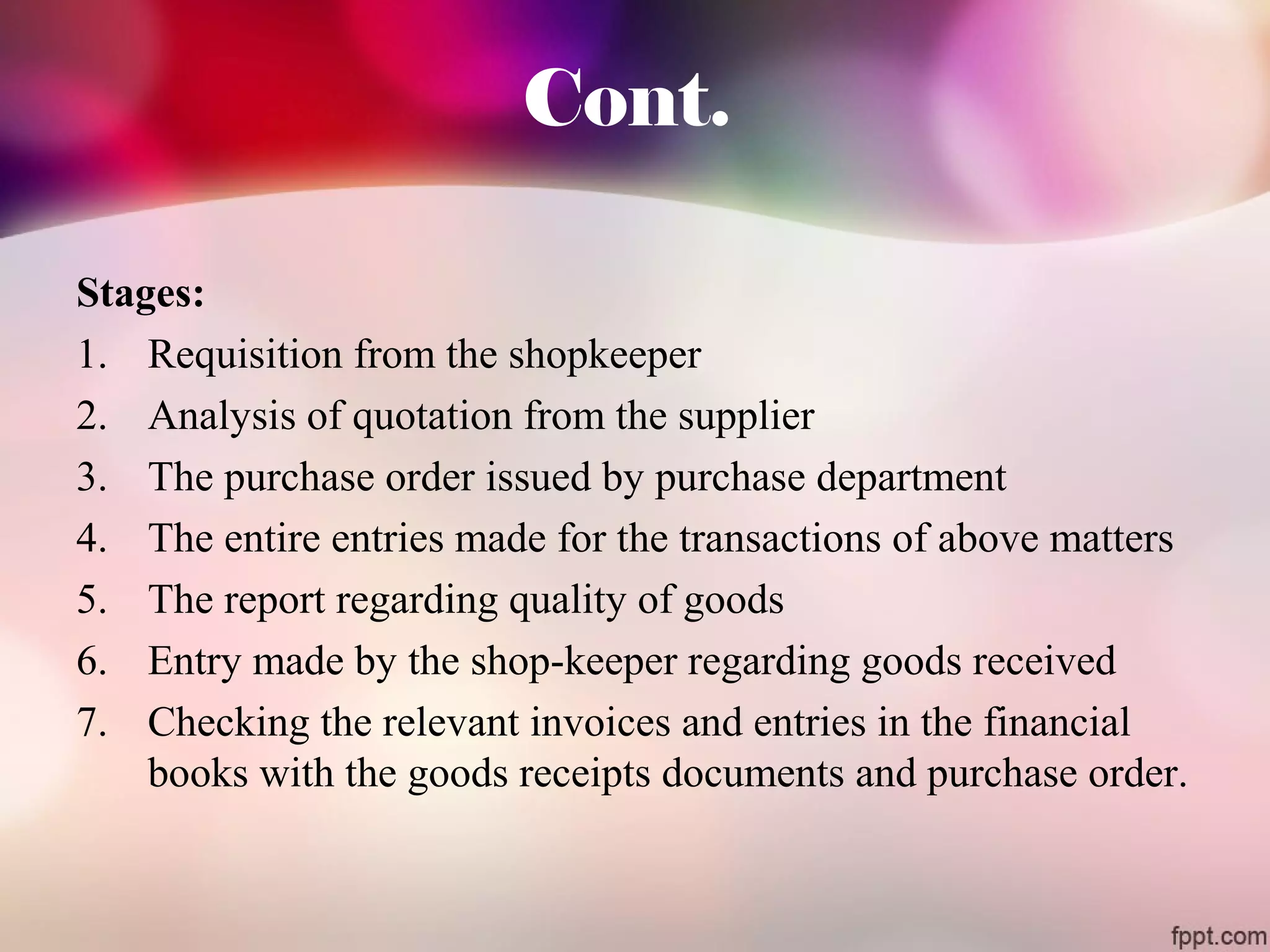

Downloaded 441 times

![2. From view point of Law:

i. Statutory Audit [Compulsory]

ii. Voluntary Audit [Private]](https://image.slidesharecdn.com/unit2-140919134418-phpapp02/75/Unit-2-Types-of-Auditing-8-2048.jpg)

![Cont.

i. Statutory Audit [Compulsory]

▬ Certain type of undertakings established under some law.

a) Company Audit

b) Audit of Trusts

c) Audit of Institutions

d) Government Audit

e) Compulsory Audit

- For Businessman [40 lacs]

- For Professional [10 lacs]](https://image.slidesharecdn.com/unit2-140919134418-phpapp02/75/Unit-2-Types-of-Auditing-9-2048.jpg)

![Cont.

ii. Voluntary Audit: [Private Audit]

▬ For private concerns which are not established by any statute.

a) Sole Proprietary Concerns

b) Partnership Firms

c) Other Institutions or Professional Persons [Doctors, Engineers,

Solicitors]](https://image.slidesharecdn.com/unit2-140919134418-phpapp02/75/Unit-2-Types-of-Auditing-10-2048.jpg)

![Cont.

iii. Branch Audit:

- In case of joint stock co…..

- The statutory auditor of the co. is responsible for the audit of

the branch a/c

1. Acc. To sec. 228…[branch office outside india]

2. Where a/c are audited other than the co.’s auditor…

3. In general meeting the person other than the auditor should be

appointed by BoD.

4. The Branch Auditor.. Duties, qualification, responsibilities,

remuneration, powers etc will be decided by BoD](https://image.slidesharecdn.com/unit2-140919134418-phpapp02/75/Unit-2-Types-of-Auditing-17-2048.jpg)

This document discusses different types of auditing based on the organization being audited, legal requirements, scope, continuity, specialty, and time period. It covers audits of sole proprietorships, partnerships, joint stock companies, trusts, and cooperatives. Statutory audits are compulsory while voluntary audits are private. Internal audits are conducted by employees while external audits use outside auditors. Annual, interim, and branch audits vary based on timing. Specialized audits include cost, management, propriety, and social audits. Continuous, complete, partial, and in-depth audits have different methodologies.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)