Downloaded 17,654 times

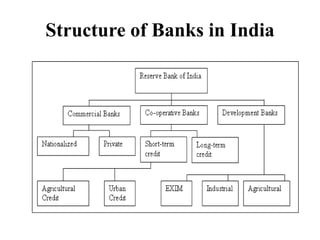

This document provides an overview of the banking system in India. It defines banking and outlines the key laws and institutions that govern banking operations, including the Reserve Bank of India Act and the Banking Regulation Act. It describes the structure of banks in India, categorizing them as commercial banks, cooperative banks, and development banks. It provides details on the various types of commercial banks, cooperative banks, and development banks in India. It also summarizes the major functions and roles of the Reserve Bank of India in regulating the banking system.