BBS 1st year account Accounting for shareholders equity

•

1 like•938 views

Dear friend it is very very useful ppt slide for teaching. Please like comment and subscribe my you tube channel Sapkota Academy.

Recommended

More Related Content

What's hot

What's hot (12)

Similar to BBS 1st year account Accounting for shareholders equity

Similar to BBS 1st year account Accounting for shareholders equity (20)

More from Pragati Secondary School Hetauda- 9, Makawanpur, Nepal

More from Pragati Secondary School Hetauda- 9, Makawanpur, Nepal (19)

Recently uploaded

Recently uploaded (20)

BBS 1st year account Accounting for shareholders equity

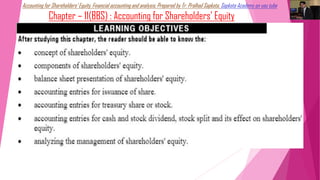

- 1. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Chapter – 11(BBS) : Accounting for Shareholders’ Equity

- 2. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Concept Shareholders’ / Stockholders’ Equity Shareholders' equity (or business net worth) shows how much the owners of a company have invested in the business—either by investing money in it or by retaining earnings over time. It is the amount of assets remaining in a business after all liabilities have been settled. It is calculated as the capital given to a business by its shareholders, plus donated capital and earnings generated by the operation of the business, less any dividends issued.

- 3. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Components/Elements Shareholders’ Equity 1. Common Share/stock: Common stock = Number of shares issued x Par value per share 2. Preferred stock/Preference share Preferred stock=Number of preferred shares issued x Par per share 3. Additional paid in capital/share premium/paid in capital in excess of par (APC) APC = No. of issued shares x(Issue price – Par per share)

- 4. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 4. Contributed Capital/Capital stock: It is the amount of shareholders’ equity the shareholders have contributed to the company. The company received capital amount from the sale of share(CS or PS) to the shareholders. Contributed capital = Common & Pref. stock + Additional paid in capital Or Contributed capital=No of issued shares x Issue price

- 5. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 5. Retained Earning/Undistributed profit / Accumulated earning / The amount of not paid as dividend: RE for the end of a period = Net income–Dividend Paid 6. Treasury stock/Reacquired the co.’s own stock/buy back share/repurchase shares: Methods of retirement (purchase and reissue of TS): Negotiation, Tender price, Open security market price, cost price and par value

- 6. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Balance Sheet Presentation of Shareholders’ Equity: Partial balance sheet of ……Company Ltd. as on 31st …. Particulars Amount Amount Liabilities and Shareholder’s Equity: Contributed capital & shareholders’ fund: …….. % Preferred stock/Preference share capital (Old +…… share issued x Par ) (PSC) Common stock ( Old +……. Share issued x par) (CSC) Additional paid in capital {Old + …. Share issued x (issue price – par)} PS if (APC—PS) Additional paid in capital {Old +…. Share issued x (issue price – par)} CS if (APC—CS) Total contributed capital Retained Earnings ending (Beg. RE + NI –Dividend paid): RE xxx xxx xxx xxx xxx xxx Total contributed capital and Retained Earning Less: Treasury stock If any (No. of TS x repurchase price) Total Shareholders’ Equity or Net worth (TSE or TSF) xxxx xxx xxxx Statement of shareholders’ equity or shareholders’ equity account

- 7. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Analyzing the management of shareholders’ equity/Owners’ Equity 1. Total Shareholders’ equity/ Fund= Total contributed capital + RE – TS = Rs. ……. 2. Total Shareholders’ equity = PSC+ CSC + APC +GR+ RE- TS = Rs. ……. 3. Total SE= Assets- Liabilities or Debt (ie, Assets = Liabilities or Debt + Equity) = Rs. ……. 4. Number of Shares: No. of authorized/Registered shares = …… shares No. of issued shares = 𝐶𝑜𝑚𝑚𝑜𝑛 𝑠ℎ𝑎𝑟𝑒 𝑐𝑎𝑝𝑖𝑡𝑎𝑙 𝑎𝑡 𝑝𝑎𝑟 𝑃𝑎𝑟 𝑣𝑎𝑙𝑢𝑒 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒 = ………… shares No. of common share outstanding (N) = no of issued shares- no of treasury shares 5. Par value or face value or recorded value in paper share certificate but now DEMAT is use. Par value per share = 𝐶𝑜𝑚𝑚𝑜𝑛 𝑠ℎ𝑎𝑟𝑒 𝑐𝑎𝑝𝑖𝑡𝑎𝑙 𝑛𝑜 𝑜𝑓 𝑖𝑠𝑠𝑢𝑒𝑑 𝑠ℎ𝑎𝑟𝑒𝑠 = Rs. ….

- 8. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube DEMAT: Companies have started keeping their shares in electronic form instead of paper share certificates that is associated with share transfer. These are known as DEMAT or dematerialized (converted from physical to electronic) shares. Thus making share trading easy for the users during online trading.

- 9. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 6. Book Value Per Share (BVPS)= 𝑇𝑜𝑡𝑎𝑙 𝐵𝑜𝑜𝑘 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑐𝑜𝑚𝑚𝑜𝑛 𝑒𝑞𝑢𝑖𝑡𝑦 𝑁 or BVPS = 𝑇𝑜𝑡𝑎𝑙 𝑠ℎ𝑎𝑟𝑒ℎ𝑜𝑙𝑑𝑒𝑟𝑠′𝐸𝑞𝑢𝑖𝑡𝑦−𝑃𝑟𝑒𝑓. 𝑠ℎ𝑎𝑟𝑒 𝑐𝑎𝑝𝑖𝑡𝑎𝑙 𝑁 = Rs …. 7. Market value per share (MVPS or MPS or P0): MPS is determined from the interaction between demand and supply of the share in the share market. It is currently trading/selling price. 8. Return on Assets (ROA)= 𝑁𝑃𝐴𝑇+𝐼𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠 x 100=…… % 9. Return on Common Equity (ROCE)= 𝐸𝐴𝐶𝑆 𝐶𝑜𝑚𝑚𝑜𝑛 𝑠ℎ𝑎𝑟𝑒ℎ𝑜𝑙𝑑𝑒𝑟𝑠′𝑒𝑞𝑢𝑖𝑡𝑦 x 100 = ……% or, ROCE = 𝑁𝑃𝐴𝑇 −𝑃𝑑 𝑇𝑆𝐸−𝑃𝑆𝐸 x 100 = ……% And, Return on Equity (ROE) = 𝑁𝑃𝐴𝑇 𝑇𝑆𝐸 x 100 = ……%

- 10. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 10. Preference dividend (Pd)=Preference share capital x given preference dividend rate. 11. Earning per share (EPS)= 𝐸𝐴𝑆𝐶 𝑁 = Rs…. or, EPS = 𝑁𝑃𝐴𝑇 −𝑃𝑑 𝑁𝑜 𝑜𝑓𝑐𝑜𝑚𝑚𝑜𝑛 𝑠ℎ𝑎𝑟𝑒 𝑜𝑢𝑡𝑠𝑡𝑎𝑛𝑑𝑖𝑛𝑔 = Rs…. 12. Earning available to common shareholders (EASC) = Net Income (NI) = NPAT-Pd = Rs… 13. Dividend Per Share (DPS) = 𝑇𝑜𝑡𝑎𝑙 𝐷𝑖𝑣𝑖𝑑𝑒𝑛𝑑𝑠 𝑜𝑓 𝑐𝑜𝑚𝑚𝑜𝑛 𝑠ℎ𝑎𝑟𝑒ℎ𝑜𝑙𝑑𝑒𝑟𝑠 𝑁𝑜 𝑜𝑓𝑐𝑜𝑚𝑚𝑜𝑛 𝑠ℎ𝑎𝑟𝑒 𝑜𝑢𝑡𝑠𝑡𝑎𝑛𝑑𝑖𝑛𝑔 = Rs…. or DPS = 𝑇𝐷 𝑁 = Rs…. 14. Dividend Payout Ratio( D/P or D/E ratio or DPR) = 𝐷𝑃𝑆 𝐸𝑃𝑆 x 100= …. % or, 𝑇𝐷 𝑁𝐼 x 100= …. % 15. Price Earning Ratio (P/E Ratio) = 𝑀𝑃𝑆 𝐸𝑃𝑆 = … times or ……. X 100= ….%

- 11. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Source: Kriti Publication:

- 12. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Source: Asmita Publication:

- 13. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube

- 14. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Accounting entries for issuance of shares/stock (Journal Entries) 1. Share /stock issued for cash: a. If issued at Par: Bank a/c …….. Dr. xxx To Common/Preferred stock a/c xxx (No of issued shares x Par per share) (Being …. common / preference shares issued at Rs…. each) b. If issuance of no par stock or issuance of stated value stock or issued at no par price: Bank a/c …….. Dr. xxx To Common/Preferred stock a/c xxx (No of issued shares x issued price per share) (Being …. common / preference shares issued at Rs…. each)

- 15. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube c. If issued at Premium/APC or issue price is more than par: Bank a/c (No of issued shares x Issue price per share) …….. Dr. xxx To Common/Preferred stock a/c (…..shares x Par each) xxx To Additional Paid in Capital a/c – CS or PS (….shares x prem. each) xxx (Being …. common / preference shares issued at Rs…. each) d. If issued at discount or issue price is less than par: Bank a/c (No of issued shares x Issue price per share) …….. Dr. xxx Discount on issue of ….. Stock a/c(…Share x dis. Rs.. each …. Dr. xxx To Common/Preferred stock a/c (No of shares x Par per share) xxx (Being …. common / preference shares issued at Rs…. each)

- 16. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 2. Share /stock issued for non cash consideration (other than cash): Building (Assets individually) a/c Dr. xxx Discount on issue a/c (if) Dr. xxx To Common stock a/c (…. Share x Par each) xxx To Preferred stock a/c (…. Share x Par each) xxx To APC – CS a/c (…issued shares x prem--CS) (if) xxx To APC – PS a/c (…issued shares x prem--PS) (if) xxx (Being issuance of common / preference stock for purchase of building….)

- 17. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 2. Share /stock issued on subscription basis or contract basis purchase: When an investor purchases share on a subscription basis prior to incorporation of the business entity, a partial payment is received and the share is not issued until the final payment is made. The offer specify the part of the share price payable at the time of buying for share and require that the balanced amount be paid when share are issued whether it is on contract basis or subscription basis.

- 18. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube On agreement/signing date: Cash or Bank a/c (Partial amt. if) Dr. xxx Subscription Receivable a/c Dr xxx To Common stock subscribed a/c (…. Share x Par each) xxx To APC – CS a/c (..issued shares x prem. - CS) (if) xxx (Being issuance of common stock on subscription basis) On amount receiving date: Cash or Bank a/c Dr. xxx To Subscription Receivable a/c xxx (Being subscription receivable amount received)

- 19. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Source: Asmita Publication

- 20. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube

- 21. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube

- 22. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube

- 23. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube

- 24. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Source: Kriti Publication: IIlustration 9: On Feb. 1, Help corporation signs a contract with an investor to issue 100 shares of stock with a par value of Rs. 10 for Rs. 80 per share in one month. The buyer has to make a down payment of Rs. 800 at the signing date. And subscription balance was paid on march 1. Required: Journal Entries with effect on balance sheet. Solution: On Feb 1: Bank a/c Dr 800 Subscription Receivable a/c Dr 7200 To Common stock subscribed a/c (100 Share x Rs. 10 each) 1000 To APC – CS a/c (100 shares x 70) 7000 (Being issuance of common stock on subscription basis) On March 1: Bank a/c Dr 7200 To Subscription Receivable a/c 7200 (Being subscription receivable amount received)

- 25. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Accounting entries for treasury share/stock (Journal Entries) 1. Purchase of treasury share /stock: Treasury Stock a/c Dr xxx To Cash or bank a/c xxx (Being purchase of …. shares of treasury stock at Rs…. each) 2. Re sale or Release or Re issue of treasury share / stock: a. Sale / re issue of treasury stock at cost Cash or Bank a/c Dr xxx To Treasury stock a/c xxx (Being sale of …. Shares of TS at cost of Rs….each)

- 26. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube b. Sale / re issue of treasury stock above cost Cash or Bank a/c (No of TS x Re issue price) Dr xxx To Treasury stock a/c (No of TS x Cost price) xxx To APC a/c – TS (No of TS x above price) xxx (Being sale of …. Shares of TS at above cost of Rs….each) c. Sale / re issue of treasury stock below cost Cash or Bank a/c (No of TS x Re issue price) Dr xxx Retained Earning or APC-TS a/c (No of TS x below price) Dr xxx To Treasury stock a/c (No of TS x Cost price) xxx (Being sale of …. Shares of TS at below cost of Rs….each)

- 27. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 3. Retirement of treasury share / stock: i. On cost method: a. Retirement of treasury stock at cost equal to originally issued at par: Common stock a/c Dr xxx To Treasury stock a/c xxx (Being retirement of …. shares of TS) b. Retirement of treasury stock at cost above than par: Common stock a/c (No of TS x par) Dr xxx Retained Earning or APC-TS a/c (No of TS x above price) Dr xxx To Treasury stock a/c (No of TS x cost price) xxx (Being retirement of …. Shares of TS )

- 28. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube c. Retirement of treasury stock at cost below than par: Common stock a/c (No of TS x par) Dr xxx To Treasury stock a/c (No of TS x cost price) xxx To Retained Earning or APC-TS a/c (No of TS x below price) xxx (Being retirement of …. Shares of TS) ii. On par value method: Common stock a/c Dr xxx To Treasury stock a/c xxx (Being retirement of …. shares of TS)

- 29. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Source: Asmita Publication

- 30. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube

- 31. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube

- 32. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Source: accountingformanagement.org The American company issued 5,000 shares of its Rs. 5 par value common stock at Rs. 8 per share. Later, the company bought back 1,000 shares at Rs. 12 per share and immediately retired them. Required: Prepare journal entries for retiring the shares assuming the company accounts for treasury stock related transactions using: 1. Cost method. 2. Par value method.

- 33. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Solution: 1. When 1,000 shares are retired – Under cost method: Common Stock a/c (1000 x 5) Dr 5000 Additional Paid in Capital–TS a/c* Dr 3000 Retained earning a/c** Dr 4000 To Treasury stock a/c (1000 x 12) 12000 (Being retirement of 1000 shares of TS at cost) *Additional paid in capital associated with 1,000 shares: 1,000 × (Rs. 8 – Rs. 5)= Rs. 3,000 **Retained earnings account has been debited with the remaining amount: (Rs. 12,000 – Rs. 5,000 – Rs. 3,000= Rs. 4,000)

- 34. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Solution: 2. When 1,000 shares are retired – Under Par value method: Common Stock a/c (1000 x 5) Dr 5000 To Treasury stock a/c (1000 x 5) 12000 (Being retirement of 1000 shares of TS at par)

- 35. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Dividend / Distributed earning It is the return on common stockholder after distribution to bondholder and preferred stockholders. It is part of profit. If a company has sufficient cash available and adequate retained earning dividend may be declared. It is not expenses, it is liabilities on the date of declaration. Types: 1. Cash Dividend 2. Stock Dividend/Bonus share

- 36. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 1. Cash Dividend: Cash dividend is cash distribution of accumulated earning by a company to its shareholders. There are various types of cash dividend payment policy. BOD may apply one policy to declare dividend after approval of resolution. Generally cash dividend amount can be calculated from the following: Amount of cash dividend = Total par value of CS x Div. Rate = N x Par per share x Div. Rate= Rs…

- 37. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Accounting Entries for Cash Dividend (Journal Entries): 1. At the time of dividend declaration: Retained Earning a/c Dr xxx To Cash dividend payable a/c xxx (Being record for declaration of cash dividend) 2. At the time of dividend payment: Cash dividend payable a/c Dr xxx To cash or bank a/c xxx (Being record the payment of cash dividend)

- 38. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Effect of cash dividend on shareholders equity and Balance Sheet • Decrease the cash or bank (asset) equal by dividend amount • Decrease the amount of retained earning equal by dividend amount (ie, New RE= old RE – dividend) • Decrease the Value of the firm equal by total dividend • Decrease the MPS equal by DPS. Where, Adjusted price of a stock or MPS after cash dividend = MPS before cash dividend - DPS

- 39. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 2. Stock Dividend / Bonus Share: If the company distributes additional share rather than cash as dividend to it’s existing shareholder with free of cost is called stock dividend. Company use stock dividend from the following reason: • If the company has not sufficient cash available • To reduce price at reasonable tradable range in the market for small scale investors • To make tax benefit for investors

- 40. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Accounting Entries for Stock Dividend (Journal Entries): The journal entries for a stock dividend depends on whether the company is involved in a small stock dividend or a large stock dividend. The journal entries for both sizes are as follows: 1. Small size stock dividend (up to 25% or less than 25%) A stock dividend is considered a small stock dividend if the number of shares being issued is less than 25%. It will have little effect on the market price and it to be recorded at fair market price.

- 41. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 1. At the time of stock dividend declaration: Retained Earning (n x MPS) a/c Dr xxx To CS dividend distributable (n x MPS) a/c xxx (Being record for declaration of stock dividend) 2. At the time of distribution of stock dividend: CS dividend distributable a/c (n x MPS) xxx To Common stock a/c (n x par) xxx To APC – CS a/c (n x Premium per share) xxx (Being record the distribution of stock dividend)

- 42. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 2. Large size stock dividend (greater than 25%) A stock dividend is considered a large stock dividend if the number of shares being issued is greater than 25%. It will have more effect on the market price and it to be recorded at par value. 1. At the time of stock dividend declaration: Retained Earning a/c (n x Par) Dr xxx To CS dividend distributable a/c (n x par) xxx (Being record for declaration of stock dividend)

- 43. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube 2. At the time of distribution of stock dividend: CS dividend distributable (n x par) a/c xxx To Common stock a/c xxx (Being record the distribution of stock dividend) Effect of stock dividend on shareholders equity: Consider: N= no of old shares outstanding = ……. shares SDR= Stock Dividend Rate (…% Given) n (No of stock dividend) = N x SDR = …… shares

- 44. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Effect: 1. Increase the no. of Shares equal by n :. Total no of shares after stock dividend= N + n = … Shares or Nx(1+ SDR)=…. Shares 2. Decrease the amount of Retained Earning equal by (n x MPS) :. New RE= old Retained Earning-(n x MPS) for Small size stock dividend :. New RE= old Retained Earning-(n x Par) for large size stock dividend 3. Decreased the Retained Earning transferred to Common Stock at par and Additional paid in Capital at premium.

- 45. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube :.Total amount of new common stock=old CS + n x par per share = Rs …. or (N + n)x par per share = Rs ….. :. Total amount of New APC= old APC + (n x premium per share) 4. Total value of TS, PS, TSE unchanged. Or, You can work at chart for small size stock dividend: n = N x SDR =…….. shares = Rs…… add in CS = Rs…… add in APC x MPS(Po)Rs ….= Rs…… Less from RE

- 46. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Or, You can work at chart for large size stock dividend: n = N x SDR =…….. shares = Rs…… add in CS = Rs 0 add in APC X par Rs…. = Rs…… Less from RE 5. MPS, EPS and DPS after stock dividend decreased :. adjusted price (P1) will decreased :. P1= Total Market Value of Equity / Total no of Share = P0 x N N +n or, P1 = P0 1+ SDR Where P0 =Currently selling price or existing MPS

- 47. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Stock Split: It is the process of increasing the number of share and decreasing the par and stock’s price in to reasonable tradable range for small scale investors. The main objective of stock split is to reduce the market price in order to make attractive to the investors. Example: Stock split (Given) Find: split ratio 2 for 1 stock split --- 2/1 3 for 2 stock split --- 3/2 5 for 2 stock split --- 5/2

- 48. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Effect and recording of stock split on shareholders equity: • Increase the no. of share by split ratio. :. Total no of share after split= N x split ratio= …….. Shares • Decrease the par, MPS, EPS and DPS by split ratio :. Par after split = old par 𝑆𝑝𝑙𝑖𝑡 𝑟𝑎𝑡𝑖𝑜 = Rs…. :. MPS after split = old MPS 𝑆𝑝𝑙𝑖𝑡 𝑟𝑎𝑡𝑖𝑜 = Rs… • Total value of CS, APC, RE and TSE unchanged. :. Common stock( …… share x par) = Rs. …… # Accounting transaction is not recorded if company declares and executes a stock split.

- 49. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Source: Asmita Publication: QN 5: Do yourself

- 50. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Source: Asmita Publication: QN 11: Do yourself

- 51. Accounting for Shareholders’ Equity, Financial accounting and analysis, Prepared by Tr. Pralhad Sapkota, Sapkota Academy on you tube Thank You