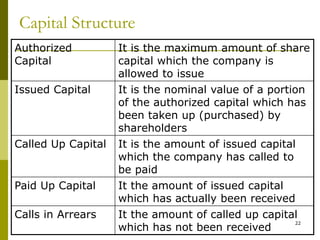

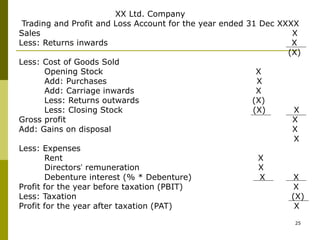

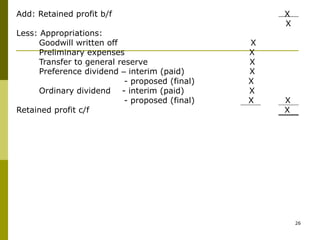

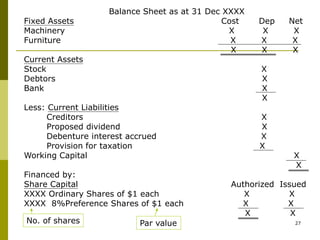

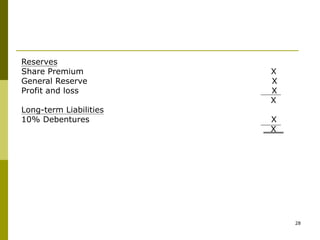

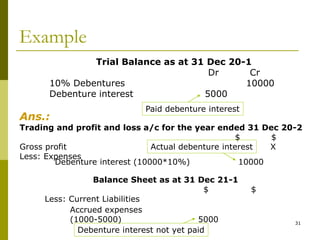

The document provides information about types of companies and final accounts preparation for limited companies in Hong Kong. It discusses key aspects such as types of limited companies (private and public), share capital structure, means of funding, reserves, appropriation of profits, and bonus share issues. The final accounts include the trading and profit & loss account and balance sheet, with details on treatment of expenses like debenture interest and dividends for limited companies.