Youngest aren’t always the trendsetters

•

2 likes•4,751 views

Our most recent US edition of the Global Mobile Consumer Survey showed that with the technological know-how and the increased cash flow, 25 to 34-year-olds are demonstrating higher levels of mobile device interest and use. Learn more at www.deloitte.com/us/mobileconsumer

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (18)

Similar to Youngest aren’t always the trendsetters

Similar to Youngest aren’t always the trendsetters (20)

More from Deloitte United States

More from Deloitte United States (20)

Recently uploaded

Recently uploaded (20)

Youngest aren’t always the trendsetters

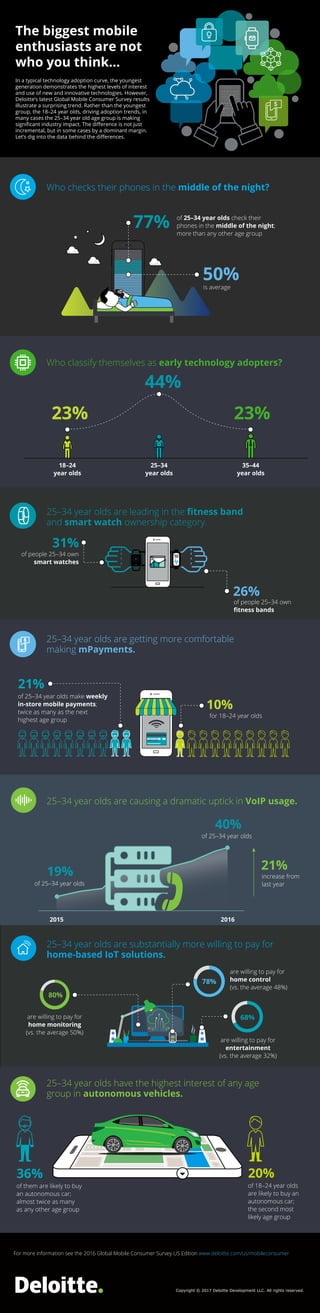

- 1. The biggest mobile enthusiasts are not who you think… In a typical technology adoption curve, the youngest generation demonstrates the highest levels of interest and use of new and innovative technologies. However, Deloitte’s latest Global Mobile Consumer Survey results illustrate a surprising trend. Rather than the youngest group, the 18–24 year olds, driving adoption trends, in many cases the 25–34 year old age group is making significant industry impact. The difference is not just incremental, but in some cases by a dominant margin. Let’s dig into the data behind the differences. of 25–34 year olds check their phones in the middle of the night; more than any other age group 31% 26% 21% 10% 77% 68% 80% 78% Who checks their phones in the middle of the night? Who classify themselves as early technology adopters? 25–34 year olds are leading in the fitness band and smart watch ownership category. 25–34 year olds are getting more comfortable making mPayments. 25–34 year olds are causing a dramatic uptick in VoIP usage. 25–34 year olds are substantially more willing to pay for home-based IoT solutions. 50% is average 18–24 year olds 25–34 year olds 35–44 year olds 23% 44% of people 25–34 own fitness bands of people 25–34 own smart watches of 25–34 year olds make weekly in-store mobile payments; twice as many as the next highest age group for 18–24 year olds 19% 40% 2015 2016 21% increase from last year 25–34 year olds have the highest interest of any age group in autonomous vehicles. are willing to pay for home monitoring (vs. the average 50%) are willing to pay for entertainment (vs. the average 32%) are willing to pay for home control (vs. the average 48%) 36% of them are likely to buy an autonomous car; almost twice as many as any other age group 20% of 18–24 year olds are likely to buy an autonomous car; the second most likely age group of 25–34 year olds of 25–34 year olds Copyright © 2017 Deloitte Development LLC. All rights reserved. For more information see the 2016 Global Mobile Consumer Survey US Edition www.deloitte.com/us/mobileconsumer 23%