RELATED PARTIES - ECONOMY

•

1 like•125 views

LET SEE AND GET KNOWLEDGE FROM IT

Recommended

More Related Content

What's hot

What's hot (20)

Similar to RELATED PARTIES - ECONOMY

Similar to RELATED PARTIES - ECONOMY (20)

More from MUHAMMAD HUZAIFA CHAUDHARY

More from MUHAMMAD HUZAIFA CHAUDHARY (20)

Recently uploaded

Recently uploaded (20)

RELATED PARTIES - ECONOMY

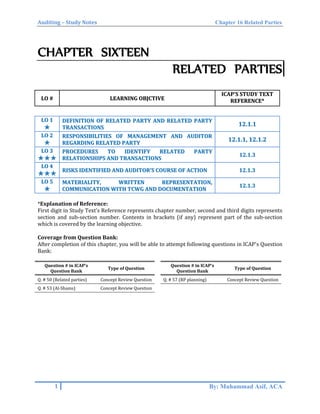

- 1. Auditing – Study Notes Chapter 16 Related Parties CHAPTER SIXTEEN RELATED PARTIES LLOO ## LLEEAARRNNIINNGG OOBBJJCCTTIIVVEE IICCAAPP''SS SSTTUUDDYY TTEEXXTT RREEFFEERREENNCCEE** LLOO 11 ✯✯ DDEEFFIINNIITTIIOONN OOFF RREELLAATTEEDD PPAARRTTYY AANNDD RREELLAATTEEDD PPAARRTTYY TTRRAANNSSAACCTTIIOONNSS 1122..11..11 LLOO 22 ✯✯ RREESSPPOONNSSIIBBIILLIITTIIEESS OOFF MMAANNAAGGEEMMEENNTT AANNDD AAUUDDIITTOORR RREEGGAARRDDIINNGG RREELLAATTEEDD PPAARRTTYY 1122..11..11,, 1122..11..22 LLOO 33 ✯✯✯✯✯✯ PPRROOCCEEDDUURREESS TTOO IIDDEENNTTIIFFYY RREELLAATTEEDD PPAARRTTYY RREELLAATTIIOONNSSHHIIPPSS AANNDD TTRRAANNSSAACCTTIIOONNSS 1122..11..33 LLOO 44 ✯✯✯✯✯✯ RRIISSKKSS IIDDEENNTTIIFFIIEEDD AANNDD AAUUDDIITTOORR’’SS CCOOUURRSSEE OOFF AACCTTIIOONN 1122..11..33 LLOO 55 ✯✯ MMAATTEERRIIAALLIITTYY,, WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONN,, CCOOMMMMUUNNIICCAATTIIOONN WWIITTHH TTCCWWGG AANNDD DDOOCCUUMMEENNTTAATTIIOONN 1122..11..33 *Explanation of Reference: First digit in Study Text’s Reference represents chapter number, second and third digits represents section and sub-section number. Contents in brackets (if any) represent part of the sub-section which is covered by the learning objective. Coverage from Question Bank: After completion of this chapter, you will be able to attempt following questions in ICAP's Question Bank: Question # in ICAP’s Question Bank Type of Question Question # in ICAP’s Question Bank Type of Question Q. # 50 (Related parties) Concept Review Question Q. # 57 (RP planning) Concept Review Question Q. # 53 (Al-Shams) Concept Review Question 1 By: Muhammad Asif, ACA

- 2. Auditing – Study Notes Chapter 16 Related Parties LLOO 11:: DDEEFFIINNIITTIIOONN OOFF RREELLAATTEEDD PPAARRTTYY AANNDD RREELLAATTEEDD PPAARRTTYY TTRRAANNSSAACCTTIIOONNSS:: Related Parties: A related party is either a party as defined in AFRF. If AFRF establishes no or minimum requirements, related party is: A person or entity which has control or significant influence over audit client. An entity over which audit client has control or significant influence. An entity which is under common control with audit client through common key management, common controlling ownership, and owners who are close family members. Examples of related parties include directors, majority shareholders, holding company, subsidiary, associated company. Related Party Transactions: Related party transactions are transactions between the client company and a related party of the company. CONCEPT REVIEW QUESTION What is a related party and a related party transactions? (04 marks) (CA Final, Winter 1991) LLOO 22:: RREESSPPOONNSSIIBBIILLIITTIIEESS OOFF MMAANNAAGGEEMMEENNTT AANNDD AAUUDDIITTOORR RREEGGAARRDDIINNGG RREELLAATTEEDD PPAARRTTYY:: Responsibilities of Management: If AFRF establishes related party requirements, responsibility of management will be to identify, account for and disclose related party relationships and transactions in accordance with AFRF. Responsibilities of Auditor: Auditor is responsible to evaluate: 1. whether related party relationships/transactions have been appropriately identified, accounted for and disclosed in accordance with AFRF. 2. whether fraud risk factors exist arising from related party relationships, and 3. whether financial statements present true and fair view in respect of related party relationships. Why party relationships/transactions give higher risk of material misstatement: 1. Related parties may operate through variety of relationships and complex structure. 2. Information systems may not be able to separately identify transactions of related parties. 3. Related party transactions may be conducted at nominal amounts or even without consideration. Why identification of related party relationships/transactions is difficult for auditor: An auditor cannot be held responsible to identify all related-party relationships and transactions because: 1. Management may not be aware of all related party relationships/transactions (particularly if AFRF does not require management to identify/disclose). 2. Management may intentionally conceal related party relationships/transactions for fraud. 3. Some related party transactions involve immaterial values, which are difficult for auditor to detect. 2 By: Muhammad Asif, ACA

- 3. Auditing – Study Notes Chapter 16 Related Parties CONCEPT REVIEW QUESTION You are the audit manager on the audit of Gold Limited. During the planning phase of the audit, the audit senior had a meeting with the CFO of the company. While discussing matters such as performance of the company, financial ratios and the overall audit strategy etc., the CFO informed that there were no related party transactions during the year. He also acknowledged that management is responsible for identification and disclosure of related parties. In view of the above, the audit senior feels that there is no need to prepare audit program in respect of related parties. Required: Comment on the conclusion drawn by the audit senior and give brief explanation of the auditor’s responsibility in respect of related party transactions. (04 marks) (CA Inter, Autumn 2008) Explain the inherent limitations which mean that auditors may not identify related parties and related party transactions (04 marks) (ACCA P7 – June 2011) LLOO 33:: PPRROOCCEEDDUURREESS TTOO EENNSSUURREE AALLLL RREELLAATTEEDD PPAARRTTYY RREELLAATTIIOONNSSHHIIPPSS AANNDD TTRRAANNSSAACCTTIIOONNSS AARREE IIDDEENNTTIIFFIIEEDD AANNDD DDIISSCCLLOOSSEEDD IINN FFIINNAANNCCIIAALL SSTTAATTEEMMEENNTTSS:: 1. Auditor shall inquire of management regarding: Identification of related parties, including changes from the prior period Relationships with related parties; and Transactions with related parties 2. Auditor shall inquire management and shall perform other risk assessment procedures to obtain understanding of client’s controls over: Identification, accounting for and disclosure of related party relationships and transactions. Approval of significant transactions with related parties. Approval of significant transactions outside normal course of business. 3. Inquire about affiliation of TCWG, directors and other officers with other entities. 4. Review working papers for previous years for known related parties. 5. Inquire component auditor or predecessor auditor about their knowledge of additional related parties (if applicable). 6. Auditor shall remain alert when inspecting records or documents, including: Bank and legal confirmations obtained as part of the auditor’s procedures; Minutes of meetings of shareholders and of those charged with governance; and Such other records or documents as the auditor considers necessary in the circumstances e.g. o Third-party confirmations (in addition to bank and legal confirmations). o Register of shareholders to identify principal shareholders, o Entity’s income tax return and other information supplied to regulatory bodies. o Records of the entity’s investments and those of its pension plans o Significant contracts and agreements not in the entity’s ordinary course of business. o Register of directors/officers, o Significant contracts re-negotiated by the entity during the period, o Published documents by company (e.g. financial statements of prior period, prospectuses). 3 By: Muhammad Asif, ACA

- 4. Auditing – Study Notes Chapter 16 Related Parties CONCEPT REVIEW QUESTION As the auditor of a listed company with a number of related parties, what steps would you consider as part of your audit planning to ensure that all related party relationships and transactions are identified and disclosed in the financial statements. (13 marks) (CA Inter, Autumn 2011) LLOO 44:: RRIISSKKSS IIDDEENNTTIIFFIIEEDD AANNDD AAUUDDIITTOORR’’SS CCOOUURRSSEE OOFF AACCTTIIOONN:: Risk Identified Auditor’s course of action/procedures to address risk Auditor identifies related party relationships or transactions not identified by management: Auditor shall perform following procedures when he identifies a previously unidentified related party relationship/transaction: Promptly communicate the relevant information to other members of engagement. If AFRF establishes related party requirements: Request management to identify all transactions of newly identified related party, and disclose them accordingly. Inquire as to why entity’s process and controls failed to identify or disclose such related party relationship/transaction. Perform appropriate substantive procedures on newly identified related party, and/or significant related party transactions. Reconsider risk that other unidentified related parties may also exist. If non-disclosure appears intentional, Reconsider risk of fraud and other implications on audit. If auditor identifies significant transactions outside the normal course of business. Auditor shall inquire about nature of transactions and shall evaluate whether related party is involved. For identified significant related party transactions, outside the normal course of business, auditor shall: (a) inspect underlying contracts or agreements and shall evaluate whether: i. Transaction is entered to engage in fraudulent financial reporting or misappropriation of assets (lack of business rationale may indicate this). ii. Terms of the transactions are consistent with management’s explanations. iii. Transactions have been appropriately accounted for and disclosed in accordance with the AFRF. (b) Obtain audit evidence that transactions have been appropriately authorized (e.g. by TCWG). If there is a related party with dominant influence*** Any such party may override the views of entity’s management and force entity to enter into a transaction in which dominant party has an interest. If there is a related party with dominant influence, auditor shall inspect significant contracts of entity with such related party. If management states that transactions with related party are on arm’s length. Auditor shall obtain evidence to support this assertion e.g.: by comparing terms of transactions with market terms and conditions. by comparing terms of transactions with unrelated parties. by engaging an expert to evaluate transaction. 4 By: Muhammad Asif, ACA

- 5. Auditing – Study Notes Chapter 16 Related Parties ***Indicators of dominant influence exerted by a related party include: If the related party has played a leading role in founding the entity and continues to play a leading role in managing the entity. Significant transactions are referred to the related party for final approval. The related party has vetoed significant business decisions taken by management or those charged with governance. There is little or no debate among management and those charged with governance regarding business proposals initiated by the related party. Transactions involving the related party are rarely independently reviewed and approved. CONCEPT REVIEW QUESTION Give four examples of situations that may be indicative of dominant influence exerted by a related party. (04 marks) (CA Inter, Autumn 2010) A schedule of related party transactions provided by the client includes two significant transactions which are outside the normal course of business. State the substantive procedures that an auditor should undertake, in respect of these transactions. (04 marks) (CA Inter, Autumn 2015) You are the audit manager on the audit of a listed company, Kamil Limited (KL). Prior to completion of audit, you came across a prospectus issued by Neelum Limited (NL) according to which a director of KL is the chief executive of NL. However, the name of NL was not included in the list of related parties provided by KL. On being confronted the management has advised that the name was omitted inadvertently as the appointment took place just two months prior to the year end. Required: Discuss your course of action in the above situation. (07 marks) (CA Inter, Spring 2015) LLOO 55:: MMAATTEERRIIAALLIITTYY,, WWRRIITTTTEENN RREEPPRREESSEENNTTAATTIIOONN,, CCOOMMMMUUNNIICCAATTIIOONN WWIITTHH TTCCWWGG AANNDD DDOOCCUUMMEENNTTAATTIIOONN:: Materiality: Transactions with related parties are usually considered material irrespective of size of transaction (e.g. sale of company’s assets to related party at nominal amount). Written Representation: If AFRF establishes related party requirements, auditor shall obtain written representations from management (and TCWG where appropriate) that: 1. They have disclosed to the auditor the identity of the entity’s related parties and all the related party relationships and transactions of which they are aware 2. They have appropriately accounted for and disclosed such relationships and transactions in financial statements in accordance with the requirements of the framework. Communication with TCWG: Auditor shall communicate TCWG significant matters regarding Related Parties e.g: Non-disclosure (whether intentional or not) by management to the auditor of significant related party relationships or transactions. 5 By: Muhammad Asif, ACA

- 6. Auditing – Study Notes Chapter 16 Related Parties significant related party transactions that have not been appropriately authorized and approved Disagreement with management regarding the accounting for and disclosure of significant related party transactions in accordance with AFRF. Non-compliance with laws and regulations (e.g. entering in prohibited transactions with related parties) Documentation: The auditor shall include in the audit documentation: Names of identified related parties Nature of relationships with related parties 6 By: Muhammad Asif, ACA