INTRODUCTION TO ASSURANCE SERVICES

•

1 like•158 views

LET SEE AND GET INFORMATION FROM IT

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to INTRODUCTION TO ASSURANCE SERVICES

Similar to INTRODUCTION TO ASSURANCE SERVICES (20)

More from MUHAMMAD HUZAIFA CHAUDHARY

More from MUHAMMAD HUZAIFA CHAUDHARY (20)

Recently uploaded

Recently uploaded (20)

INTRODUCTION TO ASSURANCE SERVICES

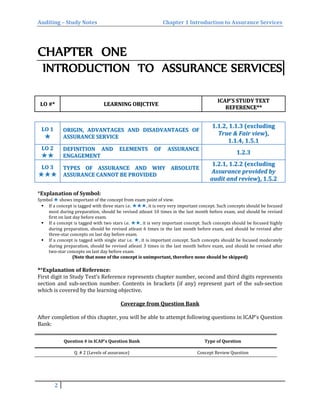

- 1. Auditing – Study Notes Chapter 1 Introduction to Assurance Services CHAPTER ONE INTRODUCTION TO ASSURANCE SERVICES LLOO ##** LLEEAARRNNIINNGG OOBBJJCCTTIIVVEE IICCAAPP''SS SSTTUUDDYY TTEEXXTT RREEFFEERREENNCCEE**** LLOO 11 ✯✯ OORRIIGGIINN,, AADDVVAANNTTAAGGEESS AANNDD DDIISSAADDVVAANNTTAAGGEESS OOFF AASSSSUURRAANNCCEE SSEERRVVIICCEE 11..11..22,, 11..11..33 ((eexxcclluuddiinngg TTrruuee && FFaaiirr vviieeww)),, 11..11..44,, 11..55..11 LLOO 22 ✯✯✯✯ DDEEFFIINNIITTIIOONN AANNDD EELLEEMMEENNTTSS OOFF AASSSSUURRAANNCCEE EENNGGAAGGEEMMEENNTT 11..22..33 LLOO 33 ✯✯✯✯✯✯ TTYYPPEESS OOFF AASSSSUURRAANNCCEE AANNDD WWHHYY AABBSSOOLLUUTTEE AASSSSUURRAANNCCEE CCAANNNNOOTT BBEE PPRROOVVIIDDEEDD 11..22..11,, 11..22..22 ((eexxcclluuddiinngg AAssssuurraannccee pprroovviiddeedd bbyy aauuddiitt aanndd rreevviieeww)),, 11..55..22 *Explanation of Symbol: Symbol ✯✯ shows important of the concept from exam point of view. If a concept is tagged with three stars i.e. ✯✯✯✯✯✯, it is very very important concept. Such concepts should be focused most during preparation, should be revised atleast 10 times in the last month before exam, and should be revised first on last day before exam. If a concept is tagged with two stars i.e. ✯✯✯✯, it is very important concept. Such concepts should be focused highly during preparation, should be revised atleast 6 times in the last month before exam, and should be revised after three-star concepts on last day before exam. If a concept is tagged with single star i.e. ✯✯, it is important concept. Such concepts should be focused moderately during preparation, should be revised atleast 3 times in the last month before exam, and should be revised after two-star concepts on last day before exam. ((NNoottee tthhaatt nnoonnee ooff tthhee ccoonncceepptt iiss uunniimmppoorrttaanntt,, tthheerreeffoorree nnoonnee sshhoouulldd bbee sskkiippppeedd)) ***Explanation of Reference: First digit in Study Text’s Reference represents chapter number, second and third digits represents section and sub-section number. Contents in brackets (if any) represent part of the sub-section which is covered by the learning objective. Coverage from Question Bank After completion of this chapter, you will be able to attempt following questions in ICAP's Question Bank: Question # in ICAP’s Question Bank Type of Question Q. # 2 (Levels of assurance) Concept Review Question 2

- 2. Auditing – Study Notes Chapter 1 Introduction to Assurance Services LLOO 11:: OORRIIGGIINN,, AADDVVAANNTTAAGGEESS AANNDD DDIISSAADDVVAANNTTAAGGEESS OOFF AASSSSUURRAANNCCEE SSEERRVVIICCEESS:: ✯✯ Origin of Assurance Services: Since the Industrial Revolution in 18th century, businessmen started forming Joint Stock Companies to do business. In most situations, people who managed the company (called management and directors) were separate from those who owned the company (called shareholders). Management and Directors had role of stewardship (i.e. management wisely look after the assets of the company on behalf of shareholders) and role of agent (i.e. management act in accordance with instructions of shareholders). To judge the performance of management and directors, shareholders asked them to prepare and present them financial statements. Soon after, it was recognized that financial statements prepared by management/directors presented “best-view” of business instead of “true-and-fair-view” due to some Incentive (e.g. bonus) or Pressure (e.g. fear of removal) faced by management. Thus credibility of financial statements was questioned. To enhance the credibility/confidence/assurance on these financial statements, an expert person (called assurance provider or auditor) was hired by shareholders to verify financial statements. This person is independent of both management and shareholders. Advantages of Assurance Services: An assurance engagement may be performed not only to meet statutory requirements, but there are also some other value-added advantages. For Shareholders: 1. Financial statements are more reliable for decision making because most of the misstatements will be detected during audit. 2. Minority shareholders (or sleeping partners) will have assurance that their interest is protected. For Directors/Management: An audit improves a company’s governance i.e. 1. Audit identifies deficiencies in entity’s internal control system and assurance providers suggest recommendations for improvement through Management Letter. 2. Audit acts as a check on employees; thereby positive behavior increases and risk of fraud is reduced. 3. Audit assures that management is performing its statutory duties. For Third Parties: An audit also provides facilities to third parties in their dealings with company e.g. 1. To prospective investors in purchase of Business or Shares. 2. To banks in granting loan. 3. To tax authorities in ascertaining tax liability. 4. To insurance companies in settlement of insurance claims Disadvantages of Assurance Services: 1) Audit takes cost and time of client. 2) Entity has to share its confidential information with auditor. 3) Management/Directors often think audit as a “disturbing activity” instead of a “value added activity”. 2 By Muhammad Asif, ACA

- 3. Auditing – Study Notes Chapter 1 Introduction to Assurance Services 4) Audit does not provide 100% (i.e. absolute) assurance, therefore, there is still some risk that errors or fraud may exist. 5) Terminology used in audit report is not usually understood by non-accountants which causes misunderstanding among stakeholders (e.g. terms of “reasonable assurance”, “material”, “misstatement”, “true and fair”, “test basis”, “accounting principles”) 6) Audit is of little value if shareholders are actively involved in management. Services of auditors were appreciated greatly. Now a days, assurance engagements are performed either because: they are required by law (called statutory assurance engagements e.g. all companies in Pakistan are required by law to get their annual financial statements audited before they are given to shareholders) they are not required by law but are voluntarily performed (called non-statutory assurance engagements e.g. sole-proprietorships, partnerships and NGOs etc. conducting an audit) CONCEPT REVIEW QUESTION What are the advantages of an audit to an organization? (05 marks) (CA Inter – Spring 2004) List six benefits to organizations, which are exempt from the statutory audit, of voluntarily undergoing an external audit. (ICAEW – December 2007) LLOO 22:: DDEEFFIINNIITTIIOONN AANNDD EELLEEMMEENNTTSS OOFF AASSSSUURRAANNCCEE EENNGGAAGGEEMMEENNTT:: ✯✯✯✯ Assurance Engagement: “Assurance engagement” means an engagement in which a practitioner obtains evidence about evaluation of a subject matter against suitable criteria, and expresses his conclusion to enhance the confidence of the intended users (other than the responsible party). Elements of Assurance Engagement: Every assurance engagement consists of following 5 elements: Element Explanation (with respect to assurance on financial statements) A three party relationship 1. Intended users (the parties who require subject matter and assurance report e.g. shareholders, bankers) 2. A responsible party (the party which is responsible for preparation of subject matter i.e. management) and 3. A practitioner (the professional who verifies subject matter and provides assurance on it i.e. auditor) A subject matter Subject matter is the data which responsible party prepares and is to be verified e.g. Financial Statements A Suitable Criteria Criteria means Framework (i.e. standard rules and regulations) which is used to prepare and evaluate financial statements e.g. IFRS or Tax Laws. Suitable means it should be selected appropriately. Evidence Evidence means information on which practitioner’s conclusion is based. Evidence should be sufficient and appropriate. 3 By Muhammad Asif, ACA

- 4. Auditing – Study Notes Chapter 1 Introduction to Assurance Services Written Assurance Report It is a page written in standard format which includes conclusion of practitioner. It is provided by practitioner to intended users e.g. Report on audit of financial statements, or Report on review of financial statements. CONCEPT REVIEW QUESTION Explain the five elements of an assurance engagement (05 marks) (ACCA F8 – June 2013) LLOO 33:: LLEEVVEELLSS OOFF AASSSSUURRAANNCCEE AANNDD WWHHYY AABBSSOOLLUUTTEE AASSSSUURRAANNCCEE CCAANNNNOOTT BBEE PPRROOVVIIDDEEDD:: ✯✯✯✯✯✯ “Assurance” means confidence with which a practitioner expresses his conclusion. Assurance adds credibility in financial statements, however level of credibility depends on type of assurance provided. Levels/Types of Assurance: There are two levels of assurance that can be provided to assurance client i.e. Reasonable Assurance and Limited Assurance. Reasonable Assurance (also called High Level or Positive Assurance) It is a high but not absolute level of assurance which is expressed in positive form of conclusion i.e. “in our opinion, financial statements give true and fair view”. This is usually given in an audit of financial statements. Concept of reasonable assurance acknowledges that there is still some risk that audit opinion can be wrong because of inherent limitations of audit. Limited Assurance (also called Moderate Level or Negative Assurance) It is a moderate level of assurance which is expressed in negative form of conclusion i.e. “Based on our review, nothing has come to our attention that causes us to believe that financial statements do not give true and fair view”. This is usually given in a review of financial statements. Why absolute assurance cannot be provided to an assurance client: Auditor cannot provide absolute assurance because of inherent limitations of assurance/audit. These limitations are discussed below: 1. Some accounts in financial statements involve estimates / judgments/ uncertainties which are difficult to calculate and verify (e.g. Provision for bad debts, Depreciation, Outcomes of legal cases, Warranty expenses, Intangible assets.) 2. There are always some limitations/weaknesses in internal control system of client. 3. Many of the audit procedures based on auditor’s judgment which can be faulty. 4. Because of time and cost limitation, auditor checks only a sample of transactions. 5. Fraud involving collusion and complex techniques are harder to detect. 6. Management may not provide complete information to auditor. 7. Auditor does not have specific legal powers e.g. power to search. 8. Most of the evidence is persuasive rather than conclusive. 4 By Muhammad Asif, ACA

- 5. Auditing – Study Notes Chapter 1 Introduction to Assurance Services CONCEPT REVIEW QUESTION (a) What is meant by reasonable assurance? (02 marks) (b) Why an auditor cannot provide an absolute assurance as a result of audit? Explain. (03 marks) (CA Inter -Autumn 2004) Distinguish between absolute and reasonable assurance. Identify the type of assurance that is expected in an audit of the financial statements, clearly outlining the reasons to justify your point of view. (08 marks) (CA Inter -Spring 2009) “An unmodified audit report is not a guarantee that the financial statements are free from material misstatements”. Discuss the rationale of this statement. (06 marks) (CA Inter -Spring 2007) Explain why audit risk cannot be reduced to zero. (02 marks) (ICAEW - December 2008) Is an auditor responsible for the detection and disclosure of every error and fraud? Discuss. (06 marks) (CA Inter -Autumn 2003) 5 By Muhammad Asif, ACA

- 6. Auditing – Case Studies Chapter 1 Introduction to Assurance Services CHAPTER ONE (Attempting Case Studies) INTRODUCTION TO ASSURANCE SERVICES AAPPXX 11:: CCAASSEE SSTTUUDDYY RREELLAATTIINNGG TTOO NNEECCEESSSSAAIITTYY,, AADDVVAANNTTAAGGEESS AANNDD DDIISSAADDVVAANNTTAAGGEESS OOFF AASSSSUURRAANNCCEE SSEERRVVIICCEE:: Structure of the Case: In exam, you may be required to comment on necessity, advantages or disadvantages of performing assurance service in a given situation. Suggested Approach to Answer: Before attempting question, carefully note: From whose perspective you are required to comment (whether shareholders, directors or bankers etc.) What you are required to comment (whether necessity, advantages or disadvantages). Model Case Study From Examination Questions: Case Study: You are the auditor of Royale Limited, a manufacturer of fireworks. Following a disappointing last three months of trading, the company has requested an extension to its overdraft facility from its bankers. The bank has in turn asked your firm to carry out an assurance engagement on financial statements of company. Explain the benefits and limitations to both the bank and Royale Limited of obtaining the assurance report. (04 marks) (ICAEW Professional Stage – March 2006) Suggested Solution: Benefits to Bank: Independent assurance report increases credibility of financial statements. Bank can better analyze liquidity and solvency position of company as well as appropriateness of value of securities. Limitation for Bank: Assurance is not absolute. There is still some risk of misstatement in financial statements. Benefits to Royale Limited: Help in approval and quick processing of loan. Limitation for Royale Limited: Assurance will take cost and time of Royal Limited. 1 By Muhammad Asif, ACA