Legal requirements (revised notes and case studies) - COMPLIANCE WITH LEGAL REQUIREMENTS

•

1 like•548 views

LET SEE AND GET INFORMATION FROM IT

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Legal requirements (revised notes and case studies) - COMPLIANCE WITH LEGAL REQUIREMENTS

Similar to Legal requirements (revised notes and case studies) - COMPLIANCE WITH LEGAL REQUIREMENTS (20)

More from MUHAMMAD HUZAIFA CHAUDHARY

More from MUHAMMAD HUZAIFA CHAUDHARY (20)

Recently uploaded

Recently uploaded (20)

Legal requirements (revised notes and case studies) - COMPLIANCE WITH LEGAL REQUIREMENTS

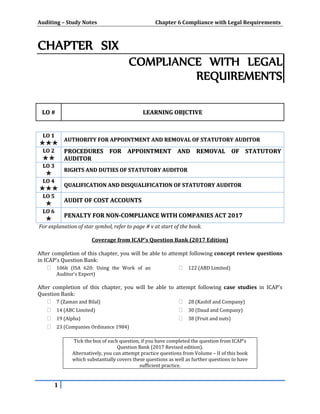

- 1. Auditing – Study Notes Chapter 6 Compliance with Legal Requirements CHAPTER SIX COMPLIANCE WITH LEGAL REQUIREMENTS LLOO ## LLEEAARRNNIINNGG OOBBJJCCTTIIVVEE LLOO 11 ✯✯✯✯✯✯ AAUUTTHHOORRIITTYY FFOORR AAPPPPOOIINNTTMMEENNTT AANNDD RREEMMOOVVAALL OOFF SSTTAATTUUTTOORRYY AAUUDDIITTOORR LLOO 22 ✯✯✯✯ PPRROOCCEEDDUURREESS FFOORR AAPPPPOOIINNTTMMEENNTT AANNDD RREEMMOOVVAALL OOFF SSTTAATTUUTTOORRYY AAUUDDIITTOORR LLOO 33 ✯✯ RRIIGGHHTTSS AANNDD DDUUTTIIEESS OOFF SSTTAATTUUTTOORRYY AAUUDDIITTOORR LLOO 44 ✯✯✯✯✯✯ QQUUAALLIIFFIICCAATTIIOONN AANNDD DDIISSQQUUAALLIIFFIICCAATTIIOONN OOFF SSTTAATTUUTTOORRYY AAUUDDIITTOORR LLOO 55 ✯✯ AAUUDDIITT OOFF CCOOSSTT AACCCCOOUUNNTTSS LLOO 66 ✯✯ PPEENNAALLTTYY FFOORR NNOONN--CCOOMMPPLLIIAANNCCEE WWIITTHH CCOOMMPPAANNIIEESS AACCTT 22001177 For explanation of star symbol, refer to page # v at start of the book. Coverage from ICAP’s Question Bank (2017 Edition) After completion of this chapter, you will be able to attempt following concept review questions in ICAP's Question Bank: 106b (ISA 620: Using the Work of an Auditor’s Expert) 122 (ABD Limited) After completion of this chapter, you will be able to attempt following case studies in ICAP's Question Bank: 7 (Zaman and Bilal) 14 (ABC Limited) 19 (Alpha) 23 (Companies Ordinance 1984) 28 (Kashif and Company) 30 (Daud and Company) 38 (Fruit and nuts) Tick the box of each question, if you have completed the question from ICAP’s Question Bank (2017 Revised edition). Alternatively, you can attempt practice questions from Volume – II of this book which substantially covers these questions as well as further questions to have sufficient practice. 1

- 2. Auditing – Study Notes Chapter 6 Compliance with Legal Requirements LLOO 11:: AAPPPPOOIINNTTMMEENNTT AANNDD RREEMMOOVVAALL OOFF SSTTAATTUUTTOORRYY AAUUDDIITTOORR:: ✯✯✯✯✯✯ Appointing Authority for Auditor: Appointment of first auditor: First auditor is appointed by Board of Directors within 90 days of incorporation. Appointment of subsequent auditor: Subsequent auditor is appointed by company at each AGM (on recommendation of the board). Appointment in case of casual vacancy: Casual vacancy (i.e. death or disqualification of auditor during audit) is filled by directors within 30 days of its occurrence. Appointment in case of mid-term removal of auditor: If auditor is removed before expiry of his term, board of directors shall appoint the auditors with prior approval of the Commission. If a disqualified person is appointed by company: If a disqualified person is appointed as auditor, this appointment shall be void, and SECP will appoint qualified auditor in his place. Appointment by SECP/Commission: Commission may (on its own, or on application by company or any member) direct company to make good the default if: 1. the company fails to appoint the first auditors within ninety days of incorporation, or 2. the company fails to appoint subsequent auditors at an annual general meeting; or 3. the company fails to fill up a casual vacancy within thirty days of occurrence of the vacancy; or 4. the appointed auditors are unwilling to act as auditors of the company; If the company does not comply order within specified time, the Commission shall appoint auditors of the company. Tenure/Term of Auditor: Tenure of auditor appointed in each case is from date of appointment till the conclusion of next AGM. Mid-Term Removal of Auditor: (i.e. removal before expiry of tenure) An auditor, whether appointed by Directors or appointed by Members, can be removed before expiry of his term by members through Special Resolution. Remuneration of Auditor: The remuneration of the auditor shall be fixed: (a) by the company in the general meeting; or (b) by the board or by the Commission, if the auditors are appointed by the board or the Commission, as the case may be. 2

- 3. Auditing – Study Notes Chapter 6 Compliance with Legal Requirements CONCEPT REVIEW QUESTION Write short notes on the following: - Appointment of first auditors. (03) (ICAP, CAF 03 Level – Autumn 2003) State the circumstances in which the auditors may be appointed by the directors and by the members of a company. (03) (Institute of Chartered Accountants in England and Wales, Professional Level – December 2001, Amended) Narrate the circumstances in which SECP becomes empowered to appoint auditors under the Companies Act, 2017. (06) (ICAP, CAF 03 Level – Spring 2008) Can auditor of a listed company be removed during the term of his office? (02) (ICAP, CAF 09 Level – Spring 2002) LLOO 22:: PPRROOCCEEDDUURREESS FFOORR AAPPPPOOIINNTTMMEENNTT AANNDD RREEMMOOVVAALL OOFF SSTTAATTUUTTOORRYY AAUUDDIITTOORR:: ✯✯✯✯ Legal Procedure for Removal/Appointment/Change of Statutory Auditor at AGM: 1. Board of Directors shall recommend auditors, after obtaining consent of proposed auditors. A notice of recommendation shall be sent to members with the notice of AGM. 2. A member or members (having 10% or more shareholding in company) can also propose an auditor, provided: a. consent of proposed auditors has been obtained by member, and b. member has sent a notice in this regard to company atleast 7 days before AGM. Company shall send copy of this notice to retiring auditor and shall also post on its website. 3. Retiring auditor has a right to make a representation in writing to company atleast two days before the date of general meeting. If such a representation in writing is made by retiring auditor: a. It shall be read out at AGM before taking up the agenda for appointment of the auditor. b. it shall be mandatory for the auditor or a person authorized by him in writing to attend the general meeting. 4. At AGM, members will pass a resolution to appoint auditor from proposed auditors. 5. Within 14 days of appointment of auditor, company shall send Registrar intimation of appointment of auditor alongwith written consent of appointed auditor. Ethical Responsibilities when there is change of auditor: Responsibilities of Incoming (Proposed/Successor) Auditor: 1. Incoming auditor shall send professional clearance letter to outgoing auditor to ensure that incoming auditor knows and considers all relevant facts of client before making decision to accept. 2. Incoming auditor shall obtain a copy of the Representation before acceptance (if made by retiring auditor). 3. Additional responsibility if predecessor auditor is removed during audit, Incoming auditor should also inform ICAP about the offer of appointment. Incoming auditor should not accept offer of appointment without prior clearance from ICAP. ICAP usually gives clearance within 15 days. Responsibilities of Outgoing (Existing/Predecessor) Auditor: 1. To maintain confidentiality (even after change of appointment). 3

- 4. Auditing – Study Notes Chapter 6 Compliance with Legal Requirements 2. To transfer all books and papers of client (to client or to incoming auditor if advised so by client). 3. To reply promptly to incoming auditor’s Professional Clearance Letter. 4. Outgoing auditor will file with ICAP a copy of Representation (if made). 5. Additional responsibility if predecessor auditor is removed during audit, he must immediately file with ICAP a “Statement of Facts/Circumstances”. CONCEPT REVIEW QUESTIONS Describe the procedure prescribed in the Companies Ordinance, 1984 for removal of auditor of a listed company. (06) (ICAP, CAF 09 Level – Spring 2002) Set out the responsibilities of the outgoing firm of auditors relating to the change of appointment in order to comply with the ICAEW Code of Ethics. (06) (Institute of Chartered Accountants in England and Wales, Professional Level – 2007 June) On March 15, 2006, Karom Textile Limited received a notice from a shareholder of the company nominating another firm of Chartered Accountants as auditors in place of the existing auditors at the annual general meeting to be held on March 31, 2006. Explain the conditions required to be fulfilled by a member of the company while making such nomination under the Companies Act, 2017. Also describe the company’s responsibilities on receiving such notice, towards other members and the existing auditors of the company. (05) (ICAP, CAF 03 Level – Autumn 2006) LLOO 33:: RRIIGGHHTTSS AANNDD DDUUTTIIEESS OOFF SSTTAATTUUTTOORRYY AAUUDDIITTOORR:: ✯✯ Statutory Rights of Auditor: Auditors’ right to information 1. An auditor of a company has a right: of access to the company‘s books, accounts and vouchers (in whatever form they are held). of access to copies of books, accounts and vouchers of branches (transmitted to principal office). to require any director, officer or employee of the company or its subsidiary to provide him with such information and explanation as he thinks necessary for the purpose of audit. Rights with regard to the general meeting: 2. Right to receive all notices of any general meetings which members of company are entitled to receive. 3. Right to attend general meetings. However, in case of listed company, it is duty of auditor or a person authorized by him in writing to attend general meeting in which financial statements and auditor’s report are considered. 4. Right to speak at general meetings on audit related matters. 5. Right to make representation in writing if change of auditor is proposed. Exam Tip In exam question, be careful whether question relates: Legal procedures or Ethical procedures. Change of auditor during tenure or at end of tenure. Course of Action by Incoming auditor or Outgoing auditor. 4

- 5. Auditing – Study Notes Chapter 6 Compliance with Legal Requirements Statutory Duties of Auditor: 1. A company‘s auditor shall conduct the audit and prepare his report in accordance with the requirements of ISAs as adopted by ICAP. 2. A company‘s auditor shall examine whether: a. adequate records have been kept and returns have been received by company from branches not visited by him. b. accounting records and returns are in agreement with financial statements. 3. The auditor shall make a report to the members of the company which shall state: (a) whether or not they have obtained all the information and explanations which to the best of their knowledge and belief were necessary for the purposes of the audit; and if not, the details and effect of such information on financial statements. (b) whether or not in their opinion, proper books of accounts have been kept by the company as required by the Companies Act, 2017. (c) whether or not in their opinion, the ‘statement of financial position’ and ‘profit and loss account and other comprehensive income’ (or income and expenditure account) and cash flows have been drawn up in conformity with the requirements of accounting and reporting standards as notified under the Companies Act , 2017, and are in agreement with the books of accounts and are further in accordance with accounting policies consistently applied; (d) whether or not in their opinion and to the best of their information and according to the explanations given to them,: (i) Statement of financial position give a true and fair view of state of affairs of company at end of financial year. (ii) Profit and loss account and other comprehensive income give a true and fair view of profit or loss (or surplus or deficit) for its financial year. (iii) Statement of cash flows give a true and fair view of generation and utilization of cash and cash equivalents of the company for its financial yr. (e) whether or not in their opinion (i) investments made, expenditure incurred and guarantees extended, during the year, were for the purpose of company’s business. (ii) zakat deductible at source under the Zakat and Ushr Ordinance, 1980, was deducted by the company and deposited in the Central Zakat Fund established under that Ordinance. If any of the above matters is answered in “negative” or in “qualification”; auditor shall state its reason with factual position in auditor’s report. Signing of Audit Report: Audit report shall be signed, dated and shall indicate the place at which it is signed. If the auditor is an individual, report shall be signed by him. If the auditor is a firm, report shall be signed by firm, with the name of engagement partner. CONCEPT REVIEW QUESTION What are the rights and duties of an auditor under the Companies Ordinance, 1984? (10) (ICAP, CAF 09 Level – Spring 2000) Your firm has received notice from Ash plc (Ash), a listed company, that your firm will not be re-appointed as external auditor when its term of office expires as the audit committee of Ash has recommended the appointment of another firm. Set out the rights and responsibilities of your firm, including those under the Companies Ordinance 1984, relating to the change in appointment. (03) (Institute of Chartered Accountants in England and Wales, Professional Level – 2016 June, amended) 5

- 6. Auditing – Study Notes Chapter 6 Compliance with Legal Requirements (a) What are the provisions of the Companies Act, 2017, regarding remuneration of auditors of a company. (03) (b) What are the provisions of Companies Act, 2017 regarding auditors signature on audit report? (03) (ICAP, CAF 03 Level – Autumn 2001) LLOO 44:: QQUUAALLIIFFIICCAATTIIOONN AANNDD DDIISSQQUUAALLIIFFIICCAATTIIOONN OOFF SSTTAATTUUTTOORRYY AAUUDDIITTOORR:: ✯✯✯✯✯✯ In Pakistan, annual audit is required for all types of companies, except a private company having paid up capital of one million or less. Qualification Criteria: Audit of a Public Company, or a Private company which is subsidiary of a public company, or a private company with paid up capital of Rs. 3 million or more, shall be conducted by a chartered Accountant or a firm of chartered accountants (having valid certificate of practice from ICAP). Audit of other companies shall be conducted by: a chartered Accountant or a firm of chartered accountants (having valid certificate of practice from ICAP), or a cost and management accountant or firm of cost and management accountants (having valid certificate of practice from ICMAP) Disqualification Criteria: Following persons shall not be appointed as auditor in a company: 1. A person or his spouse or minor child holds any shares in the audit client or any of its associated company. However, if such a person holds shares at time of appointment, he can be appointed if he discloses the fact at time of appointment and disinvest shares within 90 days of appointment. 2. A person is indebted to the company, other than in ordinary course of business of such entities. However following are not considered debt in this regard: a. sum payable to a credit card issuer upto Rs. 1,000,000. b. sum payable to a utility company unpaid upto 90 days. 3. If a person is or was an employee (or officer or director) of the company in last 3 years. 4. If a person is a partner or employee of an employee (or officer or director) of the company. 5. If a person is Spouse of a director. 6. If a person is a Body corporate. 7. A person who has given guarantee or security to the company in connection with the indebtedness of third person. 8. A person or firm who has business relationship with the company (directly or indirectly), other than in ordinary course of business of such entities. 9. A person who has been convicted by a Court of an offence involving fraud in last 10 years. 10. A person who is not eligible for appointment as auditor under Code of Ethics adopted by ICAP and ICMAP. If a person is disqualified for a company, he is also disqualified for its subsidiaries, its holding, and holding’s other subsidiaries. Therefore, always be sure about status if question involves two companies. Exam Tips A firm can be appointed as auditor if majority of its partners are qualified for appointment. However, only a qualified person can act as auditor or can sign on behalf of firm. 6

- 7. Auditing – Study Notes Chapter 6 Compliance with Legal Requirements CONCEPT REVIEW QUESTION The Directors of Sunshine Limited, a listed company, intend to appoint the first auditors of the company. In view of the provisions of the Companies Act 2017, advise the directors in respect of the following: (i) The time frame within which the first auditors should be appointed. (ii) The person(s) who may or may not be eligible for appointment as auditor(s). (10) (ICAP, CAF 03 Level – Autumn 2014) LLOO 55:: AAUUDDIITT OOFF CCOOSSTT AACCCCOOUUNNTTSS:: ✯✯ Cost Accounting Records: A company engaged in production, processing, manufacturing or mining activities is required to keep prescribed particulars relating to following cost accounting records: 1. Utilisation of Material, 2. Utilisation of Labour, 3. Utilisation of Other inputs or items of cost. Audit of Cost Accounting Records: Where a company is required to keep Cost Accounting records, Commission may direct (subject to the recommendation of the regulatory authority supervising the business of relevant sector) that an audit of cost accounts of the company shall be conducted in the manner as may be specified in the order. Audit of cost accounts shall be conducted by an auditor who is a: Chartered accountant within the meaning of the Chartered Accountant Ordinance, 1961, or Cost and management accountant within the meaning of the Cost and Management Accountants Act, 1966. Such auditor shall have the same powers, duties and liabilities as an auditor of the company and such other powers, duties and liabilities as may be prescribed. CONCEPT REVIEW QUESTION Narrate the provisions of the Companies Act, 2017 regarding audit of cost accounts. (04) (ICAP, CAF 03 Level – Autumn 2006) Exam Tips 1. All conditions of disqualification apply at time of appointment as well as during term of appointment. 2. Carefully note which relatives are covered in which case of disqualification. 3. Word “Limited” in the name of an organization shows that it is a Company. Similarly, word “Private” in the name confirms that it is a private company. 4. Make sure you know definitions of “Associated Company”, “Holding” and “Subsidiary”. 5. As per Companies Act 2017, auditor means only sole-proprietor/partners of audit firm. 7

- 8. Auditing – Study Notes Chapter 6 Compliance with Legal Requirements LLOO 66:: PPEENNAALLTTYY FFOORR NNOONN--CCOOMMPPLLIIAANNCCEE WWIITTHH CCOOMMPPAANNIIEESS AACCTT 22001177:: ✯✯ Situation Penalty A person who is not qualified (or is subsequently disqualified) to be an auditor of a company, acts as auditor of a company Penalty of Level 2 at Standard Scale i.e. Penalty @ Rs. 1,000 per day subject to maximum of Rs. 500,000. If auditor’s report or review report or any other document is signed/authenticated in contravention of the requirements of the Act, or If auditor’s report or review report or any other document is untrue or fails to bring out material facts about the affairs of the company Penalty of Level 2 at Standard Scale i.e. Penalty @ Rs. 1,000 per day subject to maximum of Rs. 500,000. If the auditor’s report is made with the intent to profit the auditor or any other person or to put another person to a disadvantage or loss or for a material consideration Penalty of Level 2 at Standard Scale i.e. Penalty @ Rs. 1,000 per day subject to maximum of Rs. 500,000. + Auditor shall be punishable with imprisonment for a term which may extend two years and with a penalty which may extend to one million rupees. If company or an officer of company refuses or fails (without lawful justification): to allow auditor access to books and papers in his custody or to provide auditor information and explanation required by him or obstructs or delays an auditor in performance of his duties or fails to give notice of a general meeting to auditor, or provides false or incorrect information Penalty of Level 3 at Standard Scale i.e. Penalty @ Rs. 500,000 per day subject to maximum of Rs. 100,000,000. 8

- 9. Auditing – Case Studies Chapter 6 Compliance with Legal Requirements CHAPTER SIX (CASE STUDIES) COMPLIANCE WITH LEGAL REQUIREMENTS AAPPXX 11:: SSTTEEPP--WWIISSEE AAPPPPRROOAACCHH TTOO SSOOLLVVEE CCAASSEE SSTTUUDDYY FFOORR AAPPPPOOIINNTTMMEENNTT OOFF AAUUDDIITTOORR ((LLEEGGAALL ++ EETTHHIICCAALL)):: ✯✯✯✯✯✯ Structure of the Case: You may be given different short situations and requirement will be to comment on appointment/qualification/independence of statutory auditor in each situation. Suggested Approach to Answer: Decide whether it is a situation of legal requirements or ethical requirements: If words like “Companies Ordinance”, “Legal”, “Statutory” are used, apply legal provisions. If words like “Code of Ethics”, “Ethical”, “Threats, Safeguards” are used apply ethical provisions. If words “applicable rules and regulation” are used, apply legal provision if situation is discussed in law. Otherwise, apply ethical provisions. Remember: In exam, both (legal and ethical) regulations are not discussed in a single situation. If question relates to legal requirements: 1. There may be THREE issues involved in the case: a. Whether appointment is made by appropriate authority. b. Whether qualification criteria is complied. c. Whether disqualification criteria is complied. 2. If appointment is not appropriate on more than one grounds, you will cover BOTH one by one. 3. Whatever is the case, do not reproduce provision of law; rather state your decision by directly applying legal provisions to the facts of case. (this is because usually 2 or 3 marks only are allocated to each case of legal provisions in exam question) If question relates to ethical requirements: When faced with an ethical conflict, a chartered accountant should consider relevant facts of the situation and should: 1. Identify threat(s) involved in the situation. 2. Evaluate threat (i.e. whether significant or insignificant). 3. Apply relevant safeguards (or course of actions) to reduce threat to acceptable level. 4. All ethical issues and relevant considerations should be documented. If a significant ethical conflict/threat cannot be resolved, chartered accountant should consider withdrawal from engagement, if possible and practicable. 1

- 10. Auditing – Case Studies Chapter 6 Compliance with Legal Requirements Model Case Study From Examination Questions: Case Study – First Example Comment on each of the following situations with reference to the appointment of external auditors in accordance with the requirements of the Companies Act, 2017: (a) Farrukh & Co., Chartered Accountants, has received an offer to be appointed as the external auditor of Ebrahim Gas Company. The firm is indebted to the company as it has not paid the last two months’ bills amounting to Rs. 4,860. (b) After seventy days of incorporation, the directors of Rahman Limited (RL) decided to appoint Mr. Shahid as the company’s statutory auditor. Mr. Shahid was employed by RL before he started his own practice. (c) The directors of Fazal Limited (FL) have decided to appoint Syed & Company, Chartered Accountants, as external auditor of the company. One of the partner’s spouse holds 1,000 shares in the subsidiary of FL. (d) The directors of Najam (Pvt.) Limited having paid-up capital of Rs. 4.5 million have appointed Mr. Dawood to act as the external auditor of the company. Mr. Dawood has been awarded a diploma in International Financial Reporting Standards by the Institute of Chartered Accountants of Pakistan and has completed the mandatory period of training from a leading firm of chartered accountants. (e) All directors of Hussain Associates (Pvt.) Limited are chartered accountants. The company has recently received an offer for appointment as the external auditor of Masood (Pvt.) Limited which has a paid-up share capital of Rs. 1,000,000. (10 marks) (ICAP, CAF 09 Level – Spring 2010) Suggested Solution: (a) Farrukh & Co. can be appointed as statutory auditor of Ebrahim Gas Company because the firm is not indebted to the company as the sum payable to utility company does not exceed period of 90 days. (b) Although, directors have power to appoint first auditor within 90 days of incorporation; however, Mr. Shahid cannot be appointed as statutory auditor of RL because he has been an employee of the company in last three years. (c) Syed & Company can be appointed as statutory auditor of FL only if: Shareholding by spouse of partner in associated company of FL is disclosed at time of appointment, and Shares are disinvested within 90 days of appointment. (d) Mr. Dawood cannot be appointed as statutory auditor of Najam (Pvt.) Limited because audit of a private company having paid up capital of three million or more can be conducted only by a chartered accountant (within the meanings of CA Ordinance 1961). (e) Hussain Associates (Pvt) Limited cannot be appointed as statutory auditor of any company because it (auditor) is a body corporate and, therefore, is disqualified. 2

- 11. Auditing – Case Studies Chapter 6 Compliance with Legal Requirements Case Study – Second Example Analyze the following independent situations with reference to qualification of statutory auditor: (i) Mr. Zakir Ali, a practicing chartered accountant, has been offered appointment in Heera Limited as external auditor. He was an employee of the company before he started his own practice. (ii) Diamond Associates (Pvt) Limited, a consultancy company, the majority of whose directors are chartered accountants, have been offered appointment as external auditor in Lal (Pvt) Limited whose share capital is less than Rs. 1.5 million. (iii) Miss Fatima Khan, a practicing chartered accountant, has been offered appointment in Neelam Limited as external auditor. She was an employee of the company’s director two months before the offer. (iv) Mr. Farid Hussain is a partner of Farid & Company, Chartered Accountants. The firm has been offered appointment in Feroza Limited as external auditor. Son of Mr. Farid holds shares of Feroza Limited. (08 marks) (ICAP, CAF 09 Level – Autumn 2006) Suggested Solution: (i) Mr. Zakir Ali can be appointed as auditor of Heera Limited if he has not been an employee of the company in last three years. (ii) Diamond Associates (Pvt) Limited cannot be appointed as statutory auditor of any company because it (auditor) is a body corporate and, therefore, is disqualified. (iii) Miss Fatima Khan can be appointed as statutory auditor of Neelam Limited because she is no more an employee of director of Neelam Limited. (iv) If son of partner is major: Farid & Company can be appointed as statutory auditor of Feroza Limited because there is no violation of law if major son of auditor holds shares in audit client. If son of partner is minor: Firm can be appointed as statutory auditor of Feroza Limited only if: Shareholding of a minor son of partner in audit client is disclosed at the time of appointment, and Share are disinvested within 90 days of appointment. Examiners’ Comments: Legal provisions regarding appointment of statutory auditor is a topic regularly asked and was attempted fairly by most students. The general deficiencies noted in the answers were as follows: • The time lapse after which an ex-employee can become an external auditor was not mentioned. • There were many examinees who said that a private limited company having paid up capital less than rupees three million can appoint, even a body corporate, as its auditors. • There was a general misconception that an ex-employee of a director also needs a time lapse of three years for appointment as an external auditor. • Very few students knew that if shares are held by the minor son of a person, he cannot accept appointment as an external auditor. There is no such restriction if the son has attained the age of majority. 3