Daily Market Report

•

0 likes•260 views

A summary of market activities and stock performance that occurred on the floor of the Nigerian stock exchange at the close of trading activities yesterday.

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (20)

Similar to Daily Market Report

Similar to Daily Market Report (20)

Recently uploaded

Recently uploaded (20)

Daily Market Report

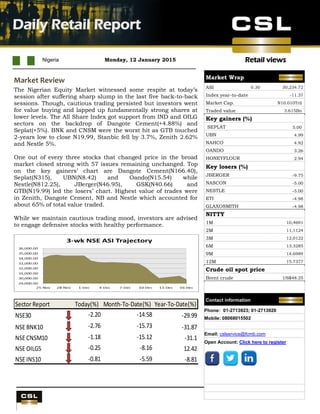

- 1. Retail views UBA Q4 results Nigeria Monday, 12 January 2015 Daily Retail Report . Market Review The Nigerian Equity Market witnessed some respite at today’s session after suffering sharp slump in the last five back-to-back sessions. Though, cautious trading persisted but investors went for value buying and lapped up fundamentally strong shares at lower levels. The All Share Index got support from IND and OILG sectors on the backdrop of Dangote Cement(+4.88%) and Seplat(+5%). BNK and CNSM were the worst hit as GTB touched 2-years low to close N19.99, Stanbic fell by 3.7%, Zenith 2.62% and Nestle 5%. One out of every three stocks that changed price in the broad market closed strong with 57 issues remaining unchanged. Top on the key gainers’ chart are Dangote Cement(N166.40), Seplat(N315), UBN(N8.42) and Oando(N15.54) while Nestle(N812.25), JBerger(N46.95), GSK(N40.66) and GTB(N19.99) led the losers’ chart. Highest value of trades were in Zenith, Dangote Cement, NB and Nestle which accounted for about 65% of total value traded. While we maintain cautious trading mood, investors are advised to engage defensive stocks with healthy performance. Sector Report Today(%) Month-To-Date(%) Year-To-Date(%) NSE30 -2.20 -14.58 -29.99 NSE BNK10 -2.76 -15.73 -31.87 NSE CNSM10 -1.18 -15.12 -31.1 NSE OILG5 -0.25 -8.16 12.42 NSE INS10 -0.81 -5.59 -8.81 Market Wrap ASI 0.30 30,234.72 Index year-to-datee -11.37 Market Cap. N10.010Tril Traded value 3.615Bn Key gainers (%) SEPLAT 5.00 UBN 4.99 NAHCO 4.92 OANDO 3.26 HONEYFLOUR 2.94 Key losers (%) JBERGER -9.75 NASCON -5.00 NESTLE -5.00 ETI -4.98 GLAXOSMITH -4.98 NITTY 1M 10,4691 2M 11,1124 3M 12,0122 6M 13.3285 9M 14.6989 12M 15.7377 Crude oil spot price Brent crude US$48.25 Contact information Phone: 01-2713923; 01-2713920 Mobile: 08068015502 Email: cslservice@fcmb.com Open Account: Click here to register

- 2. Daily Retail Report Page 2 Retail views Stock Recommendations Banking Comment Current Price Target Price Potential Upside % EPS FY 2012 1 Yr forward EPS 1-yr PAT Latest (Nbillion) 1 yr forward PAT(Nbillion) Last year's Dividend(N) Dividend Yield (%) Last year's RoAE % Shares Outstanding (millions) Year End Access Bank Plc Hold 5.23 11.00 110.3% 1.68 1.61 42.862 36.860 0.85 8.80 19.2% 22,883 Dec. Diamond Bank Plc Buy 4.70 8.10 72.3% 1.53 1.64 22.075 23.801 0.00 0.00 22.7% 14,475 Dec. Fidelity Bank Buy 1.48 3.00 102.7% 0.63 0.50 18.201 20.116 0.21 14.19 12.0% 28,974 Dec. First Bank Holding Company Hold 7.80 14.70 88.5% 2.30 2.30 75.400 74.900 1.00 12.82 18.8% 32,632 Dec. Guaranty Trust Bank Plc Buy 19.99 39.80 99.1% 3.06 3.30 90.000 97.400 1.70 8.50 29.0% 29,431 Dec. Stanbic Hold 26.00 15.50 -40.4% 1.02 1.82 11.446 20.300 0.10 0.38 12.4% 10,000 Dec. Sterling Bank Hold 2.49 2.70 8.4% 0.44 0.40 6.954 8.000 0.20 8.03 16.0% 21,592 Dec. Skye Bank under review 2.20 under review N/A 0.96 1.20 12.646 15.182 0.50 22.73 12.0% 13,219 Dec. United Bank for Africa Plc Hold 3.79 7.40 95.3% 1.70 1.50 54.800 49.800 0.50 13.19 32.3% 32,981 Dec. Zenith Bank Plc Buy 16.00 31.50 96.9% 3.19 2.96 95.300 101.800 1.75 10.94 19.5% 31,396 Dec. Food & Beverage Dangote Sugar Refinery under review 5.72 under review N/A 0.89 1.10 10.700 12.800 0.50 8.74 26.0% 12,000 Dec. Cadbury Plc under review 42.00 under review N/A 1.10 3.20 5.500 6.000 0.50 1.19 19.0% 1,878 Dec. Flour Mills Plc Hold 35.38 54.80 54.9% 2.90 3.50 8.400 10.618 1.60 4.52 10.0% 2,385 Mar. Honey Flour Mills Buy 3.15 5.20 65.1% 0.34 0.40 2.702 3.208 0.15 4.76 16.0% 7,930 Dec. Nestle Nig. Plc Hold 812.25 821.80 1.2% 26.70 27.20 22.258 21.768 25.50 3.14 75.0% 792 Dec. PZ Plc Hold 24.54 34.60 41.0% 0.60 1.20 2.400 3.800 0.43 1.00 6.0% 3,970 May UACN Plc Buy 27.60 72.60 163.0% 2.57 2.70 7.100 9.400 1.60 5.80 12.1% 1,920 Dec. Unilever Plc Sell 33.80 31.80 -5.9% 1.51 1.26 5.600 4.800 1.40 4.14 58.0% 3,783 Dec. Building Materials WAPCO under review 80.08 under review N/A 4.90 10.00 14.700 30.009 1.20 1.50 23.0% 3,001 Mar. Dangote Cement Plc Buy 166.40 258.50 55.3% 8.90 11.40 151.900 194.000 3.00 1.50 37.0% 17,040 Dec. Breweries Guinness Sell 130.00 111.00 -14.6% 7.93 8.70 11.863 13.400 7.00 5.38 36.0% 1,506 June International Breweries Hold 21.39 24.50 14.5% 0.71 0.90 2.327 2.800 0.25 1.00 25.0% 3,263 Mar. Nigerian Breweries Plc sell 144.40 121.20 -16.1% 5.00 5.50 38.100 41.012 3.00 2.08 41.0% 7,562 June Agriculture OkomuOil Buy 25.46 41.50 63.0% 7.50 3.50 3.591 3.300 7.00 15.20 16.0% 953 Dec. Presco Buy 27.00 42.70 58.1% 3.55 1.56 3.550 1.556 1.00 2.80 21.0% 1,000 Dec. Pharmaceuticals GlaxoSmithkline Buy 40.66 78.60 93.3% 2.95 3.31 2.824 3.170 1.30 3.20 29.0% 957 Dec. Note – for full report on the recommended stocks kindly send an email to cslcsu@firstcitygroup.com

- 3. Daily Retail Report Page 3 Retail views Top Highlight Violence Early signs of pre-election violence Ahead of the 14 February presidential elections, political violence was reported in several parts of the country over the weekend. Yesterday, an explosion occurred at the All Progressives Congress (APC) secretariat in Rivers State. Local newspapers reported that the blast was caused by unidentified individuals who threw dynamite into the ground floor of the APC secretariat. This was followed shortly by an attack on four members of the APC in another part of the state. Although the APC’s Presidential candidate, Retired Major General Muhammadu Buhari, last week went on a campaign tour of the South East and so-called South South regions, we believe the violence in Rivers was driven more by intra-State politics than the presidential elections. The election violence was however not limited to the South as two campaign buses of President Goodluck Jonathan, whose party is the ruling People’s Democratic Party (PDP), were burned in Plateau State on Saturday. Historically Plateau State has been a political and religious hotbed, though limited cases of violence have been reported of late. While fears have been expressed that violent clashes between rival political parties could flare up in the run-up to elections, there has been a markedly sharp increase in attacks by the Boko Haram group in the last two weeks. It was reported that, following the group’s capture of the town of Baga on 3 January, it went on a killing campaign. It was reported that about 2,000 people have been killed in Baga and neighbouring villages. It is believed that the group is specifically targeting members of the local vigilantes working with security forces. The group is also credited with a bomb blast in Maiduguri, Borno State on Saturday which killed around 19 people and another blast on Sunday in Potiskum, Yobe State, which killed four. While pre-election violence isn’t unusual in the run-up to presidential elections in Nigeria, the scale of attacks appears to be higher than usual this time around. Judging by the level of support for either side, we believe that the upcoming Presidential elections could be the closest since the return to Democracy in 1999. News Headlines SEC announces exit of Oteh as Director-General: The Securities and Exchange Commission (SEC) on Sunday announced the exit of Ms. Arunma Oteh as the commission’s Director-General. The commission made the disclosure in a statement issued by its management and made available to the News Agency of Nigeria (NAN) in Lagos. Source: thisdaylive.com CBN defers implementation of policy on oil sector risk mitigation: The Central Bank of Nigeria (CBN) has postponed an earlier directive that deposit money banks should strengthen their capital buffers in order to mitigate shocks as a result of their exposure to the oil sector. The latest decision is to ensure that the on-going implementation of the Basel II/III capital adequacy framework is not dislocated. Source: thisdaylive.com Nigerian Cocoa processors groan under huge debts: Data gathered by BusinessDay suggests that Nigeria’s Cocoa Processors are paying the price for their un-serviced loans and high input costs, with cost eroding sales. “Many of them are burdened with un-serviced debts estimated collectively at about N40 billion ($241m),” said Akin Olusuyi. Source: businessdayonline.com

- 4. Daily Retail Report Page 4 Retail views Important Risk Warnings and Disclaimers CSL STOCKBROKERS LIMITED (CSLS) is regulated and authorized by the Securities and Exchange Commission (SEC) of Nigeria and the Nigerian Stock Exchange (NSE). The details of the authorization can be viewed at the SEC Website at http://www.sec.gov.ng/consolidated-list-of-capital-market-operators.html and at the NSE Website at http://www.nse.com.ng/Regulation/ForBrokers/Pages/Dealing-Members.asp. RELIANCE ON THIS NOTE FOR THE PURPOSE OF ENGAGING IN ANY INVESTMENT ACTIVITY MAY EXPOSE YOU TO A SIGNIFICANT RISK OF LOSS. By receiving this document, you will not be deemed a client or provided with the protections afforded to clients of CSLS. When distributing this document, CSLS or any member of the First City Group is not acting for any recipient of this document and will not be responsible for providing advice to any recipient in relation to this document. Accordingly, CSLS will not be responsible to any recipient for providing the protections afforded to its clients. If you are in the UK, the protections of the Financial Services and Markets Act 2000 (FSMA) or Financial Conduct Authority (FCA) do not apply to any investment activity engaged in as a result of this communication; and any resulting transaction would not fall within the jurisdiction of any FSMA or FCA dispute resolution or compensation scheme. By accepting this document you confirm that you are so aware of the above stated. If you do not accept the above stated and/or if the distribution of this document is otherwise unlawful where you are, you are required to return the document immediately to CSLS. This document is not an offer to buy or sell or to solicit an offer to buy or sell any security. This document does not provide individually tailored investment advice. It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. The appropriateness of a particular investment will depend on an investor’s individual circumstances and objectives. The investments and shares referred to in this document may not be suitable for all investors. CSLS is a member of the FCMB Group Plc (“the Group”), a group of companies which includes First City Monument Bank Ltd., FCMB Capital Markets Ltd, First City Asset Management and FCMB UK. Either CSLS or any other member of the Group may effect transactions in shares mentioned herein, may take proprietary trading positions in those shares, and may receive remuneration for the publication of its research and for other services. Accordingly, this document may not be considered as objective or impartial. Additionally, information may be available to CSLS or the Group, which is not reflected in this material. Further information on CSLS’ policy regarding potential conflicts of interest in the context of investment research and CSLS’ policy on disclosure and conflicts in general are available on request. This document is based on information obtained from sources it believes are reliable but which it has not independently verified. Neither CSLS nor its advisors, directors or employees make any guarantee, representation or warranty as to its accuracy, reasonableness or completeness and neither CSLS nor its advisors, directors or employees accepts any responsibility or liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this document. The opinions contained in this document are subject to change without notice and not to be relied upon and should not be used in substitution for the exercise of independent judgment. Past performance is not a guarantee of future performance. Investments may go down in value as well as up and you may not get back the full amount invested. Where an investment is denominated in a currency other than the local currency of the recipient of the research report, changes in the exchange rates may have an adverse effect on the value, price or income of that investment. In case of investments for which there is no recognized market it may be difficult for investors to sell their investments or to obtain reliable information about its value or the extent of the risk to which it is exposed. The information contained in this document is confidential and is solely for use of those persons to whom it is addressed and may not be reproduced, further distributed to any other person or published, in whole or in part, for any purpose. © CSLS 2013. All rights reserved CSL STOCKBROKERS LIMITED Member of the Nigerian Stock Exchange First City Plaza, 44 Marina, PO Box 9117, Lagos State, NIGERIA