Retail views on Nigeria's Q4 results and market review

1. Retail views

UBA Q4 results

Nigeria Thursday, 19 February 2015

Daily Retail Report

.

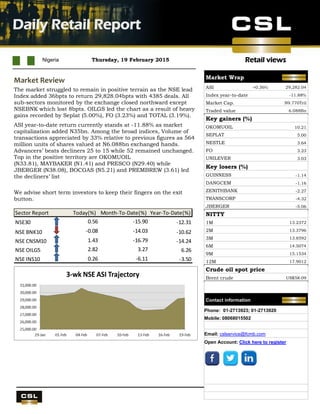

Market Review

The market struggled to remain in positive terrain as the NSE lead

Index added 36bpts to return 29,828.04bpts with 4385 deals. All

sub-sectors monitored by the exchange closed northward except

NSEBNK which lost 8bpts. OILGS led the chart as a result of heavy

gains recorded by Seplat (5.00%), FO (3.23%) and TOTAL (3.19%).

ASI year-to-date return currently stands at -11.88% as market

capitalization added N35bn. Among the broad indices, Volume of

transactions appreciated by 33% relative to previous figures as 564

million units of shares valued at N6.088bn exchanged hands.

Advancers’ beats decliners 25 to 15 while 52 remained unchanged.

Top in the positive territory are OKOMUOIL

(N33.81), MAYBAKER (N1.41) and PRESCO (N29.40) while

JBERGER (N38.08), BOCGAS (N5.21) and PREMBREW (3.61) led

the decliners’ list

We advise short term investors to keep their fingers on the exit

button.

Sector Report Today(%) Month-To-Date(%) Year-To-Date(%)

NSE30 0.56 -15.90 -12.31

NSE BNK10 -0.08 -14.03 -10.62

NSE CNSM10 1.43 -16.79 -14.24

NSE OILG5 2.82 3.27 6.26

NSE INS10 0.26 -6.11 -3.50

Market Wrap

ASI +0.36% 29,282.04

Index year-to-date -11.88%

Market Cap. N9.770Tril

Traded value 6.088Bn

Key gainers (%)

OKOMUOIL 10.21

SEPLAT 5.00

NESTLE 3.64

FO 3.23

UNILEVER 3.03

Key losers (%)

GUINNESS -1.14

DANGCEM -1.16

ZENITHBANK -2.27

TRANSCORP -4.32

JBERGER -5.06

NITTY

1M 13.2372

2M 13.3796

3M 13.8592

6M 14.5074

9M 15.1534

12M 17.9012

Crude oil spot price

Brent crude US$58.09

Contact information

Phone: 01-2713923; 01-2713920

Mobile: 08068015502

Email: cslservice@fcmb.com

Open Account: Click here to register

2. Daily Retail Report

Page 2

Retail views

0

Stock Recommendations

Banking Comment

Current

Price

Target

Price

Potential

Upside %

EPS

FY

2013

1 Yr

forward

EPS

Last

Dividend

(N)

P/BV

2013

Yield FY

2013

Yield FY

2014e

Shares

Outstanding

(millions)

Year

End

ACCESS BANK Buy 5.60 7.73 38% 1.60 1.90 0.35 0.80 7.10% 11.5% 22883.00 Dec.

DIAMOND BANK Buy 3.71 5.27 42% 2.00 1.70 0.30 0.60 5.40% 5.4% 14475.00 Dec.

FIDELITY BANK PLC Buy 1.20 1.86 55% 0.30 0.50 0.14 0.30 7.40% 11.6% 28974.00 Dec.

FBN HOLDINGS Buy 7.09 12.86 81% 2.20 2.30 1.10 0.80 10.00% 10.0% 32632.00 Dec.

GUARANTY TRUST BANK Buy 21.00 28.42 35% 3.20 3.30 1.45 2.20 6.90% 7.3% 29431.00 Dec.

STANBIC HOLDINGS Hold 24.40 32.37 33% 1.90 2.60 1.20 3.10 2.70% 3.5% 10000.00 Dec.

STERLING BANK Hold 2.25 1.57 -30% 0.40 0.40 0.25 0.80 10.90% 8.7% 21592.00 Dec.

SKYE BANK Under review 2.00 -100% 1.20 1.10 0.30 0.30 11.10% 20.7% 13219.00 Dec.

U B A Buy 3.15 5.70 81% 1.40 1.50 0.50 0.70 10.10% 10.1% 32981.00 Dec.

ZENITH BANK Buy 17.20 24.60 43% 3.00 3.00 1.75 1.30 8.10% 8.3% 31396.00 Dec.

Food & Beverage

EV/EBITDA (x)

2013

Yield FY

2013e

DANGOTE SUGAR REFINERY Under review 6.20 Under review N/A 0.89 1.20 0.60 4.70 7.40% 7.4% 12000.00 Dec.

CADBURY NIG. Under review 42.98 Under review N/A 2.90 3.20 1.30 7.60 0.00% 4.7% 1878.00 Dec.

FLOUR MILLS Hold 30.00 54.80 83% 2.90 3.50 1.60 8.90 3.30% 4.0% 2385.00 Mar.

HONEYWELL FLOURMILLS Buy 2.96 5.20 76% 0.40 0.30 0.17 12.00 5.70% 4.7% 7930.00 Mar.

NESTLE FOODS NIG. Hold 819.99 821.80 0% 28.10 31.30 24.00 24.90 2.60% 3.0% 792.00 Dec.

P Z INDUSTRIES Hold 27.30 34.60 27% 1.20 1.30 0.19 7.80 2.70% 3.0% 3970.00 May

U A C N Buy 33.99 72.60 114% 2.90 3.60 1.75 5.40 4.00% 4.7% 1920.00 Dec.

UNILEVER NIGERIA PLC Sell 34.00 31.80 -6% 1.30 1.60 1.25 13.70 3.80% 3.8% 3783.00 Dec.

Building Materials EPS 2013e

EV/EBITDA(x)

2013e

Yield FY

2013e

LAFARGE WAPCO PLC Under review 84.00 Under review N/A 9.40 9.40 3.30 8.20 3.30% 3.3% 3001.00 Mar.

DANGOTE CEMENT Buy 153.20 258.50 N/A 11.80 11.90 7.00 16.10 3.40% 3.5% 17040.00 Dec.

Breweries EPS 2013e

EV/EBITDA(x)

2013e

Yield FY

2013e

GUINNESS NIG. Sell 123.28 111.00 -10% 7.90 5.90 7.00 14.50 4.30% 3.0% 1506.00 June

INTERNATIONAL BREWERIES Hold 18.00 24.50 36% 0.90 1.30 0.30 16.20 1.00% 1.5% 3263.00 Mar.

NIGERIAN BREWERIES Sell 133.85 121.20 -9% 5.70 5.60 4.50 13.30 2.90% 2.1% 7562.00 June

Agriculture EPS 2013e

EV/EBITDA (x)

2013e

Yield FY

2013e

OKOMU OIL Buy 33.89 41.50 22% 2.20 3.00 1.00 9.00 3.20% 6.7% 953.00 Dec.

PRESCO PLC Buy 29.40 42.70 45% 1.29 1.60 0.10 9.20 0.40% 1.7% 1000.00 Dec.

Pharmaceuticals EV/EBITDA (x)

2013

Yield FY 2013

GLAXOSMITHKLINE BEECHAM NIG. Buy 42.00 78.60 0.87 3.10 4.30 1.30 8.90 2.50% 3.8% 957.00 Dec.

Note – for full report on the recommended stocks kindly send an email to cslcsu@firstcitygroup.com

3. Daily Retail Report

Page 3

Retail views

Top Highlight

Unofficial: Naira currency devaluation- The CBN devalues the naira to circa N198.0/US$1.0; and equities rally

7.1%

It has finally happened, but through an unofficial route. For the past four trading days the Central Bank of Nigeria (CBN) has been taking client

bids for US dollars via banks, and then offering banks US dollars at close to the inter-bank rate, rather than its own official rate.

We understand that late last week it was offering US dollars at N198.0/US$1.0 and at N198.5/US$1.0, then on Monday and Tuesday this week at

N198.0/US$1.0, yesterday at N197.0/US$1.0. This is a far cry from its official N168.0/US$1.0 rate arrived at last November and unchanged since

then for deals in its Retail Dutch Auction System (RDAS). Yesterday it announced that the RDAS is closed for business.

Our base case was that the CBN would ease its official RDAS rate from N168.0/US$1.0 to N182.0/US$1.0, or even out to N191.0/US$1.00 (which

would have made N200.0/US$1.0 a credible interbank exchange rate within a 5.0% band). In the event it has gone further than this by closing

RDAS and entering the interbank market itself.

But it has not made an announcement about devaluation, no doubt due to political sensitivities in the run-up to general elections on 28 March

and 11 April.

Can the currency slip further? Our base case is that it will find a back-stop in the interbank market – which is now the same as with the CBN’s

own rate – of N220.0/US$1.0. But the naira still needs support from a) a reduction in imports (this happens through lower fuel import costs, for

example), b) fewer losses through the ‘net errors and omissions line’ in national accounts (which will likely fall with reduced oil prices), and c)

portfolio investment and foreign direct investment. There is some evidence of c) as the equity market has rallied 7.1% this week.

Today’s news headlines

Imports decline sharply as ship traffic drops 63%: The volume of goods imported into Nigeria is witnessing a sharp decline,

causing a drop in cargo ship traffic in the nation’s sea ports, as the devaluation of the local currency begins to exert pressure on the

sector. Source: businessdayonline.com

CBN sells dollar to banks at N198: In a bid to reduce pressure on the naira, which has come under speculative attacks in recent

weeks, the Central Bank of Nigeria on Wednesday announced the closure of the Retail and Wholesale Dutch Auction Systems of the

foreign exchange market. The closure, which takes immediate effect, was confirmed in a statement issued by the Director, Corporate

Communications Department, CBN, Mr. Ibrahim Mu’azu. In taking the step, the central bank was said to have fixed the exchange

rate of the naira to the dollar at 198, which is N30 above its N168 (+/-5 per cent) rate. Source: punchng.com

FG considers more budget cuts ahead of elections: The Federal Government will consider further cuts to the 2015 budget and

adjust its US$65 benchmark oil price downwards, according to Ngozi Okonjo-Iweala, finance minister, who has lowered her gross

domestic product forecast for Africa’s largest economy from 5.5% to 4.5-4.8% this year. Source: businessdayonline.com