BEST Call Girls In Old Faridabad ✨ 9773824855 ✨ Escorts Service In Delhi Ncr,

Daily Market performance

1. Retail views

UBA Q4 results

Nigeria Wednesday, 7 January 2015

Daily Retail Report

.

Market Review

NSE sustained the negative momentum that has prevailed the

equity market all week. A bloodbath was witnessed amongst

Banking counters, not surprisingly though – the FG had as at

yesterday, reiterated its directive to MDAs to close all revenue

accounts with Deposit Money Banks, worsening investors’

sentiments that have been on pessimistic note since the start of the

year. Relentless selling activities was witnessed across sectoral

board as BNK was down by 7.47%,CNSM down by 3.01% and IND

down by 2.58%.

Overall market breadth was in the favour of decliners which

thumped advancers in the ratio of 52:8; while 36 remained

unchanged. Among the broad indices, NSE All Share Index

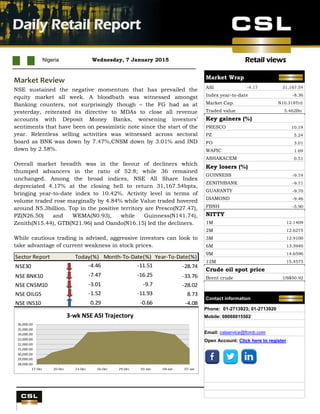

depreciated 4.17% at the closing bell to return 31,167.54bpts,

bringing year-to-date index to 10.42%. Activity level in terms of

volume traded rose marginally by 4.84% while Value traded hovered

around N5.3billion. Top in the positive territory are Presco(N27.47),

PZ(N26.50) and WEMA(N0.93), while Guinness(N141.74),

Zenith(N15.44), GTB(N21.96) and Oando(N16.15) led the decliners.

While cautious trading is advised, aggressive investors can look to

take advantage of current weakness in stock prices.

Sector Report Today(%) Month-To-Date(%) Year-To-Date(%)

NSE30 -4.46 -11.51 -28.74

NSE BNK10 -7.47 -16.25 -33.76

NSE CNSM10 -3.01 -9.7 -28.02

NSE OILG5 -1.52 -11.93 8.73

NSE INS10 0.29 -0.66 -4.08

Market Wrap

ASI -4.17 31,167.54

Index year-to-datee -8.36

Market Cap. N10.318Tril

Traded value 5.462Bn

Key gainers (%)

PRESCO 10.19

PZ 5.24

FO 3.01

WAPIC 1.69

ASHAKACEM 0.51

Key losers (%)

GUINNESS -9.74

ZENITHBANK -9.71

GUARANTY -9.70

DIAMOND -9.46

FBNH -5.90

NITTY

1M 12.1409

2M 12.6275

3M 12.9100

6M 13.3940

9M 14.6596

12M 15.4575

Crude oil spot price

Brent crude US$50.92

Contact information

Phone: 01-2713923; 01-2713920

Mobile: 08068015502

Email: cslservice@fcmb.com

Open Account: Click here to register

2. Daily Retail Report

Page 2

Retail views

Stock Recommendations

Banking Comment

Current

Price

Target

Price

Potential

Upside %

EPS

FY

2013

1 Yr

forward

EPS

Last

Dividend

(N)

P/BV

2013

Yield FY

2013

Yield FY

2014e

Shares

Outstanding

(millions)

Year

End

ACCESS BANK Hold 5.74 11.00 92% 1.60 1.90 0.35 0.80 7.10% 11.5% 22883.00 Dec.

DIAMOND BANK Buy 4.69 8.10 73% 2.00 1.70 0.30 0.60 5.40% 5.4% 14475.00 Dec.

FIDELITY BANK PLC Buy 1.60 3.00 88% 0.30 0.50 0.14 0.30 7.40% 11.6% 28974.00 Dec.

FBN HOLDINGS Hold 7.81 14.70 88% 2.20 2.30 1.10 0.80 10.00% 10.0% 32632.00 Dec.

GUARANTY TRUST BANK Buy 21.96 39.80 81% 3.20 3.30 1.45 2.20 6.90% 7.3% 29431.00 Dec.

STANBIC HOLDINGS Hold 27.99 15.50 -45% 1.90 2.60 1.20 3.10 2.70% 3.5% 10000.00 Dec.

STERLING BANK Hold 2.49 2.70 8% 0.40 0.40 0.25 0.80 10.90% 8.7% 21592.00 Dec.

SKYE BANK Hold 2.30 5.00 117% 1.20 1.10 0.30 0.30 11.10% 20.7% 13219.00 Dec.

U B A Hold 3.79 7.40 95% 1.40 1.50 0.50 0.70 10.10% 10.1% 32981.00 Dec.

ZENITH BANK Buy 15.44 31.50 104% 3.00 3.00 1.75 1.30 8.10% 8.3% 31396.00 Dec.

Food & Beverage

EV/EBITDA (x)

2013

Yield FY

2013e

DANGOTE SUGAR REFINERY Under review 5.53 Under review N/A 0.89 1.20 0.60 4.70 7.40% 7.4% 12000.00 Dec.

CADBURY NIG. Under review 42.00 Under review N/A 2.90 3.20 1.30 7.60 0.00% 4.7% 1878.00 Dec.

FLOUR MILLS Hold 35.38 54.80 55% 2.90 3.50 1.60 8.90 3.30% 4.0% 2385.00 Mar.

HONEYWELL FLOURMILLS Buy 3.46 5.20 50% 0.40 0.30 0.17 12.00 5.70% 4.7% 7930.00 Mar.

NESTLE FOODS NIG. Hold 945.82 821.80 -13% 28.10 31.30 24.00 24.90 2.60% 3.0% 792.00 Dec.

P Z INDUSTRIES Hold 26.50 34.60 31% 1.20 1.30 0.19 7.80 2.70% 3.0% 3970.00 May

U A C N Buy 30.60 72.60 137% 2.90 3.60 1.75 5.40 4.00% 4.7% 1920.00 Dec.

UNILEVER NIGERIA PLC Sell 33.80 31.80 -6% 1.30 1.60 1.25 13.70 3.80% 3.8% 3783.00 Dec.

Building Materials EPS 2013e

EV/EBITDA(x)

2013e

Yield FY

2013e

LAFARGE WAPCO PLC Under review 80.02 Under review N/A 9.40 9.40 3.30 8.20 3.30% 3.3% 3001.00 Mar.

DANGOTE CEMENT Buy 171.48 258.50 N/A 11.80 11.90 7.00 16.10 3.40% 3.5% 17040.00 Dec.

Breweries EPS 2013e

EV/EBITDA(x)

2013e

Yield FY

2013e

GUINNESS NIG. Sell 141.74 111.00 -22% 7.90 5.90 7.00 14.50 4.30% 3.0% 1506.00 June

INTERNATIONAL BREWERIES Hold 21.00 24.50 17% 0.90 1.30 0.30 16.20 1.00% 1.5% 3263.00 Mar.

NIGERIAN BREWERIES Sell 139.82 121.20 -13% 5.70 5.60 4.50 13.30 2.90% 2.1% 7562.00 June

Agriculture EPS 2013e

EV/EBITDA (x)

2013e

Yield FY

2013e

OKOMU OIL Buy 25.46 41.50 63% 2.20 3.00 1.00 9.00 3.20% 6.7% 953.00 Dec.

PRESCO PLC Buy 27.47 42.70 55% 1.29 1.60 0.10 9.20 0.40% 1.7% 1000.00 Dec.

Pharmaceuticals EV/EBITDA (x)

2013

Yield FY 2013

GLAXOSMITHKLINE BEECHAM NIG. Buy 42.79 78.60 0.84 3.10 4.30 1.30 8.90 2.50% 3.8% 957.00 Dec.

Note – for full report on the recommended stocks kindly send an email to cslcsu@firstcitygroup.com

3. Daily Retail Report

Page 3

Retail views

Top Highlight

UBA’s right issue opens

UBA’s (Hold, target price N7.40) rights issue opened on Monday, 29 December 2014. The bank is offering 3,298,138,756 ordinary shares

(compared with 32.9bn shares outstanding) on the basis of 1 new ordinary share for every 10 ordinary shares at N4.0/s, notably higher than

yesterday’s closing price of N3.98/s.

The rights if successful, could raise as much as N13.2bn (US$67.7m). According to management, proceeds of the offer will be used to expand the

bank’s e-banking channels, upgrade its technology platform, refurbish the bank’s business offices, and grow risk assets.

We have believed for some time that UBA was among three major Nigerian banks running short of capital (see CSL Nigeria’s Largest Banks – The

Capital Cycle, 1 Aug 2014) and we are of the view that the immediate effect of the rights issue will be to raise the bank’s capital adequacy ratio

(CAR) to meet regulatory requirements post Basel II implementation.

Capital requirements have become stringent. Apart from the fact that banks are expected to take a charge under Basel II/III for operational risk,

the Central Bank of Nigeria (CBN) had in August 2014 mandated that collective impairment and non-distributable regulatory reserves, and other

reserves, be excluded from tier-2 capital. The CBN also stipulated that exposure to the oil and gas sector in excess of 20% will attract a higher risk

weighting.

In addition, with effect from March 2015, systemically important banks (SIBs) in Nigeria (which includes UBA) would be required to set aside

Higher Loss Absorbency (HLA) or additional capital surcharge of 1% to their respective minimum required CARs which are expected to be met with

tier-1 common equity

News Headlines

Power: Residential consumers to pay more from July: The increase in electricity tariffs will become effective for all categories of consumers in July

this year. This means that residential consumers, who constitute about 80 per cent of power users in the country, will from that date pay the new

rates. According to the Nigerian Electricity Regulatory Commission, the bulk of the power consumers would have started paying higher tariffs from

the first day of this year if not for the freezing of the increased rates for residential users for a six-month period. Source: punchng.com

Close revenue accounts with banks, FG orders MDAs: The Federal Government on Tuesday directed all its Ministries, Departments and

Agencies to close their revenue accounts with Deposit Money Banks latest by February 28. The balances in the revenue accounts, it said, should

be transferred to the Consolidated Revenue Fund of the Federal Government. Source: punchng.com

Declining Revenue: Banks to Slow down State Governments' Borrowing: The dwindling revenue to the federation account owing to the declining

crude oil prices may hinder state governments from securing loans from Nigerian banks and other multilateral institutions as banks have already

resolved to stop lending to them to forestall a debt crisis. The Coordinating Minister for the Economy and Minister of Finance, Ngozi Okonjo-Iweala,

had called for enhanced monitoring of borrowing by state governments as a response to the decline of over N100 billion in monthly gross revenues

flowing into the federation account since July last year. Source:thisdaylive.com

Saudi set to price out Nigeria, Angola on crude: Nigeria and her African counterpart, Angola, are having their problems arising from the

dwindling prices of crude oil further compounded, as Saudi Arabia made deep cuts to its monthly oil prices for European buyers, while it trimmed

prices for U.S. refiners and increased rates for Asia. Almost half of Nigeria’s cargoes due to be exported in January are still available. The backlog

has pushed Nigerian oil differentials versus Brent to their lowest since at least 2009 BFO-QUA at 65 cents a barrel, down 80 percent since May,

said Reuters. And it is also creating a discount frenzy between African and Gulf oil producers to Asian buyers. Source: businessdayonline.com