UBA Q4 Results Daily Retail Report Nigeria

•

0 likes•215 views

Daily retail report 050315

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (20)

Similar to UBA Q4 Results Daily Retail Report Nigeria

Similar to UBA Q4 Results Daily Retail Report Nigeria (20)

Recently uploaded

Recently uploaded (20)

UBA Q4 Results Daily Retail Report Nigeria

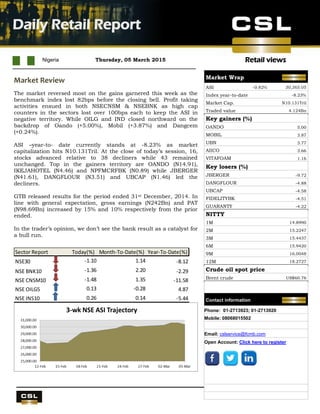

- 1. Retail views UBA Q4 results Nigeria Thursday, 05 March 2015 Daily Retail Report . Market Review The market reversed most on the gains garnered this week as the benchmark index lost 82bps before the closing bell. Profit taking activities ensued in both NSECNSM & NSEBNK as high cap counters in the sectors lost over 100bps each to keep the ASI in negative territory. While OILG and IND closed northward on the backdrop of Oando (+5.00%), Mobil (+3.87%) and Dangcem (+0.24%). ASI –year-to- date currently stands at -8.23% as market capitalization hits N10.131Tril. At the close of today’s session, 16, stocks advanced relative to 38 decliners while 43 remained unchanged. Top in the gainers territory are OANDO (N14.91), IKEJAHOTEL (N4.46) and NPFMCRFBK (N0.89) while JBERGER (N41.61), DANGFLOUR (N3.51) and UBCAP (N1.46) led the decliners. GTB released results for the period ended 31st December, 2014. In line with general expectation, gross earnings (N242Bn) and PAT (N98.69Bn) increased by 15% and 10% respectively from the prior ended. In the trader’s opinion, we don’t see the bank result as a catalyst for a bull run. Sector Report Today(%) Month-To-Date(%) Year-To-Date(%) NSE30 -1.10 1.14 -8.12 NSE BNK10 -1.36 2.20 -2.29 NSE CNSM10 -1.48 1.35 -11.58 NSE OILG5 0.13 -0.28 4.87 NSE INS10 0.26 0.14 -5.44 Market Wrap ASI -0.82% 30,365.05 Index year-to-date -8.23% Market Cap. N10.131Tril Traded value 4.124Bn Key gainers (%) OANDO 5.00 MOBIL 3.87 UBN 3.77 AIICO 3.66 VITAFOAM 1.16 Key losers (%) JBERGER -9.72 DANGFLOUR -4.88 UBCAP -4.58 FIDELITYBK -4.51 GUARANTY -4.22 NITTY 1M 14.8990 2M 15.2247 3M 15.4437 6M 15.9420 9M 16.0048 12M 18.2727 Crude oil spot price Brent crude US$60.76 Contact information Phone: 01-2713923; 01-2713920 Mobile: 08068015502 Email: cslservice@fcmb.com Open Account: Click here to register

- 2. Daily Retail Report Page 2 Retail views Stock Recommendations Banking Comment Current Price Target Price Potential Upside % EPS FY 2013 1 Yr forward EPS Last Dividend (N) P/BV 2013 Yield FY 2013 Yield FY 2014e Shares Outstanding (millions) Year End ACCESS BANK Buy 6.45 7.73 20% 1.60 1.90 0.35 0.80 7.10% 11.5% 22883.00 Dec. DIAMOND BANK Buy 4.10 5.27 29% 2.00 1.70 0.30 0.60 5.40% 5.4% 14475.00 Dec. FIDELITY BANK PLC Buy 1.27 1.86 46% 0.30 0.50 0.14 0.30 7.40% 11.6% 28974.00 Dec. FBN HOLDINGS Buy 8.00 12.86 61% 2.20 2.30 1.10 0.80 10.00% 10.0% 32632.00 Dec. GUARANTY TRUST BANK Buy 22.03 28.42 29% 3.20 3.30 1.45 2.20 6.90% 7.3% 29431.00 Dec. STANBIC HOLDINGS Hold 26.00 32.37 25% 1.90 2.60 1.20 3.10 2.70% 3.5% 10000.00 Dec. STERLING BANK Hold 2.28 1.57 -31% 0.40 0.40 0.25 0.80 10.90% 8.7% 21592.00 Dec. SKYE BANK Under review 2.07 -100% 1.20 1.10 0.30 0.30 11.10% 20.7% 13219.00 Dec. U B A Buy 3.70 5.70 54% 1.40 1.50 0.50 0.70 10.10% 10.1% 32981.00 Dec. ZENITH BANK Buy 19.00 24.60 29% 3.00 3.00 1.75 1.30 8.10% 8.3% 31396.00 Dec. Food & Beverage EV/EBITDA (x) 2013 Yield FY 2013e DANGOTE SUGAR REFINERY Under review 6.39 Under review N/A 0.89 1.20 0.60 4.70 7.40% 7.4% 12000.00 Dec. CADBURY NIG. Under review 37.90 Under review N/A 2.90 3.20 1.30 7.60 0.00% 4.7% 1878.00 Dec. FLOUR MILLS Hold 34.92 54.80 57% 2.90 3.50 1.60 8.90 3.30% 4.0% 2385.00 Mar. HONEYWELL FLOURMILLS Buy 2.90 5.20 79% 0.40 0.30 0.17 12.00 5.70% 4.7% 7930.00 Mar. NESTLE FOODS NIG. Hold 820.00 821.80 0% 28.10 31.30 24.00 24.90 2.60% 3.0% 792.00 Dec. P Z INDUSTRIES Hold 27.99 34.60 24% 1.20 1.30 0.19 7.80 2.70% 3.0% 3970.00 May U A C N Buy 35.10 72.60 107% 2.90 3.60 1.75 5.40 4.00% 4.7% 1920.00 Dec. UNILEVER NIGERIA PLC Sell 34.86 31.80 -9% 1.30 1.60 1.25 13.70 3.80% 3.8% 3783.00 Dec. Building Materials EPS 2013e EV/EBITDA(x) 2013e Yield FY 2013e LAFARGE WAPCO PLC Under review 87.99 Under review N/A 9.40 9.40 3.30 8.20 3.30% 3.3% 3001.00 Mar. DANGOTE CEMENT Buy 152.90 258.50 N/A 11.80 11.90 7.00 16.10 3.40% 3.5% 17040.00 Dec. Breweries EPS 2013e EV/EBITDA(x) 2013e Yield FY 2013e GUINNESS NIG. Sell 127.00 111.00 -13% 7.90 5.90 7.00 14.50 4.30% 3.0% 1506.00 June INTERNATIONAL BREWERIES Hold 19.47 24.50 26% 0.90 1.30 0.30 16.20 1.00% 1.5% 3263.00 Mar. NIGERIAN BREWERIES Sell 145.00 121.20 -16% 5.70 5.60 4.50 13.30 2.90% 2.1% 7562.00 June Agriculture EPS 2013e EV/EBITDA (x) 2013e Yield FY 2013e OKOMU OIL Buy 30.70 41.50 35% 2.20 3.00 1.00 9.00 3.20% 6.7% 953.00 Dec. PRESCO PLC Buy 32.38 42.70 32% 1.29 1.60 0.10 9.20 0.40% 1.7% 1000.00 Dec. Pharmaceuticals EV/EBITDA (x) 2013 Yield FY 2013 GLAXOSMITHKLINE BEECHAM NIG. Buy 40.00 78.60 0.97 3.10 4.30 1.30 8.90 2.50% 3.8% 957.00 Dec. Note – for full report on the recommended stocks kindly send an email to cslcsu@firstcitygroup.com

- 3. Daily Retail Report Page 3 Retail views Top Highlight MTN- MTN continues to look to Nigeria for growth Yesterday, MTN Group (MTN, N/R), Africa’s largest wireless operator and the parent company of MTN Nigeria (not listed) released its full year results for 2014. MTN’s Revenues increased by 4.6% y/y in FY 2014, driven mainly by a 12.1% y/y growth in MTN Nigeria’s Revenues. MTN achieved growth despite contraction in some key markets such as South Africa (its home market), where it recorded a 3.9% y/y decline in Sales. MTN ascribes the growth in its Nigerian subsidiary to improved offerings to customers and increased promotions in the year. MTN Nigeria’s subscriber base grew by 5.5% y/y in 2014 to 59.9 million. Nigeria is MTN’s largest market both by Revenues and subscriber base. Nigeria contributed 36.7% to overall Revenues and 43.2% to EBITDA in 2014. South Africa contributed 26.5% to Revenues and 17.1% to EBITDA in 2014. Out of four existing mobile operators in Nigeria, MTN Nigeria is the leader with c.44% market share as of December 2014. MTN entered into the Nigerian market in 2001 following the liberalisation of the telecommunications sector. As competition within the mobile operations market heightens, especially in the areas of voice calls and short message services, MTN Nigeria has increasingly turned to opportunities in data sales, e-commerce, and mobile money banking to defend its market share. Today’s news headlines Access Bank extends N52.6bn rights issue by two weeks: Access Bank Plc has extended its Rights Issue by two weeks to March 18, following an approval the bank received from the Securities and Exchange Commission (SEC). Access Bank Plc’s Rights Issue of 7.627 billion ordinary shares of 50 kobo each at N6.90 had opened on January 26, and was expected to close yesterday. However, the bank said the issue had been extended by two weeks. The extension, according to Access Bank, is due to the need to give shareholders, who are yet to take up their rights more time to do so considering the prevailing economic and political situation. Source: thisdaylive.com Oando receives N50bn payout, despite slump in oil price: As exploration and production (E &P) companies contend with the reality of lower oil prices translating to lower revenue and operating cash flows, the decline in prices has led to a substantial gain for Oando Energy Resources (OER), the Upstream subsidiary of Oando Plc. The company said in a statement last night that it realised a cash windfall in the sum of $234 million due to the proactive fiscal measures put in place prior to the slump in oil prices. Source: thisdaylive.com CBN creates N300bn (US$1.5bn) fund for real sector operators: The Central Bank of Nigeria says it has established a N300bn real sector support facility, in a bid to unlock the potential of the sector to engender output growth, value-added productivity and job creation. The CBN, in a circular on Wednesday, said the facility would be used to support large enterprises for startups and expansion financing needs of N500m up to a maximum of N10bn. The real sector activities targeted by the facility are manufacturing, agricultural value chain and selected service sub-sectors, the bank said. Source: punchng.com

- 4. Daily Retail Report Page 4 Retail views Important Risk Warnings and Disclaimers CSL STOCKBROKERS LIMITED (CSLS) is regulated and authorized by the Securities and Exchange Commission (SEC) of Nigeria and the Nigerian Stock Exchange (NSE). The details of the authorization can be viewed at the SEC Website at http://www.sec.gov.ng/consolidated-list-of-capital-market-operators.html and at the NSE Website at http://www.nse.com.ng/Regulation/ForBrokers/Pages/Dealing-Members.asp. RELIANCE ON THIS NOTE FOR THE PURPOSE OF ENGAGING IN ANY INVESTMENT ACTIVITY MAY EXPOSE YOU TO A SIGNIFICANT RISK OF LOSS. By receiving this document, you will not be deemed a client or provided with the protections afforded to clients of CSLS. When distributing this document, CSLS or any member of the First City Group is not acting for any recipient of this document and will not be responsible for providing advice to any recipient in relation to this document. Accordingly, CSLS will not be responsible to any recipient for providing the protections afforded to its clients. If you are in the UK, the protections of the Financial Services and Markets Act 2000 (FSMA) or Financial Conduct Authority (FCA) do not apply to any investment activity engaged in as a result of this communication; and any resulting transaction would not fall within the jurisdiction of any FSMA or FCA dispute resolution or compensation scheme. By accepting this document you confirm that you are so aware of the above stated. If you do not accept the above stated and/or if the distribution of this document is otherwise unlawful where you are, you are required to return the document immediately to CSLS. This document is not an offer to buy or sell or to solicit an offer to buy or sell any security. This document does not provide individually tailored investment advice. It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. The appropriateness of a particular investment will depend on an investor’s individual circumstances and objectives. The investments and shares referred to in this document may not be suitable for all investors. CSLS is a member of the FCMB Group Plc (“the Group”), a group of companies which includes First City Monument Bank Ltd., FCMB Capital Markets Ltd, First City Asset Management and FCMB UK. Either CSLS or any other member of the Group may effect transactions in shares mentioned herein, may take proprietary trading positions in those shares, and may receive remuneration for the publication of its research and for other services. Accordingly, this document may not be considered as objective or impartial. Additionally, information may be available to CSLS or the Group, which is not reflected in this material. Further information on CSLS’ policy regarding potential conflicts of interest in the context of investment research and CSLS’ policy on disclosure and conflicts in general are available on request. This document is based on information obtained from sources it believes are reliable but which it has not independently verified. Neither CSLS nor its advisors, directors or employees make any guarantee, representation or warranty as to its accuracy, reasonableness or completeness and neither CSLS nor its advisors, directors or employees accepts any responsibility or liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this document. The opinions contained in this document are subject to change without notice and not to be relied upon and should not be used in substitution for the exercise of independent judgment. Past performance is not a guarantee of future performance. Investments may go down in value as well as up and you may not get back the full amount invested. Where an investment is denominated in a currency other than the local currency of the recipient of the research report, changes in the exchange rates may have an adverse effect on the value, price or income of that investment. In case of investments for which there is no recognized market it may be difficult for investors to sell their investments or to obtain reliable information about its value or the extent of the risk to which it is exposed. The information contained in this document is confidential and is solely for use of those persons to whom it is addressed and may not be reproduced, further distributed to any other person or published, in whole or in part, for any purpose. © CSLS 2013. All rights reserved CSL STOCKBROKERS LIMITED

- 5. Daily Retail Report Page 5 Retail views Member of the Nigerian Stock Exchange First City Plaza, 44 Marina, PO Box 9117, Lagos State, NIGERIA