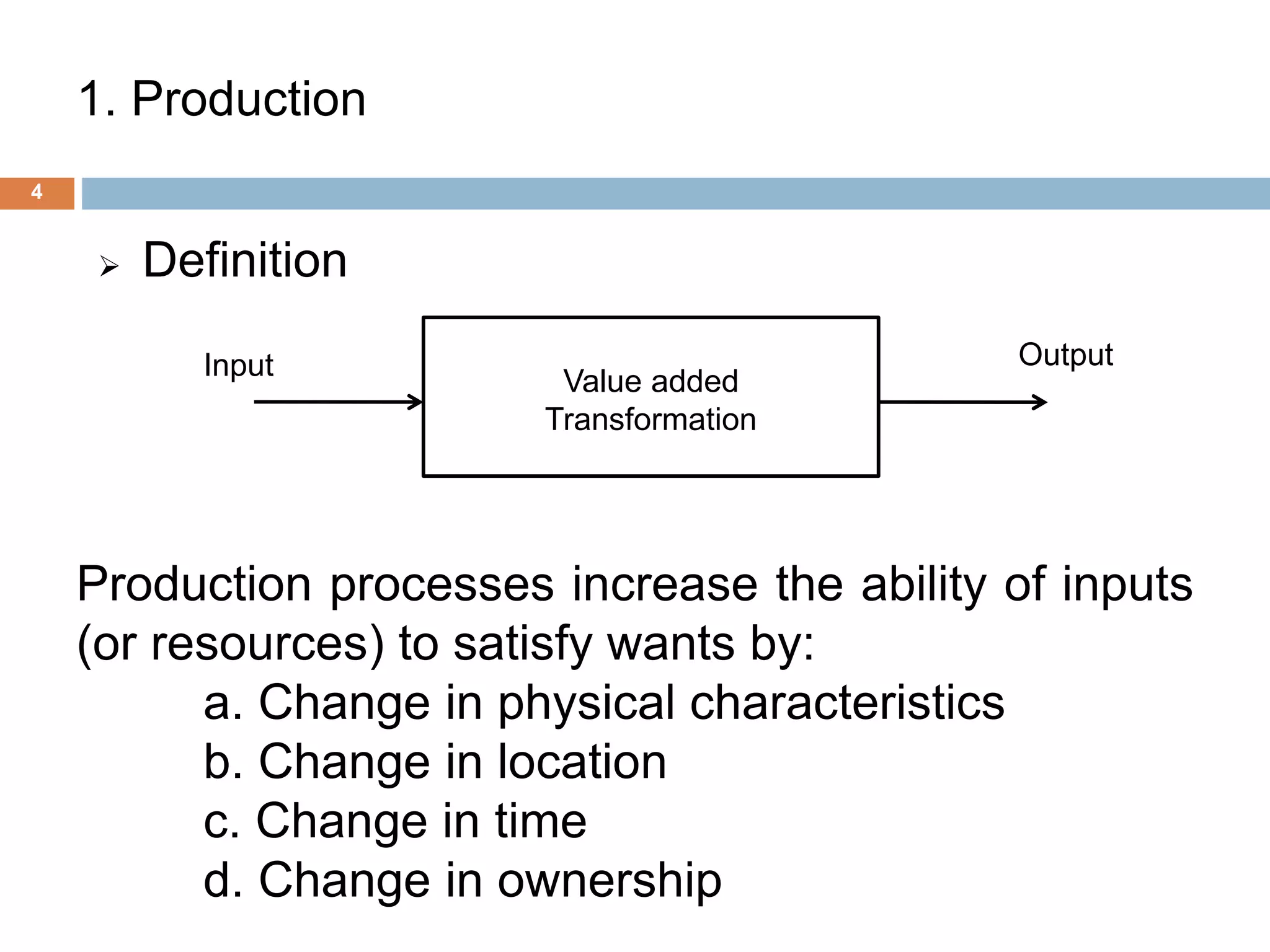

The document presents an overview of production and cost theory, outlining key concepts such as production efficiency, cost estimation, and maximizing organizational profit. It includes discussions on short-run and long-run production functions, cost components, and important economic terms like marginal cost and returns to scale. The conclusion emphasizes the significance of these theories for effective managerial decision-making and financial benefits.