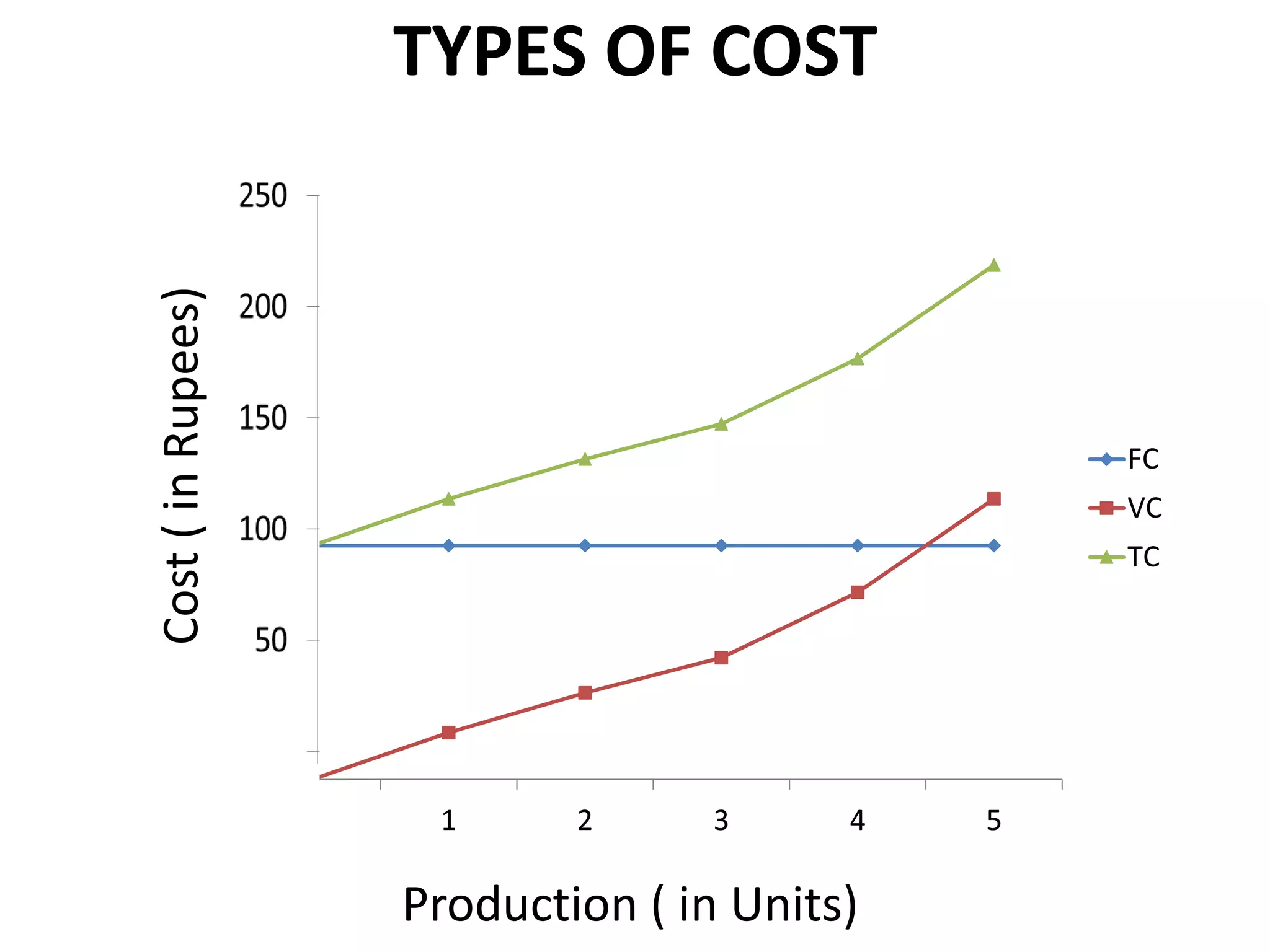

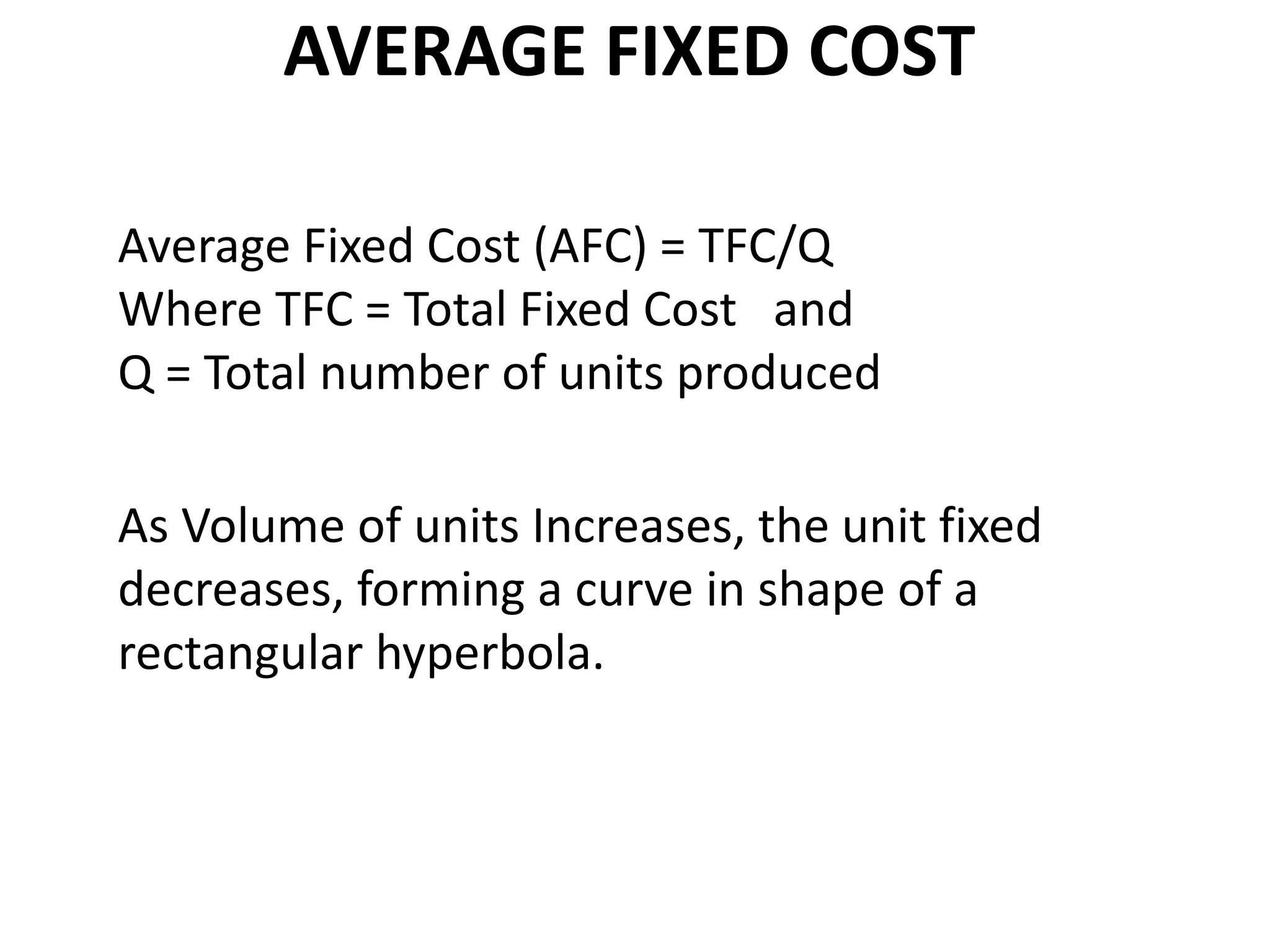

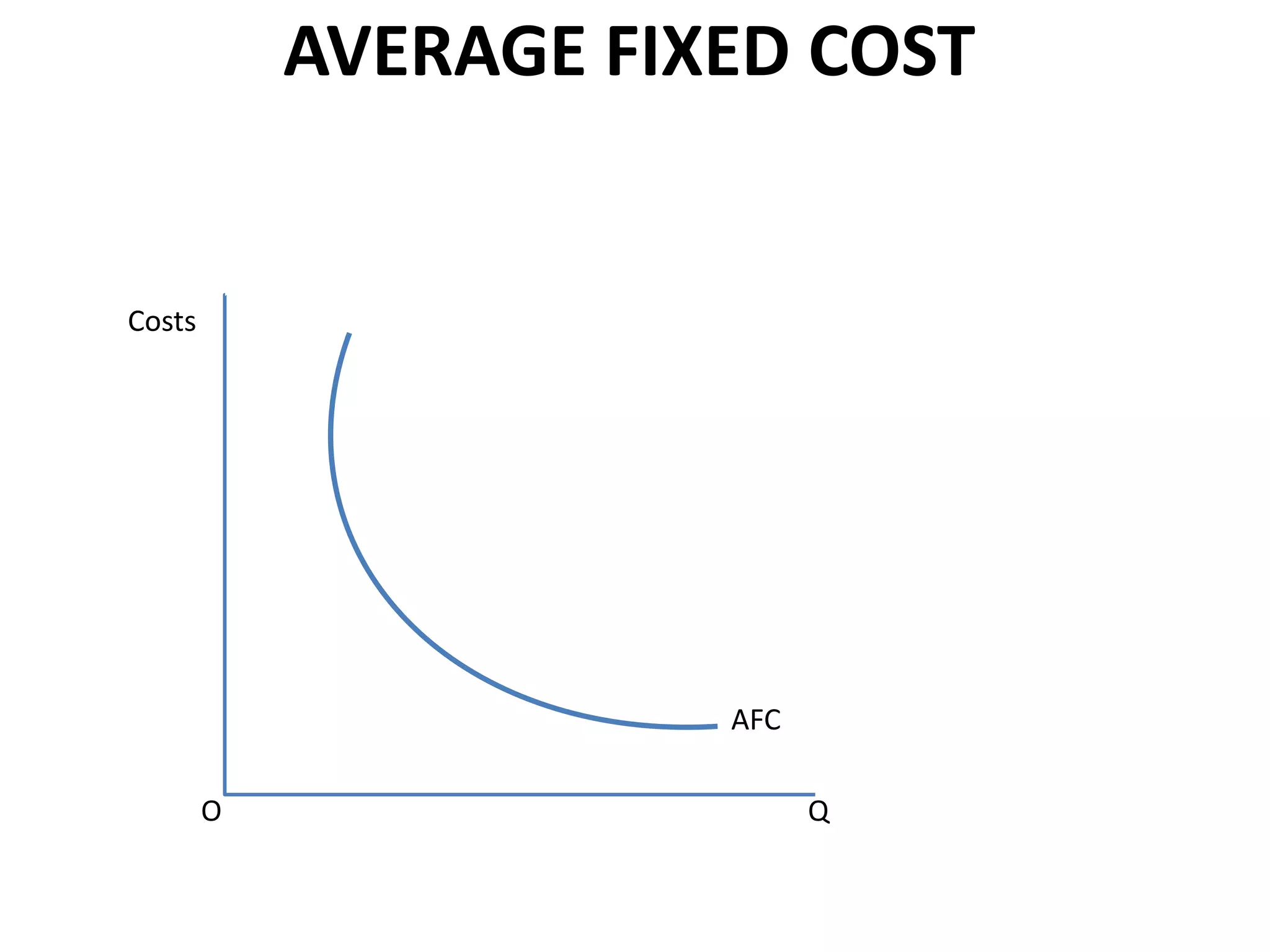

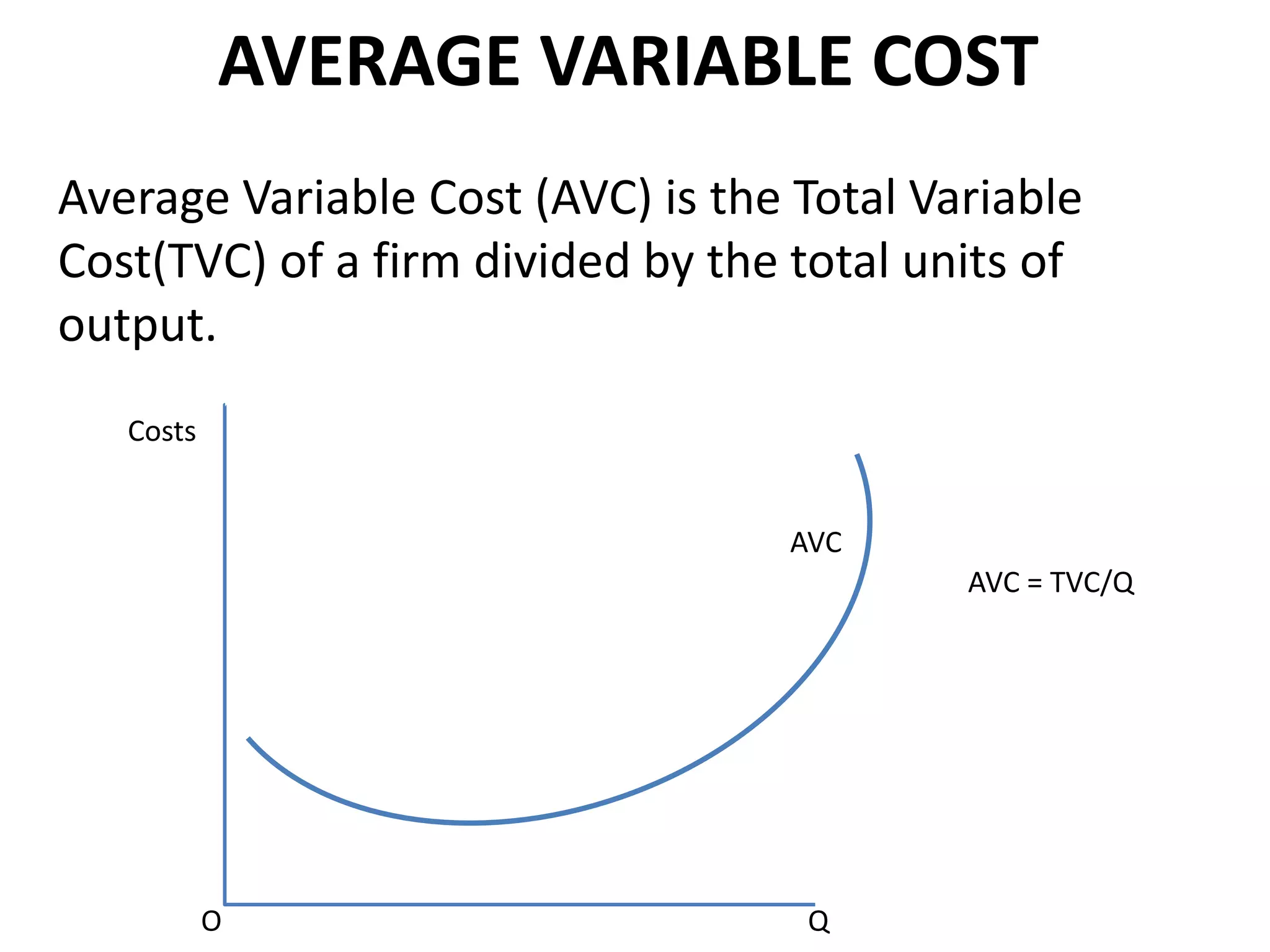

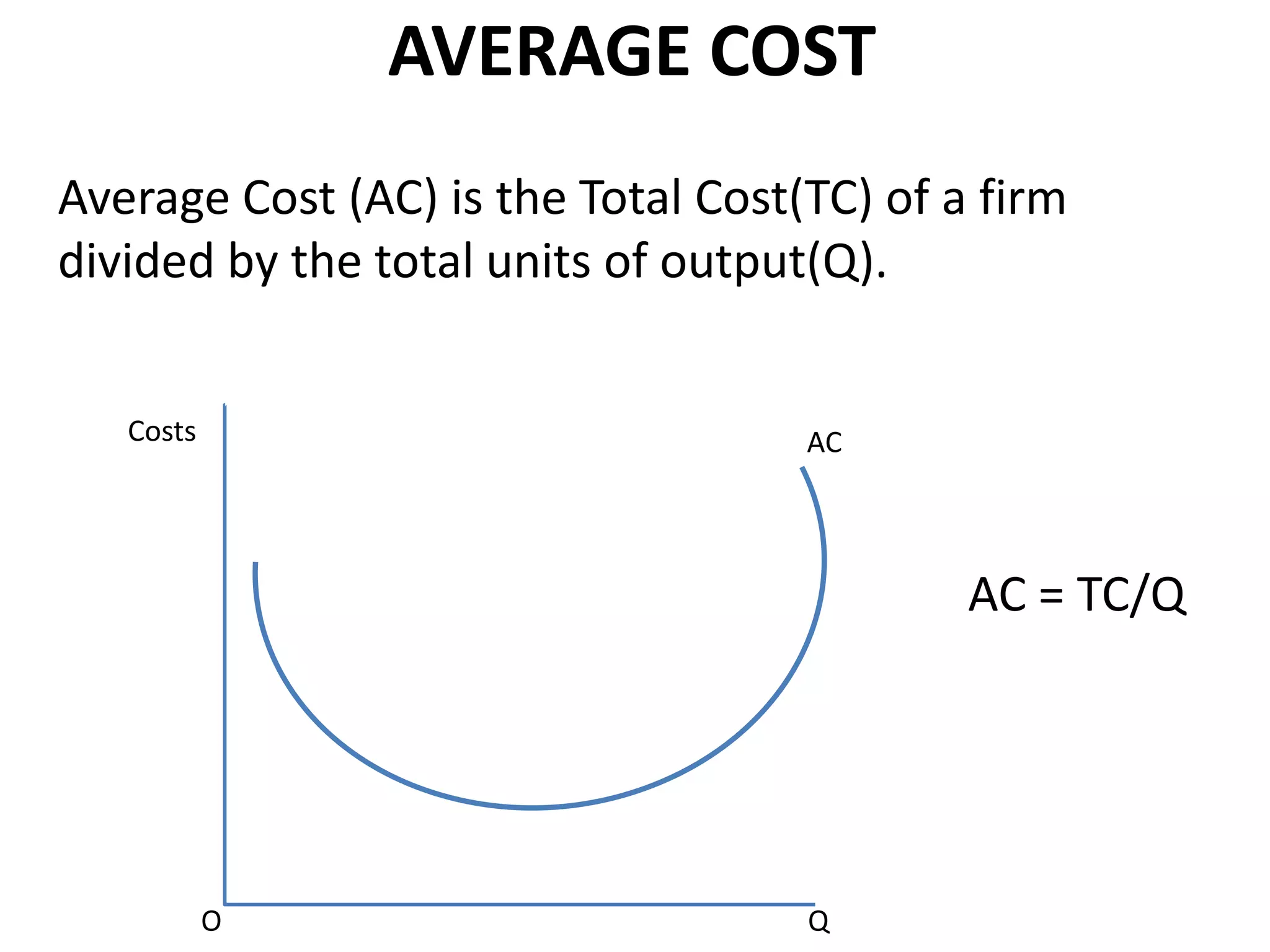

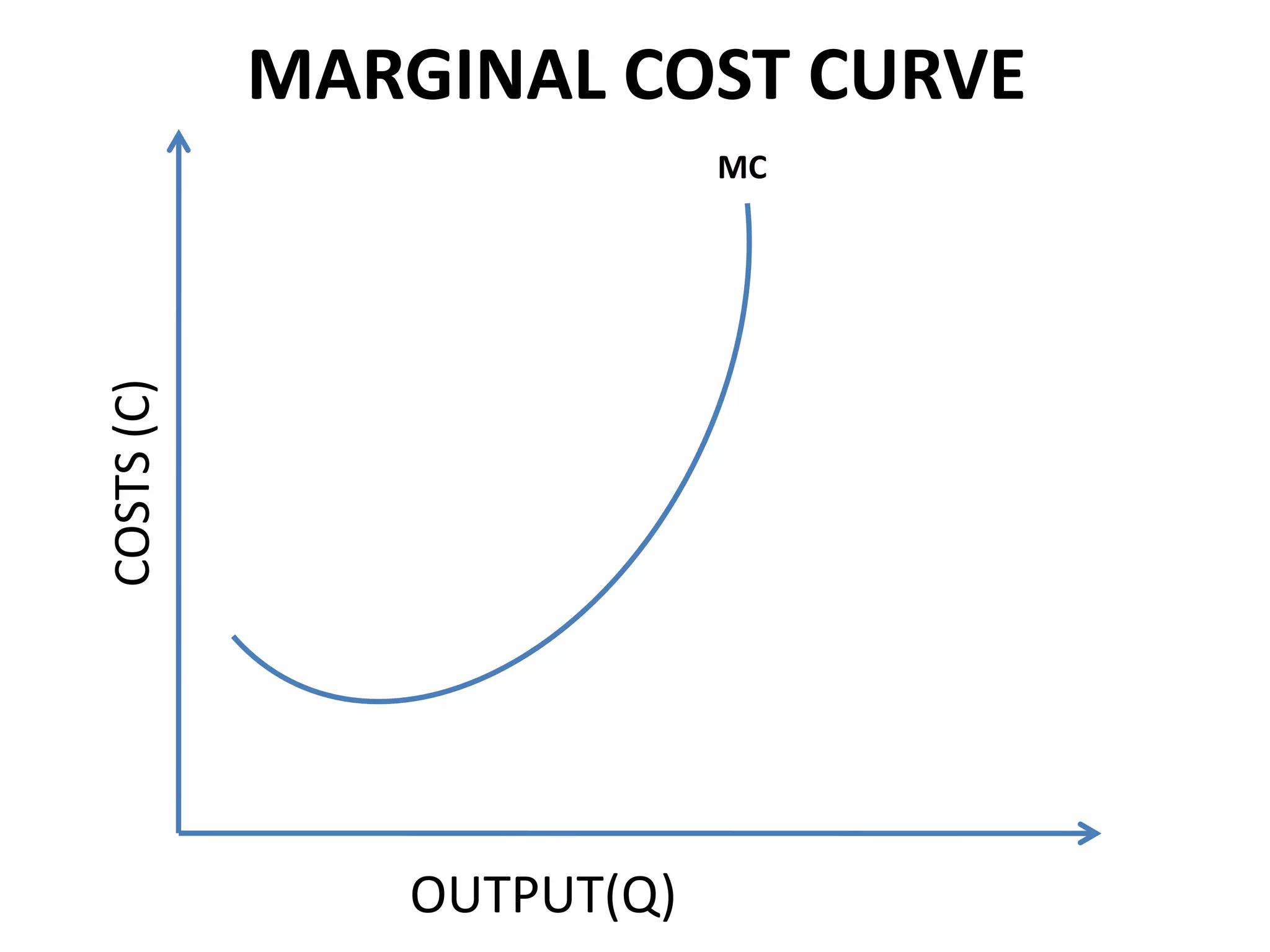

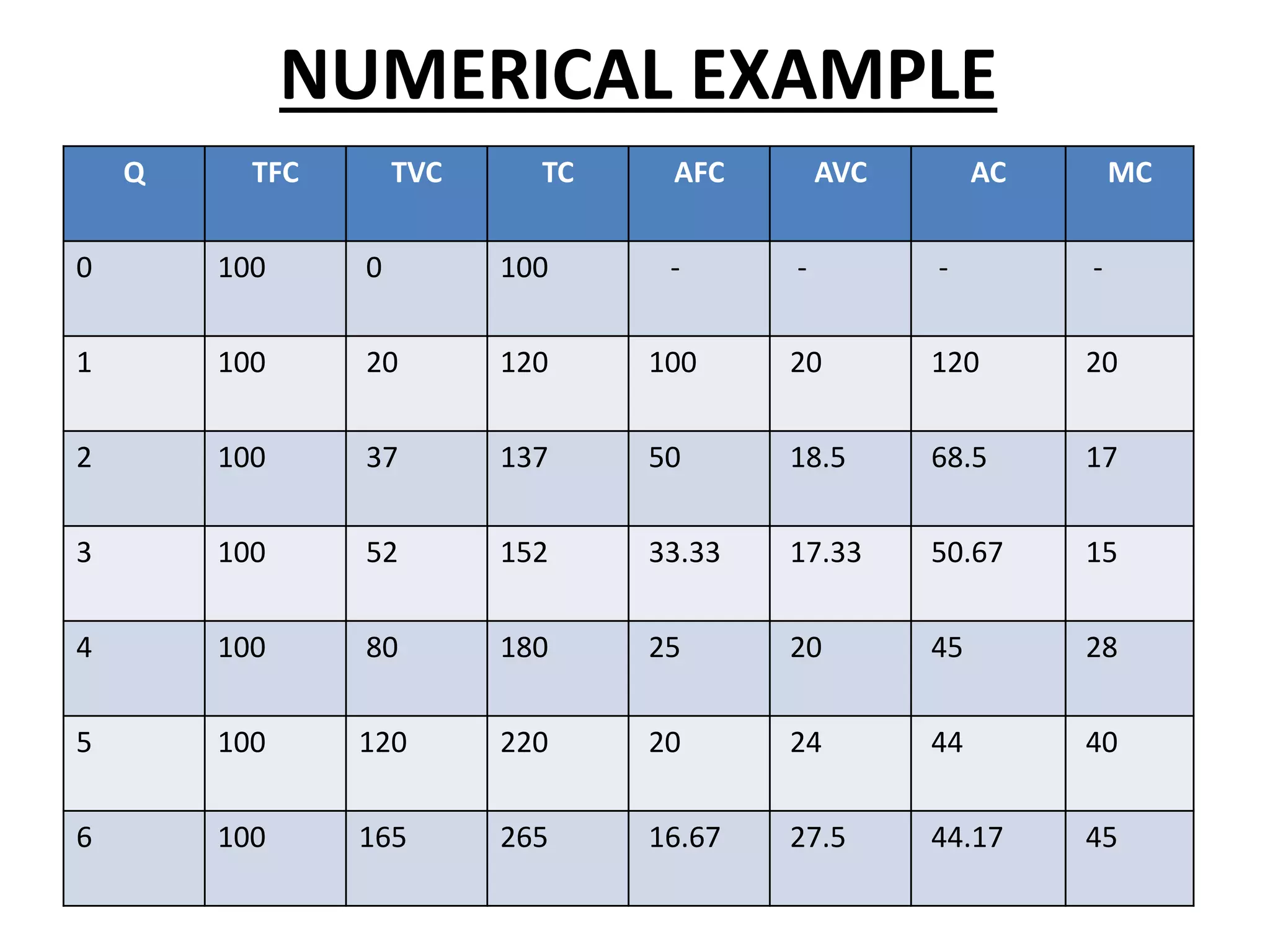

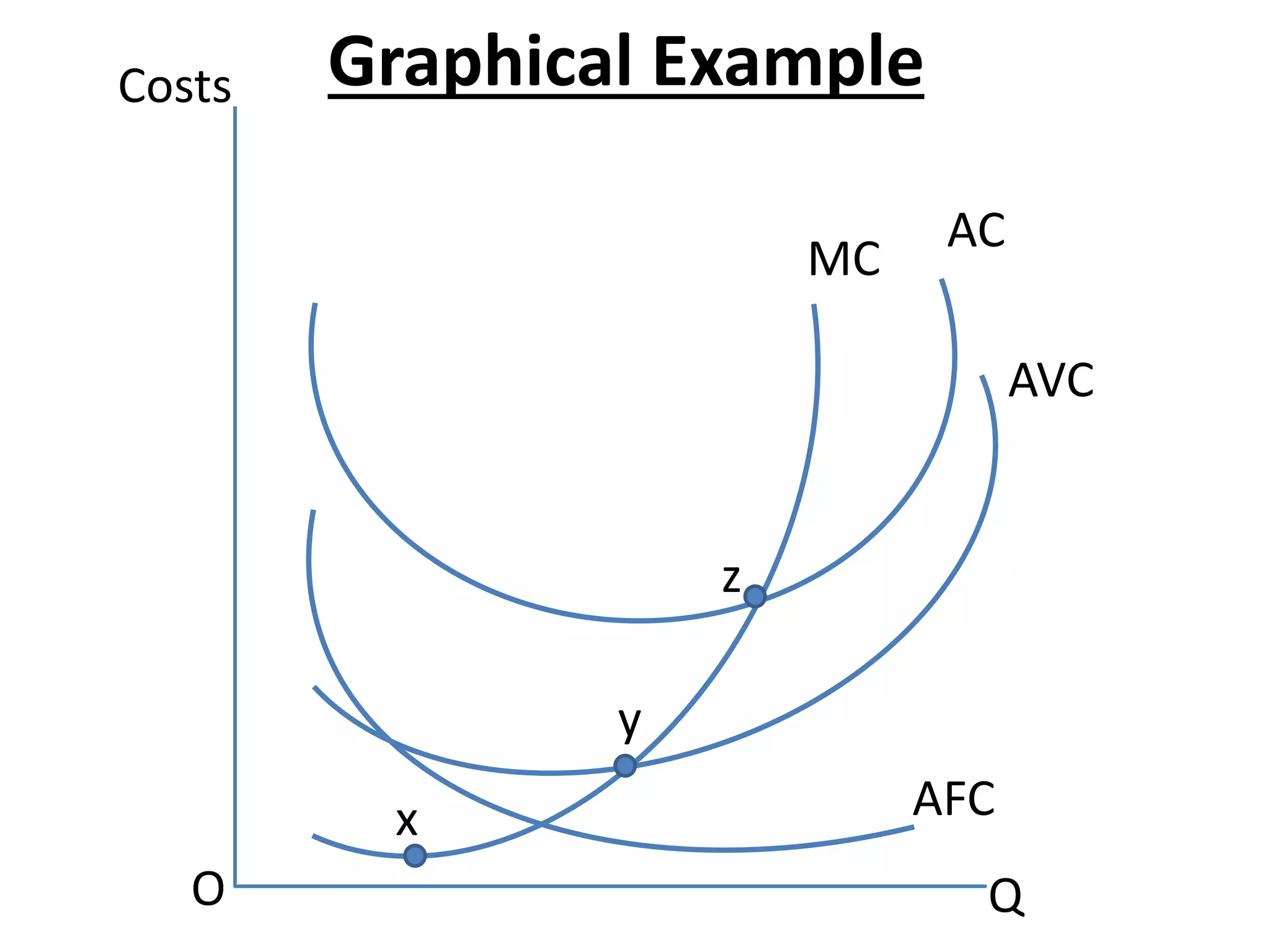

This document discusses different types of costs in economics including total, fixed, variable, average, and marginal costs. It defines each type of cost using mathematical formulas. Total cost is the sum of total fixed costs and total variable costs. As production volume increases, average fixed cost decreases in a rectangular hyperbola shape. Marginal cost is the change in total cost from producing one additional unit and the marginal cost curve is U-shaped, initially high and then decreasing to a minimum point before rising again. The document provides a numerical example to illustrate the different cost concepts.