This document discusses different types of costs involved in production, including:

- Explicit costs which are actual payments, versus implicit costs which are work done without monetary payment

- Private costs accrued by firms/individuals engaged in an activity, versus external/social costs passed to society

- Sunk costs which cannot be recovered and should be ignored in decisions

- Money costs which are payments to factors of production

- Opportunity cost as the next best alternative foregone in producing something

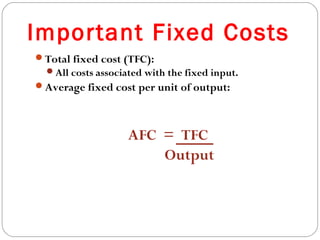

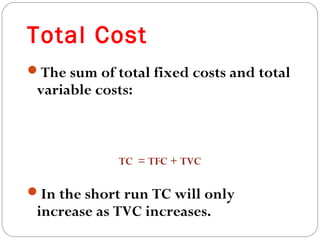

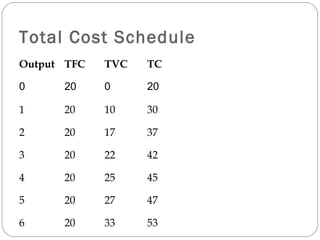

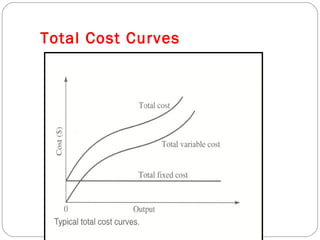

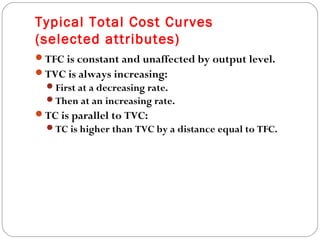

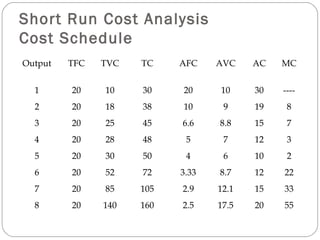

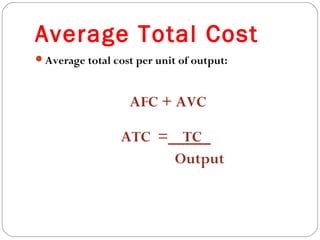

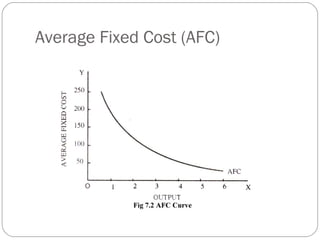

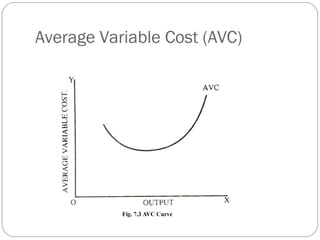

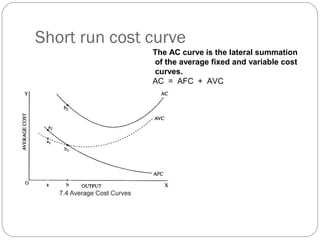

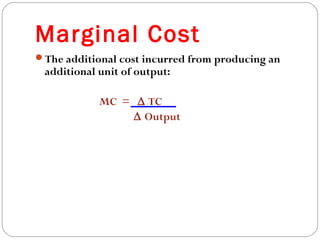

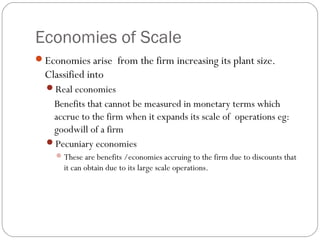

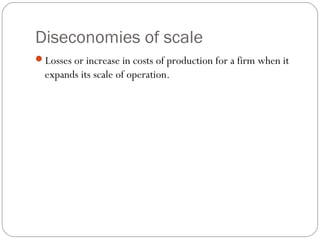

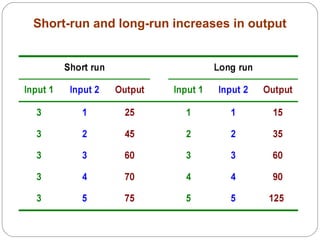

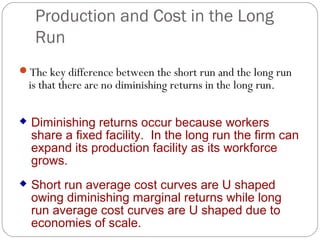

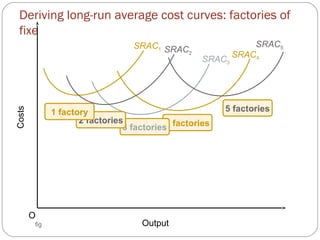

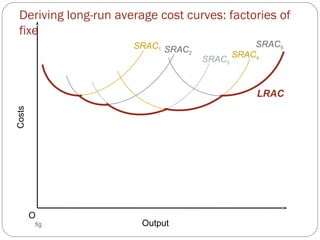

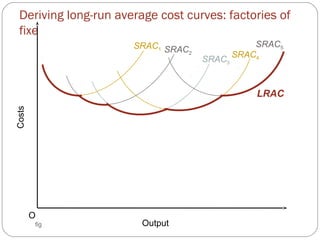

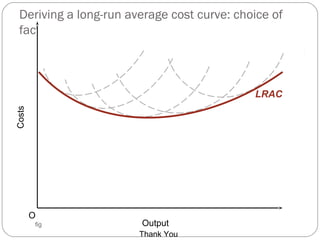

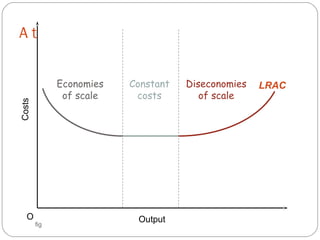

It also explains concepts like fixed costs, variable costs, total costs, average costs and marginal cost, and how they relate in the short-run and long-run, including economies and diseconomies of scale. Diagrams are used to depict