Downloaded 14 times

![THINKstrategies Strategic Consulting Services

How to Succeed and Thrive in

the Rapidly Changing SaaS

Marketplace – Best Practices

Presented by,

Jeff Kaplan

Managing Director

THINKstrategies

jkaplan@thinkstrategies.com

781-431-2690

©2011, THINKstrategies [www.thinkstrategies.com]

Slide 3](https://image.slidesharecdn.com/webinar1bestpracticestohelpyousucceedintherapidlychangingsaasmarketplace-110701143939-phpapp01/75/Webinar1-of-3-in-a-series-Best-Practices-to-Help-You-Succeed-in-the-Rapidly-Changing-SaaS-Marketplace-3-2048.jpg)

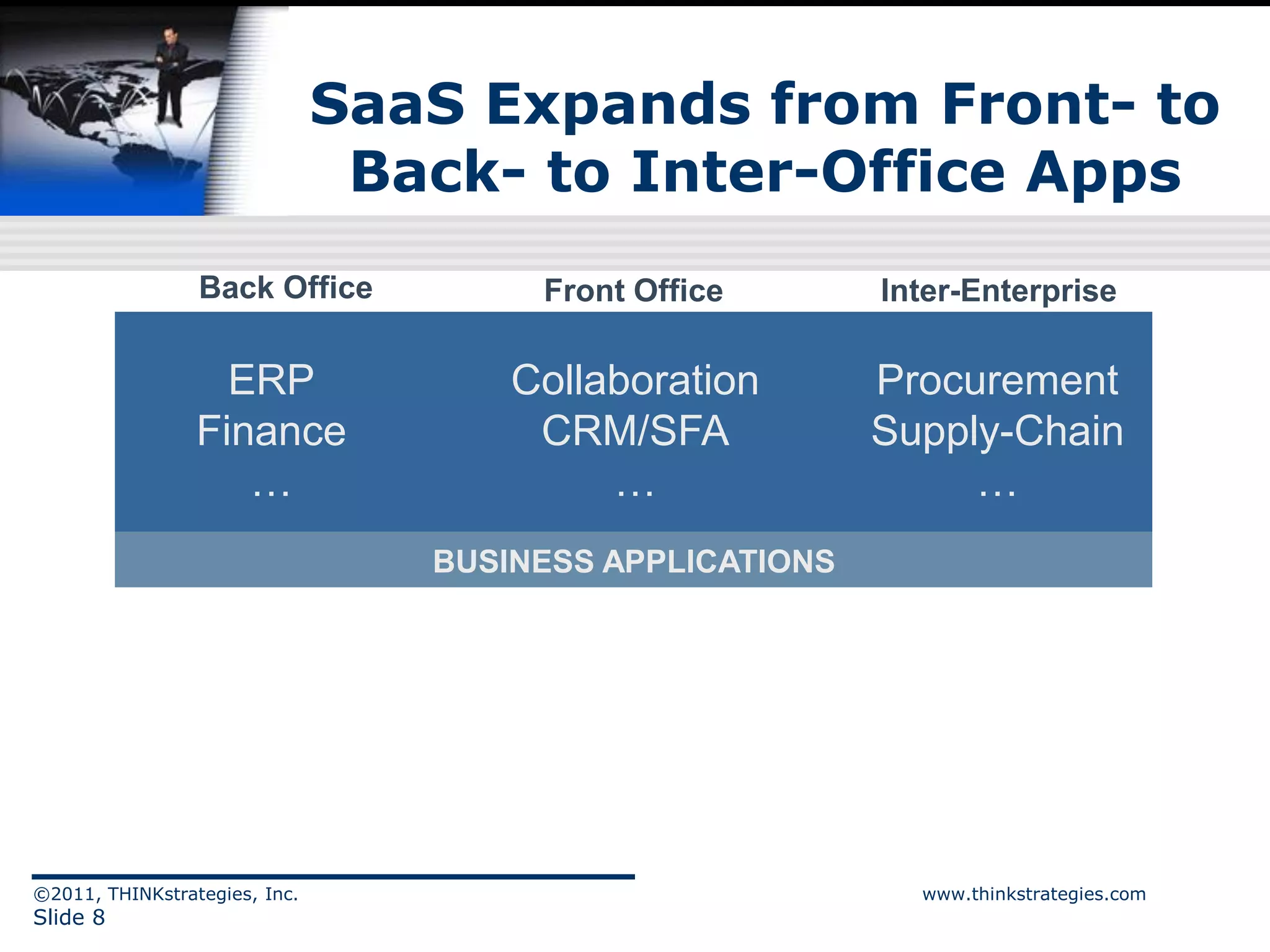

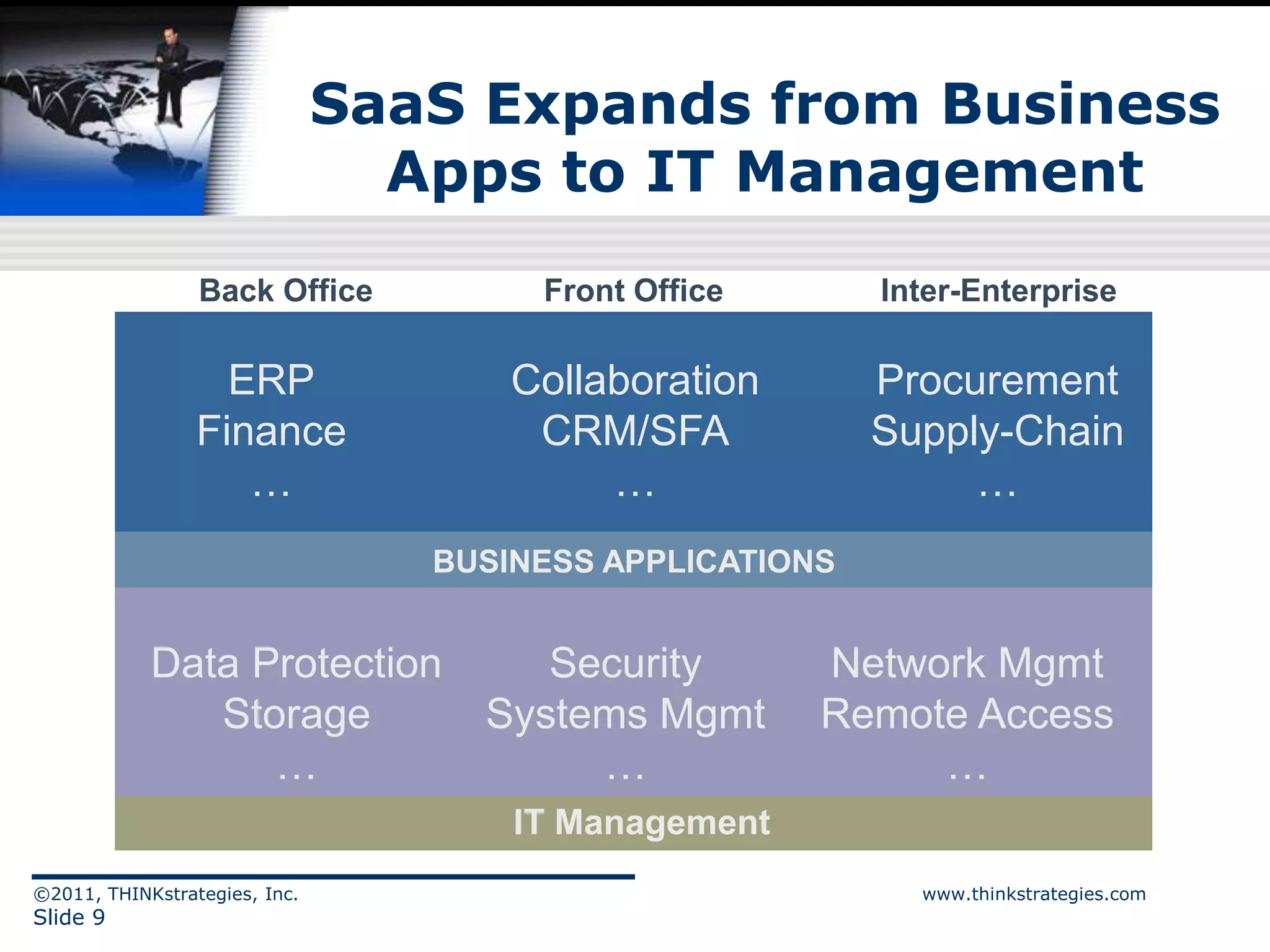

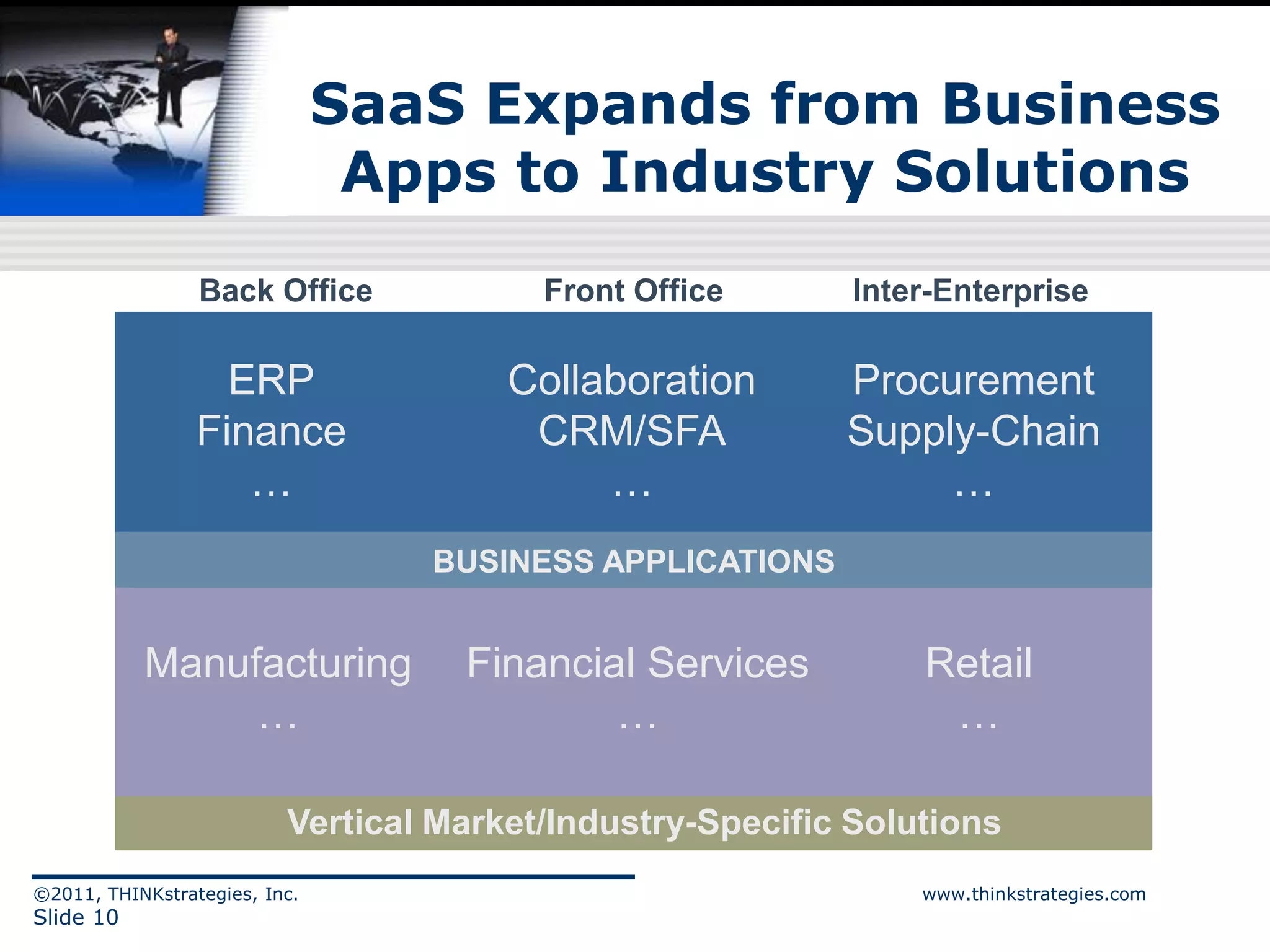

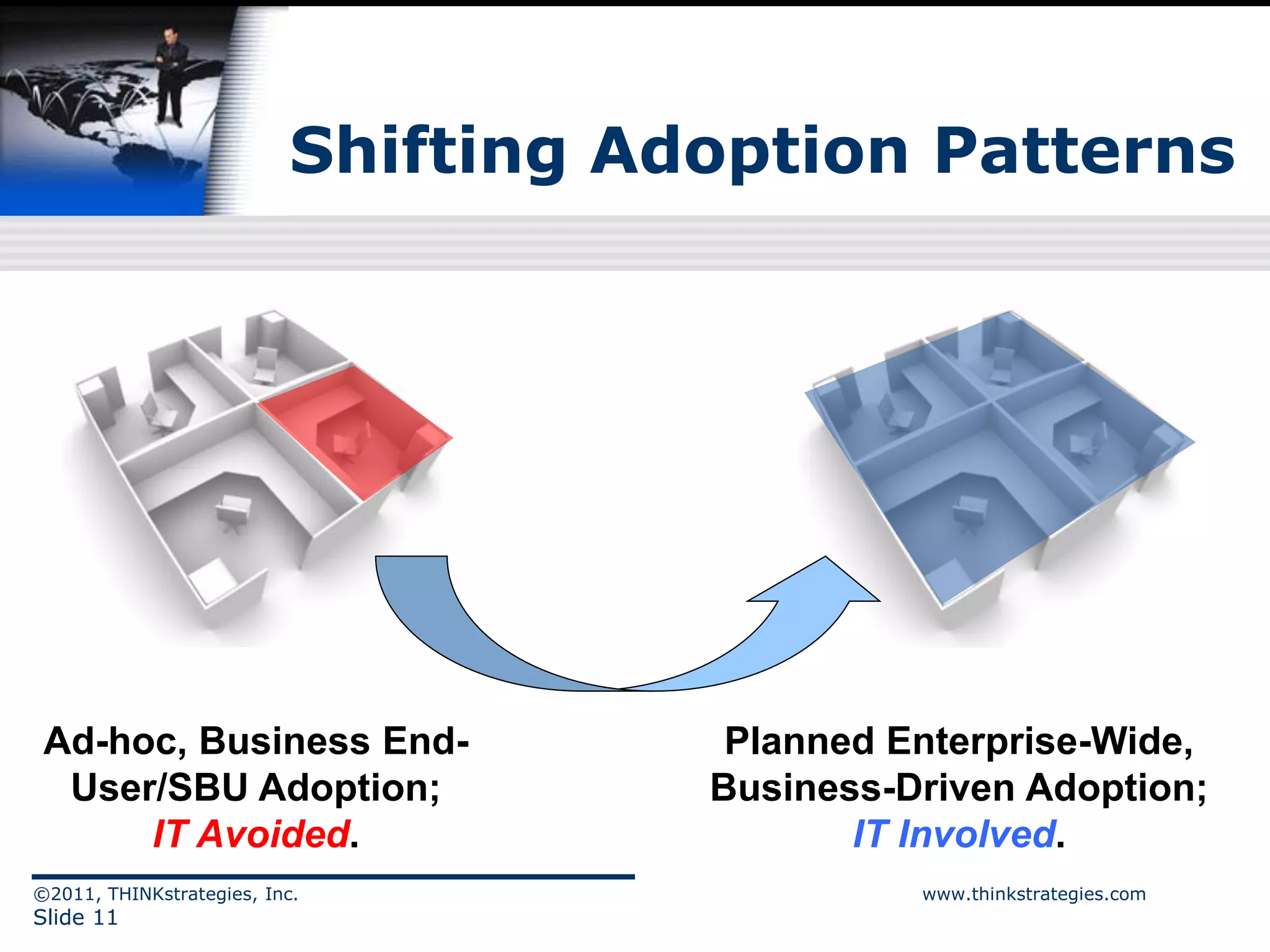

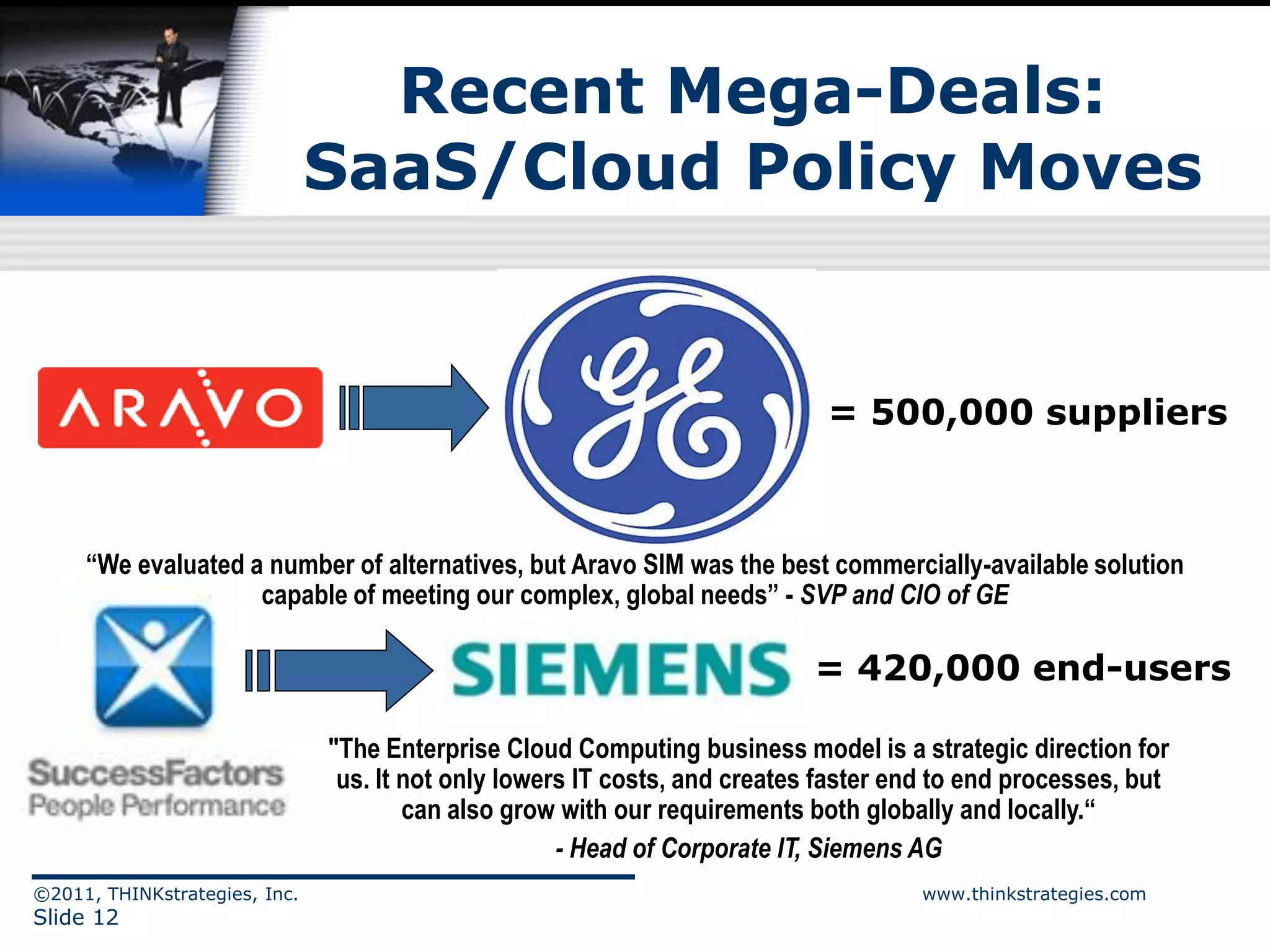

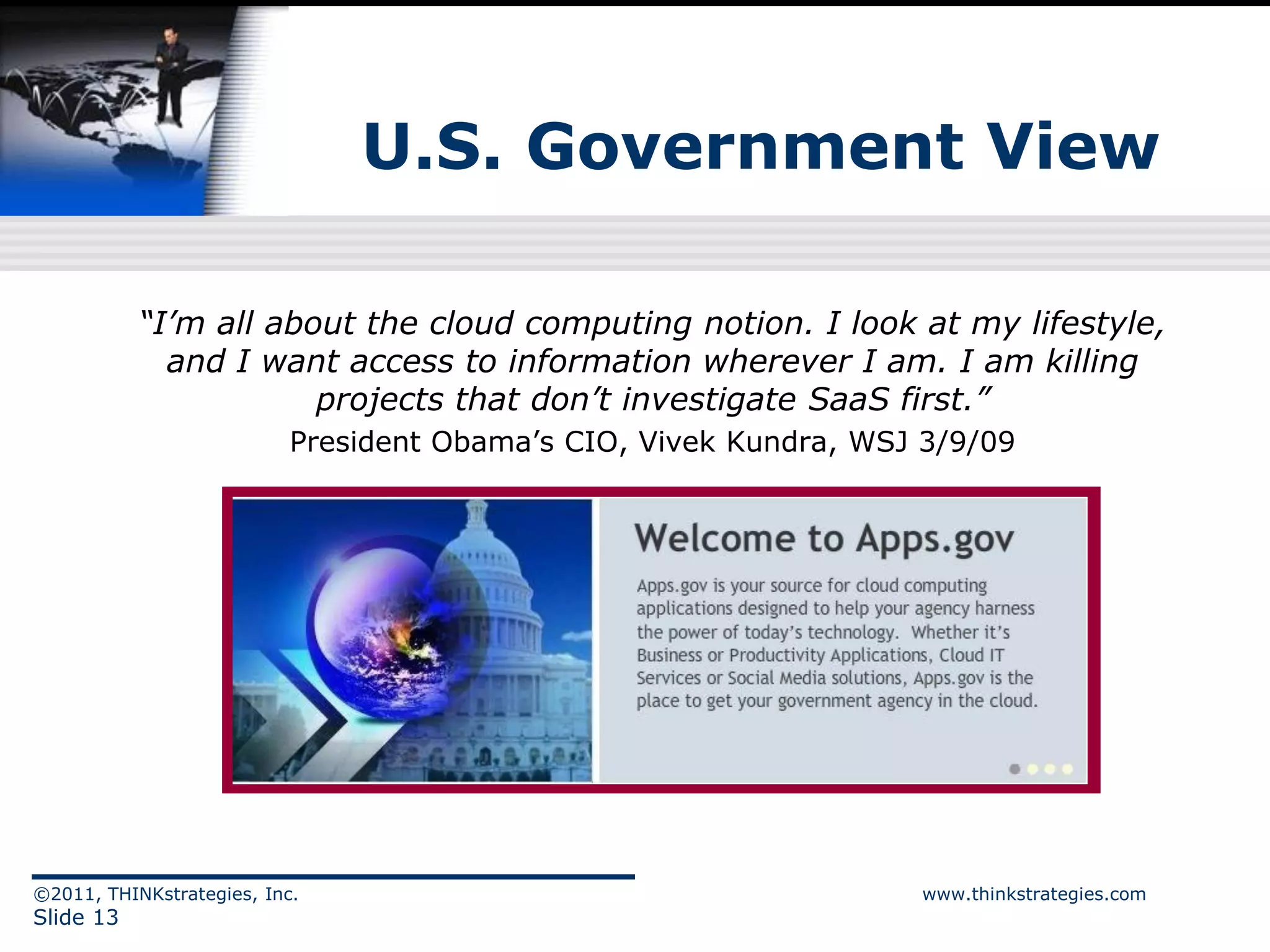

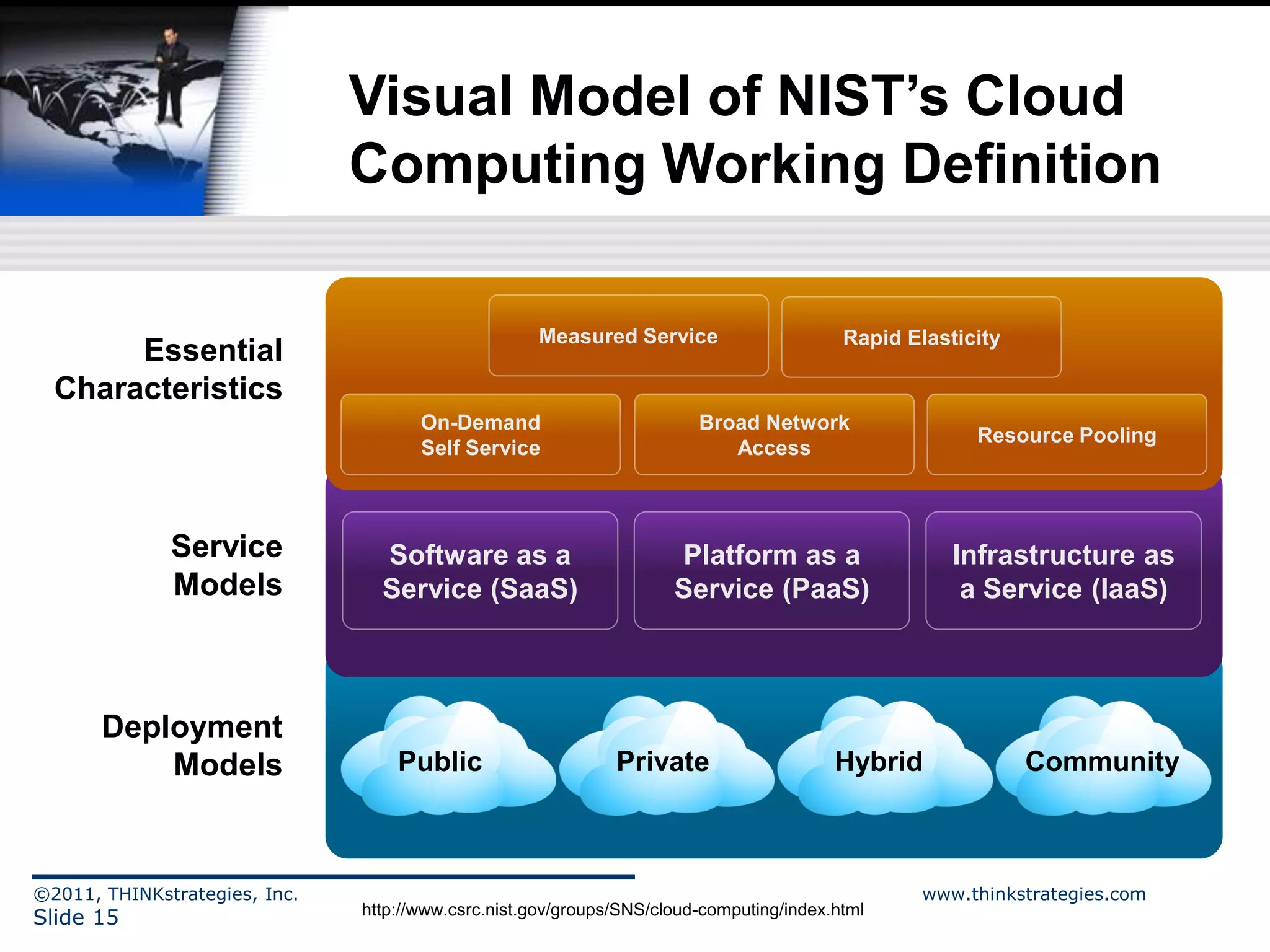

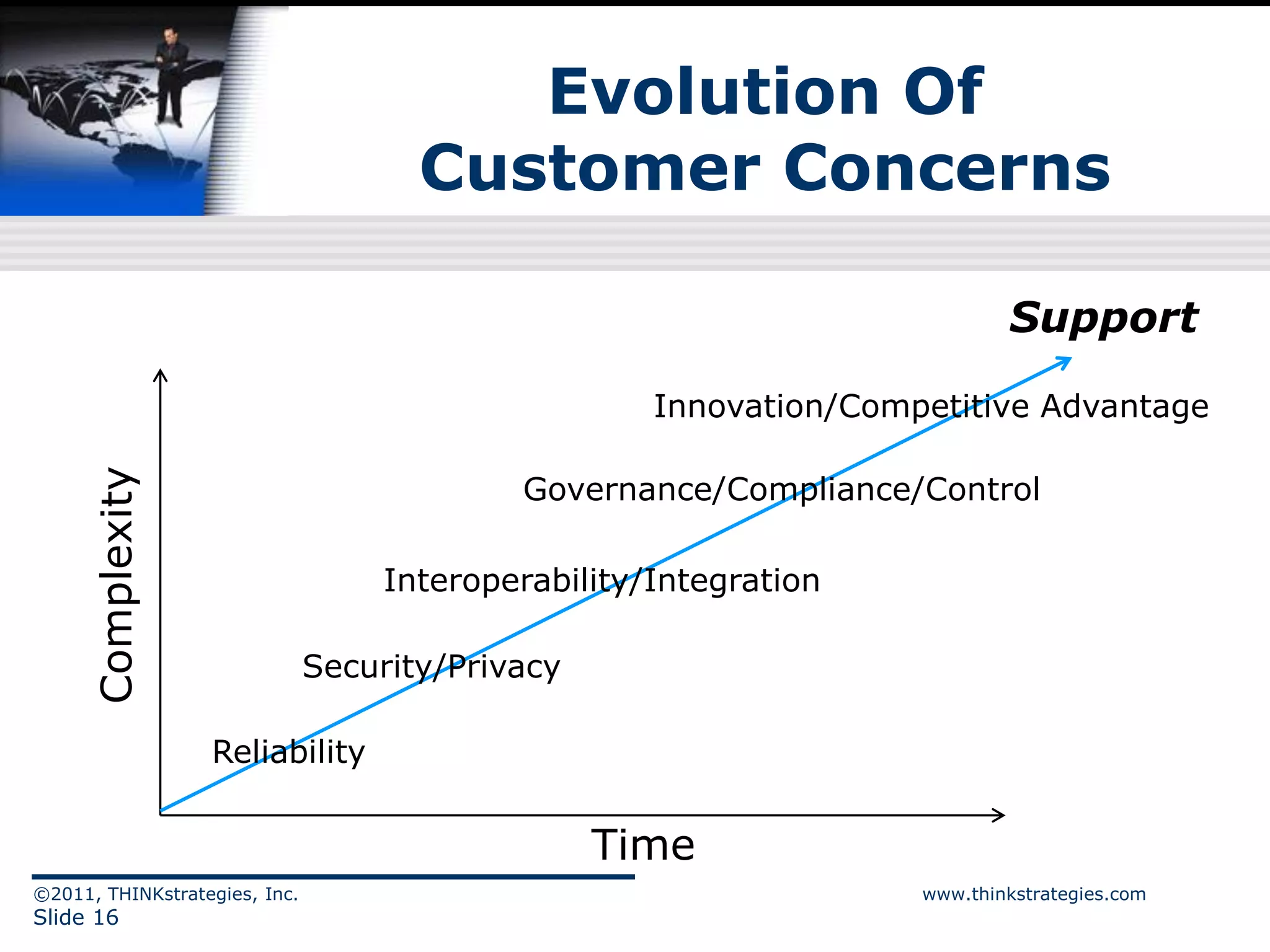

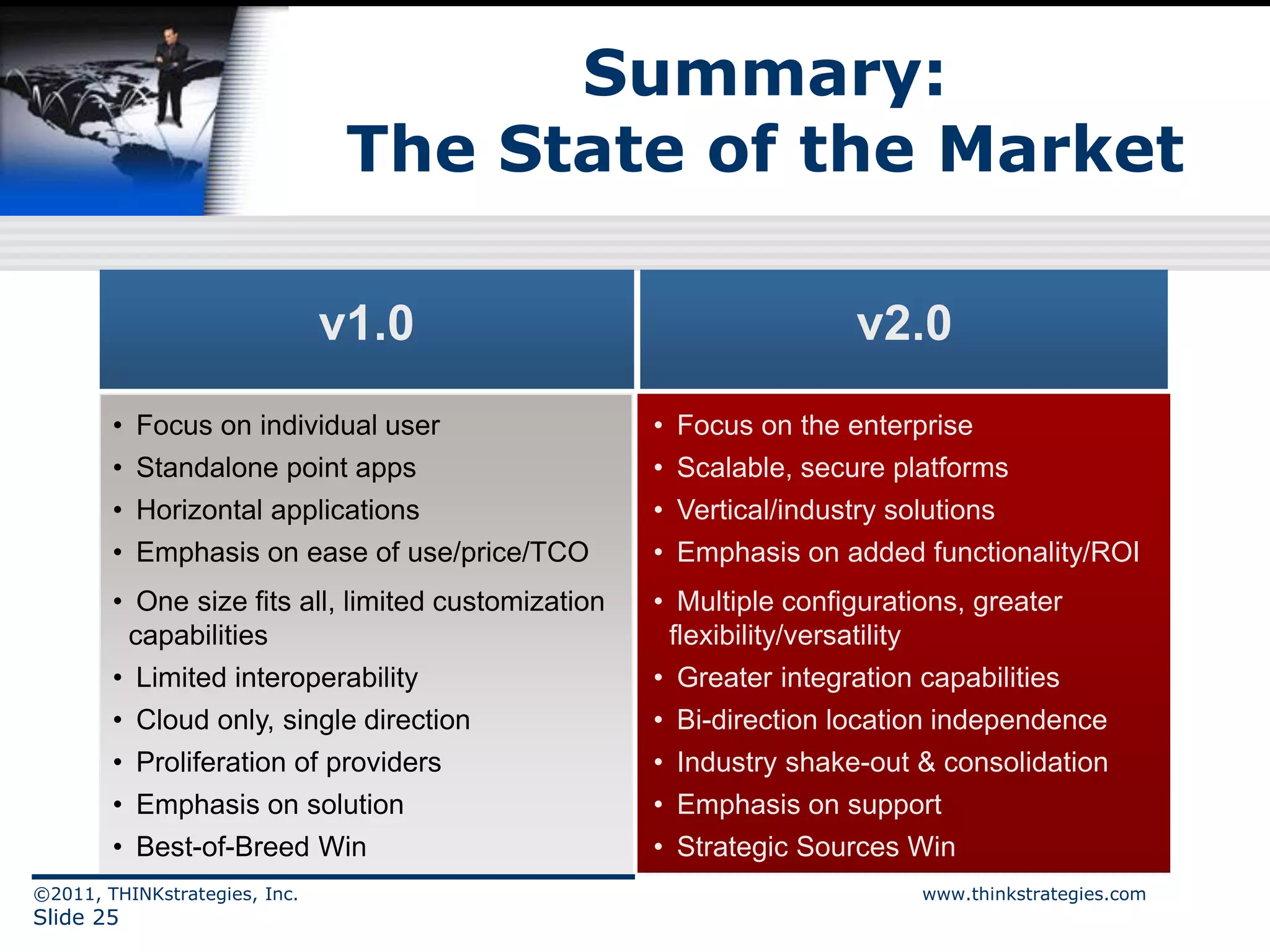

This document discusses best practices for succeeding in the rapidly changing software as a service (SaaS) marketplace. It covers macro trends driving adoption of cloud computing like consumerization, the shortcomings of legacy software, and changing customer needs and expectations. The SaaS market is expanding from business applications to include IT management, vertical industry solutions, and hybrid deployment models. Recent large enterprise deals and government policies indicate strategic adoption of cloud computing. The document provides visual models to define cloud computing and the evolution of customer concerns regarding new service models.