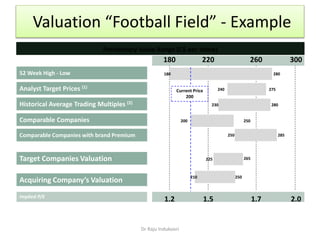

The document discusses several valuation models: 1. Discounted cash flow (DCF) model, which discounts future cash flows. 2. Tobin's Q model, which compares a firm's market value to replacement cost of assets. 3. Market multiples model, which uses multiples like price-to-earnings to value firms. 4. Valuation football field (FBF) provides an overview of valuations from different sources.