Downloaded 89 times

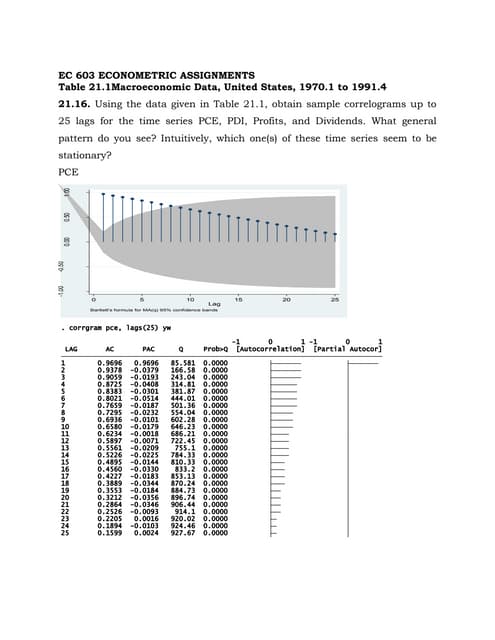

The document outlines the concept of unit root tests, including definitions and methodologies for testing non-stationarity in time series data using tests such as the Dickey-Fuller, Augmented Dickey-Fuller, and Phillips-Perron tests. It provides a step-by-step approach to conducting these tests and highlights the differences among these tests regarding autocorrelation and heteroskedasticity. Additionally, it emphasizes the importance of graphical analysis as a preliminary step in time series analysis.