Download as PDF, PPTX

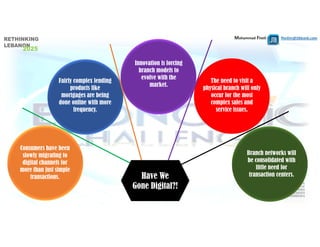

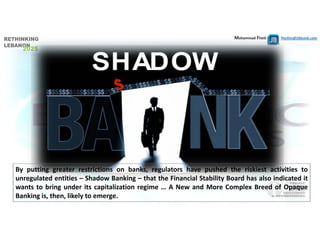

The document discusses various threats and challenges faced by the banking sector, emphasizing the impact of technology, changing customer expectations, and regulatory pressures on economic growth. It highlights the importance of adapting organizational capabilities to meet new demands, while navigating the complexities of risk management and compliance. Additionally, the document addresses the rise of shadow banking as a consequence of stricter regulations on traditional banks.

![139[1] التبادل التلقائي للمعلومات لغايات ضريبية](https://cdn.slidesharecdn.com/ss_thumbnails/1391-170725091616-thumbnail.jpg?width=640&height=640&fit=bounds)