Downloaded 23 times

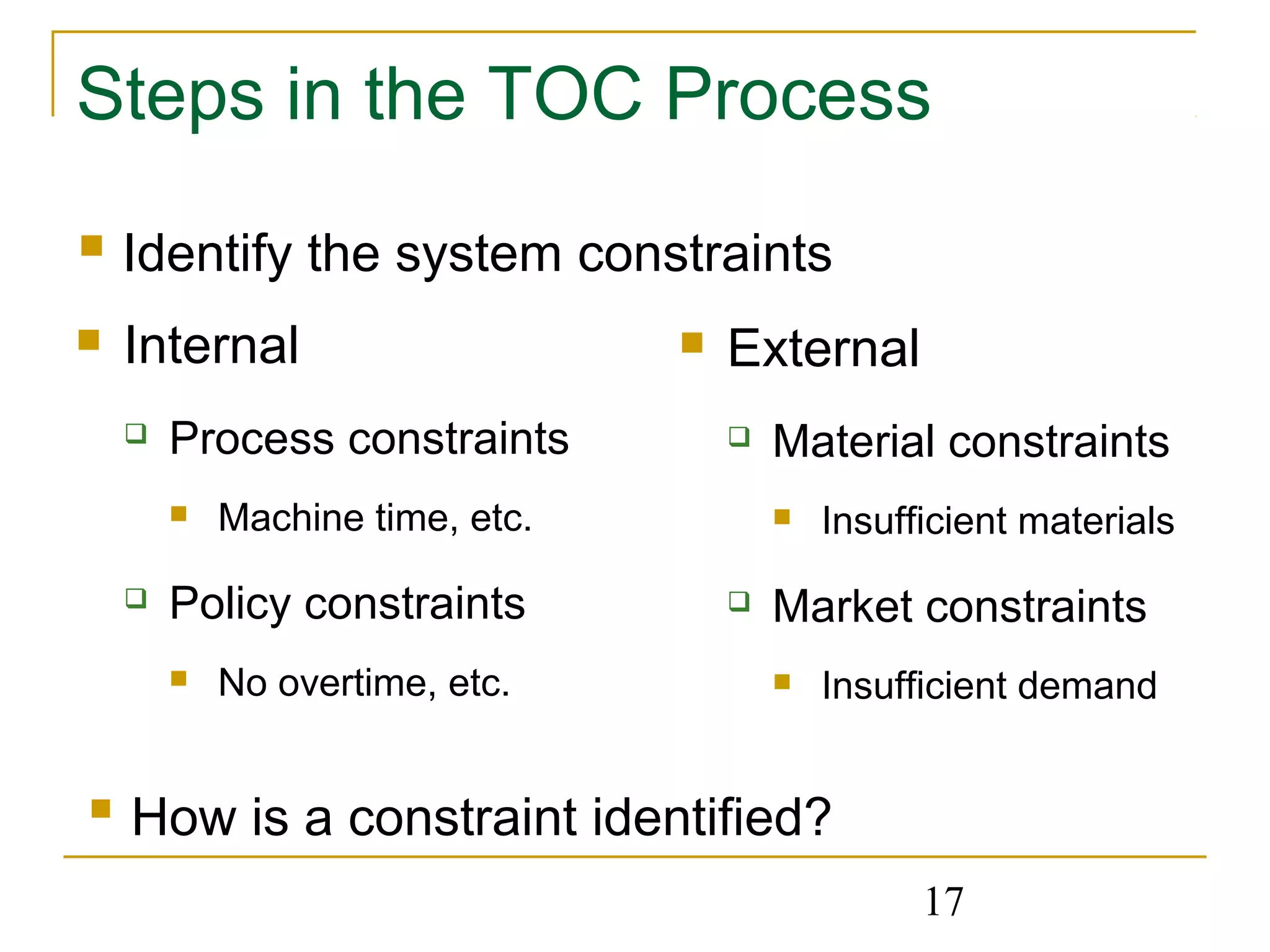

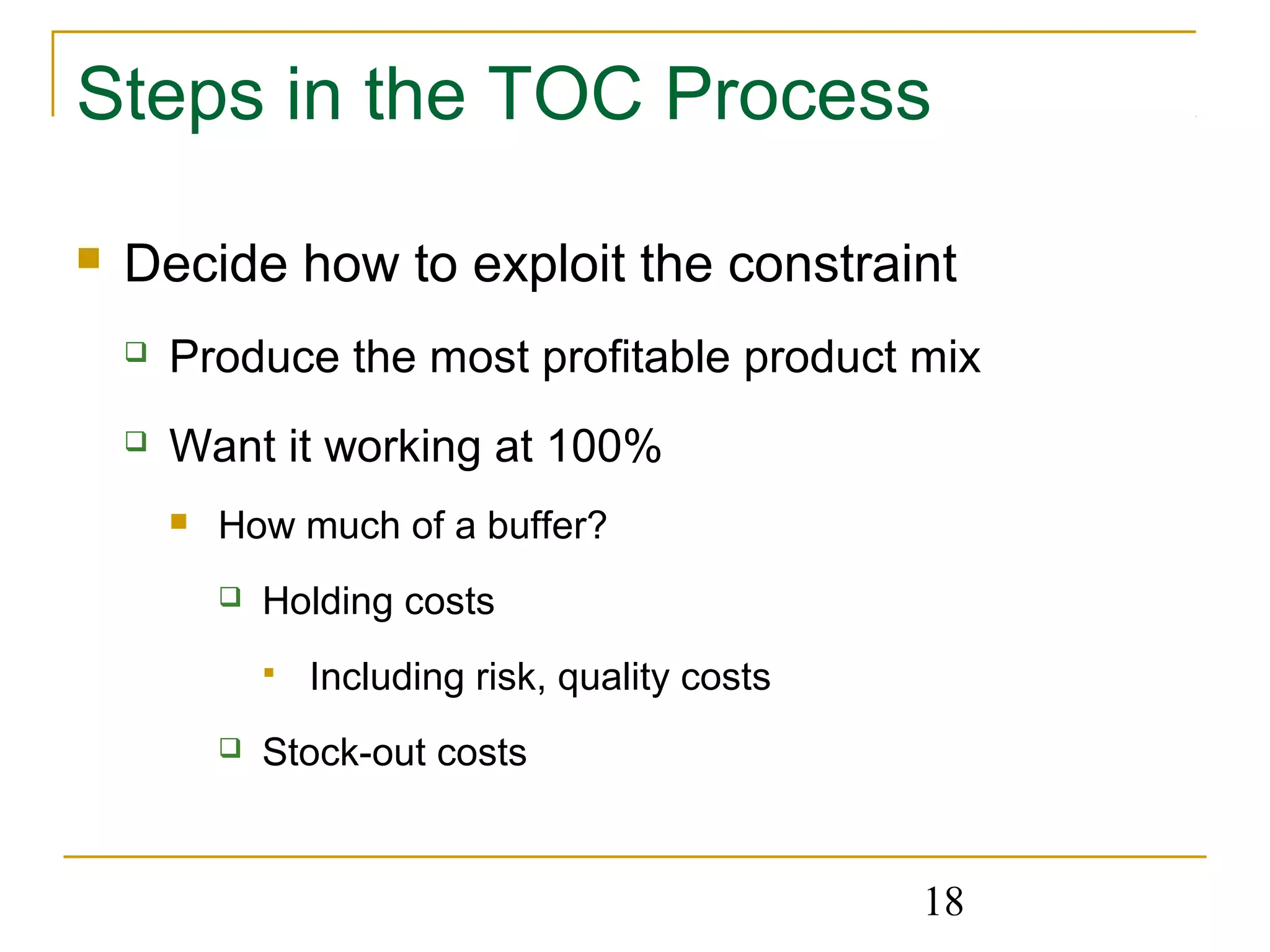

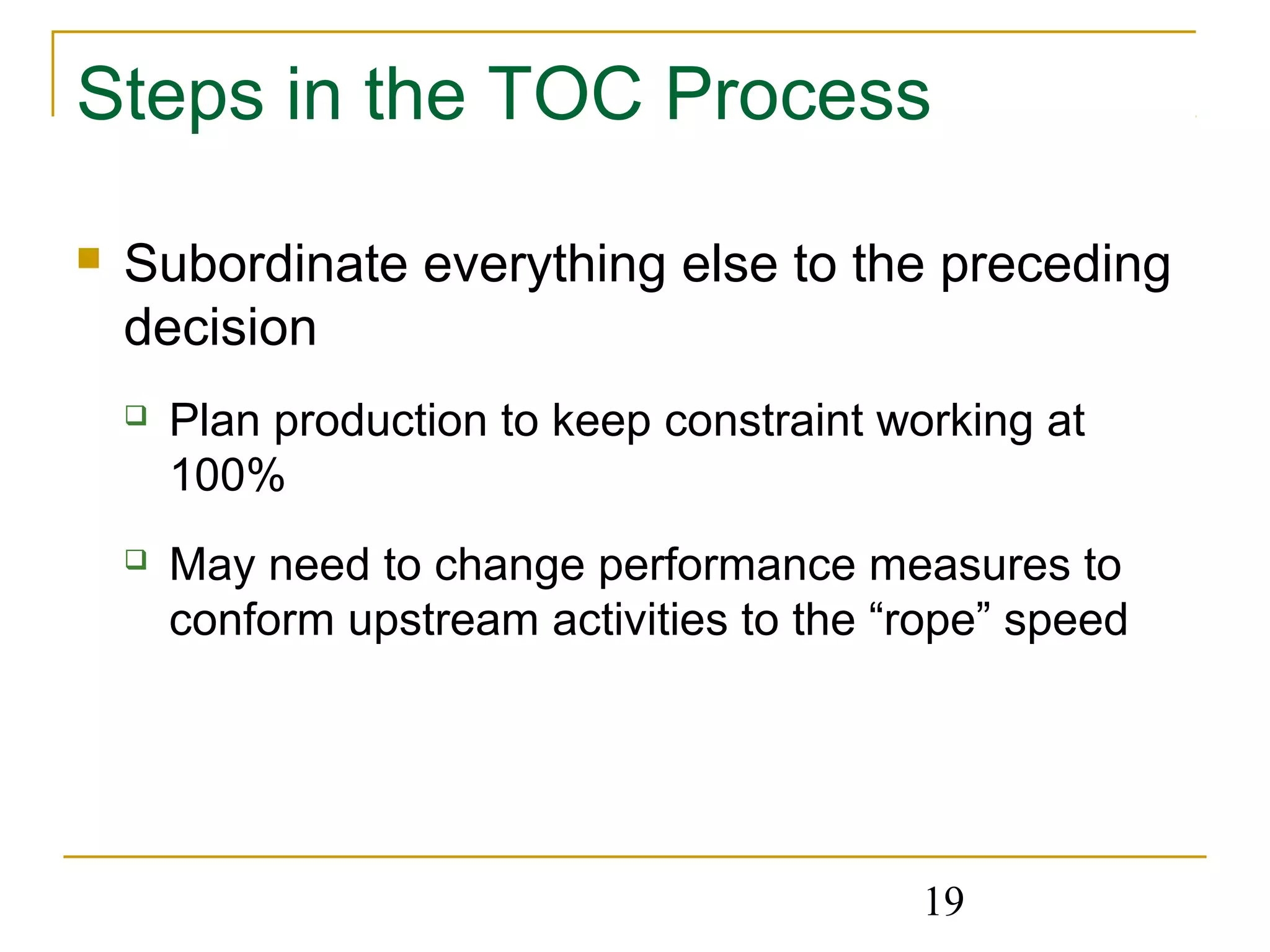

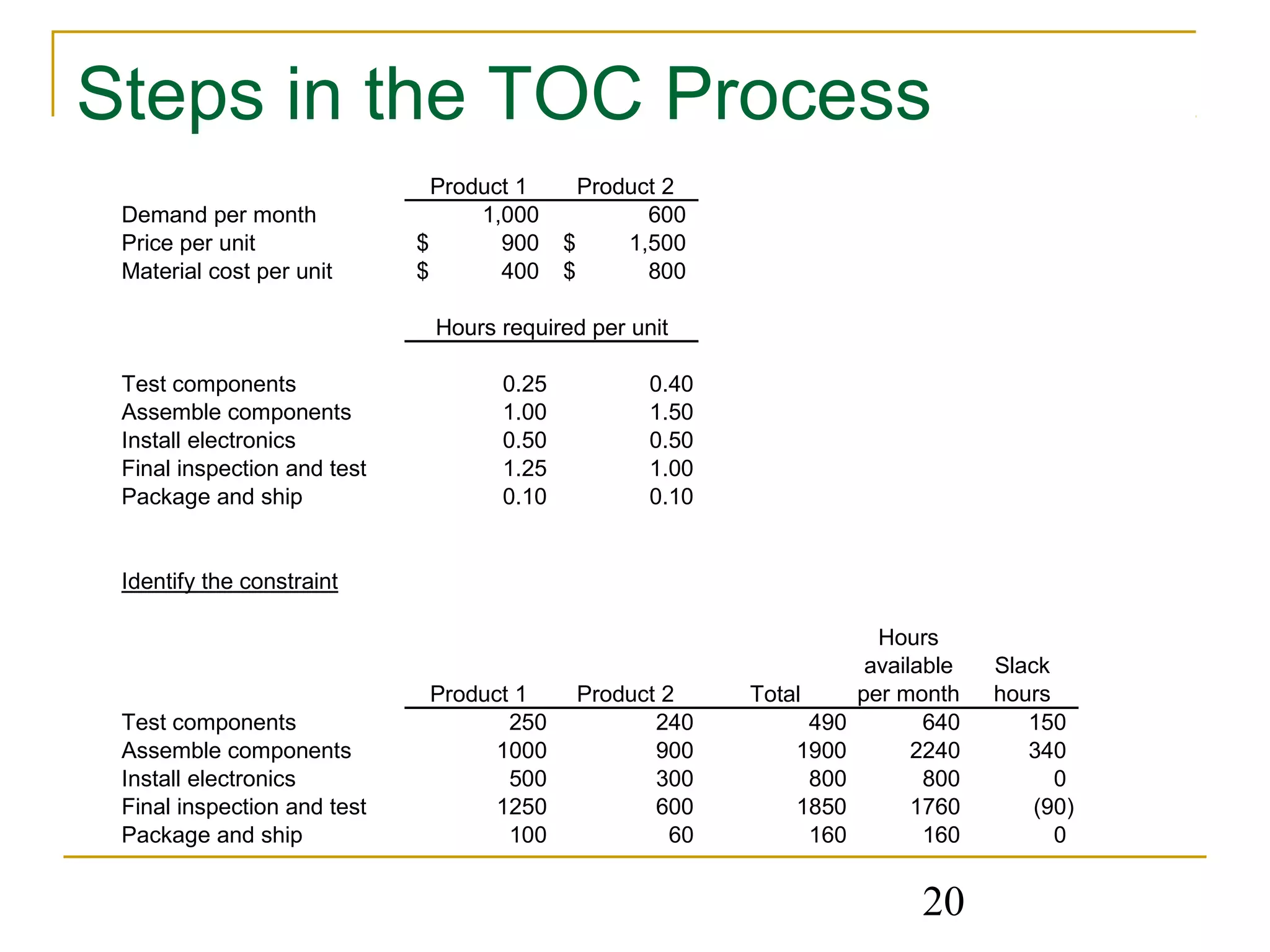

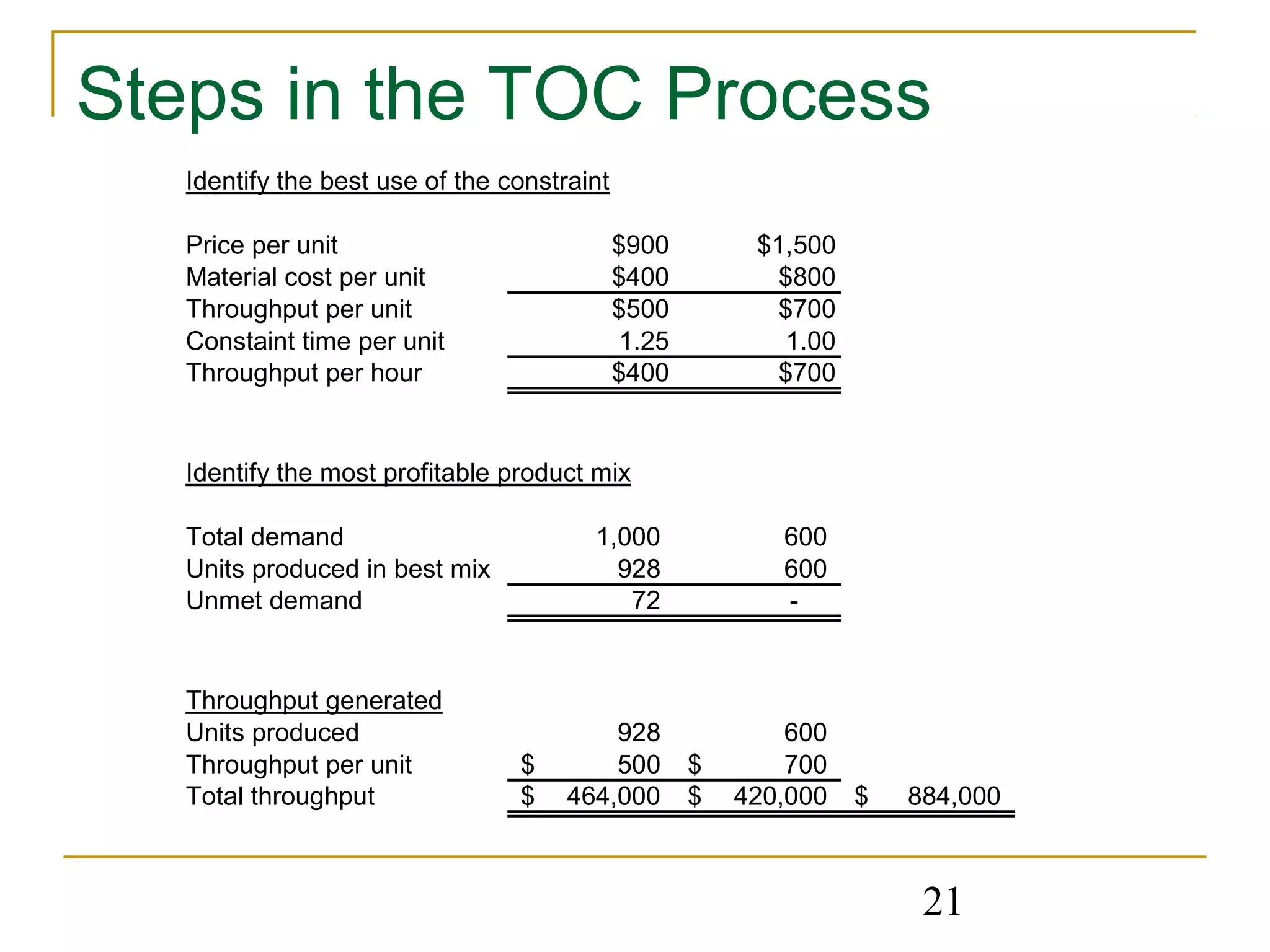

The Theory of Constraints (TOC) is a management philosophy that identifies the constraints limiting an organization from achieving its goals and focuses on restructuring processes to better exploit constraints. The key steps are to identify the system's constraints, decide how to best exploit each constraint to maximize throughput or productivity, and subordinate all other decisions and processes to supporting the constraint. TOC uses linear programming to determine the optimal product mix and production levels given capacity constraints. The goal is to keep constraints fully utilized to maximize profits in the short-term.

![[Whitepaper] The “Theory of Constraints:” What’s Limiting Your Organization?](https://cdn.slidesharecdn.com/ss_thumbnails/theoryof-210212191639-thumbnail.jpg?width=640&height=640&fit=bounds)