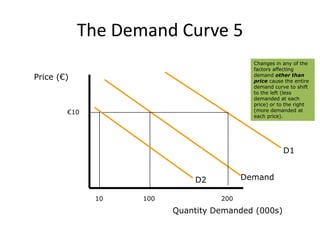

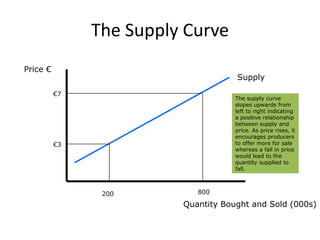

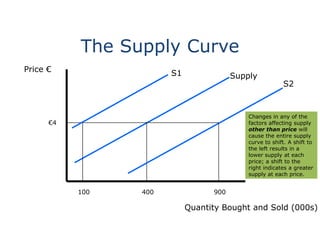

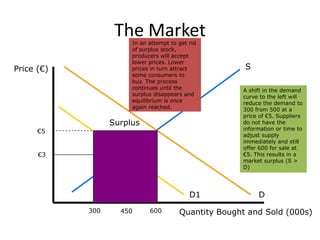

1) The market system consists of consumers who create demand and businesses that produce supply. When demand and supply are equal, the market reaches equilibrium. 2) Changes in factors like income, tastes, prices of other goods can cause the demand curve to shift, changing the quantity demanded at each price. Supply is influenced by costs of production and technology, and its curve shifts with these factors. 3) When demand decreases at a given price, a surplus occurs as supply exceeds demand. Prices fall to eliminate the surplus until equilibrium is restored. Conversely, a leftward supply shift creates shortages, raising prices until equilibrium is reestablished.