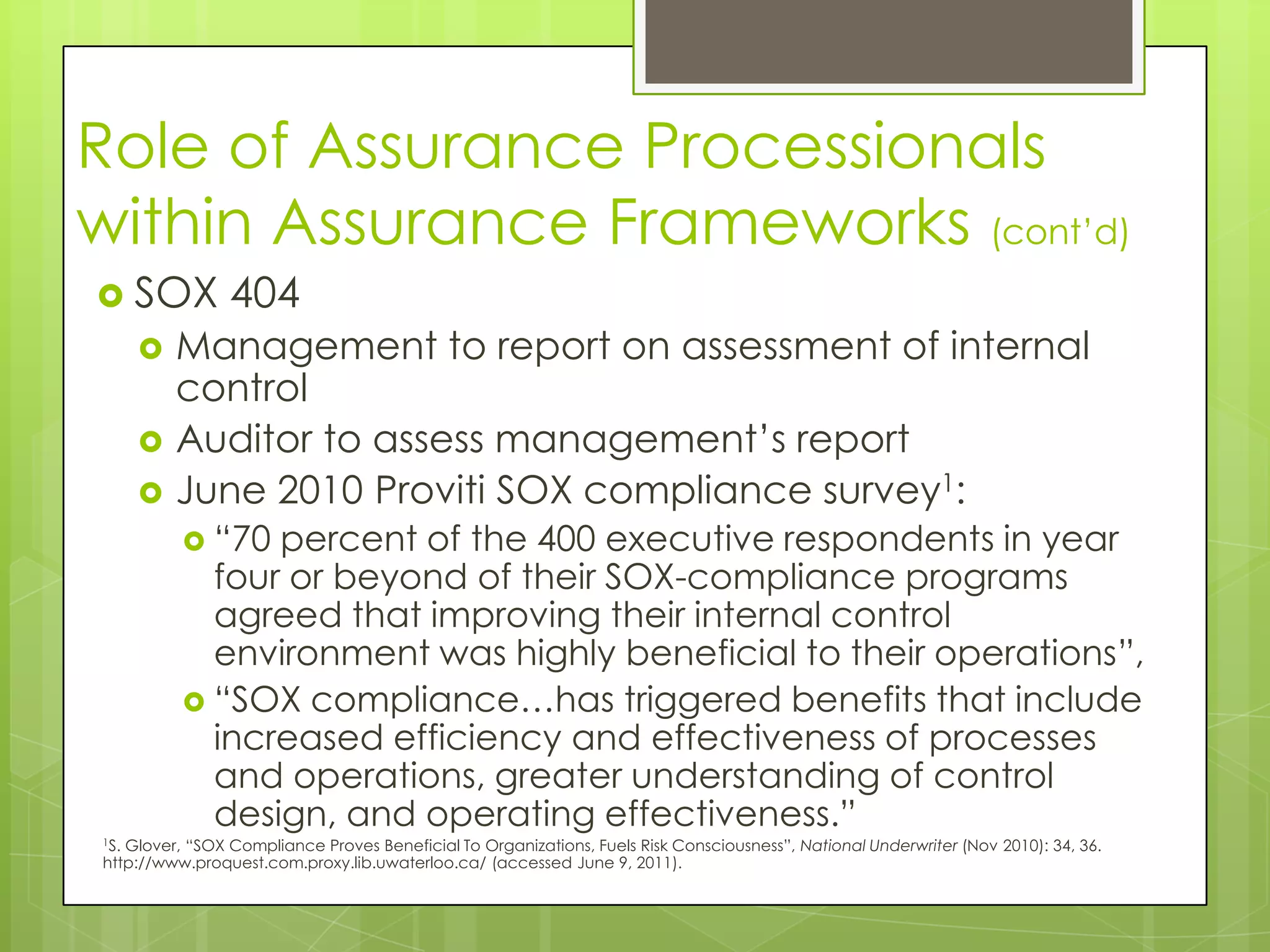

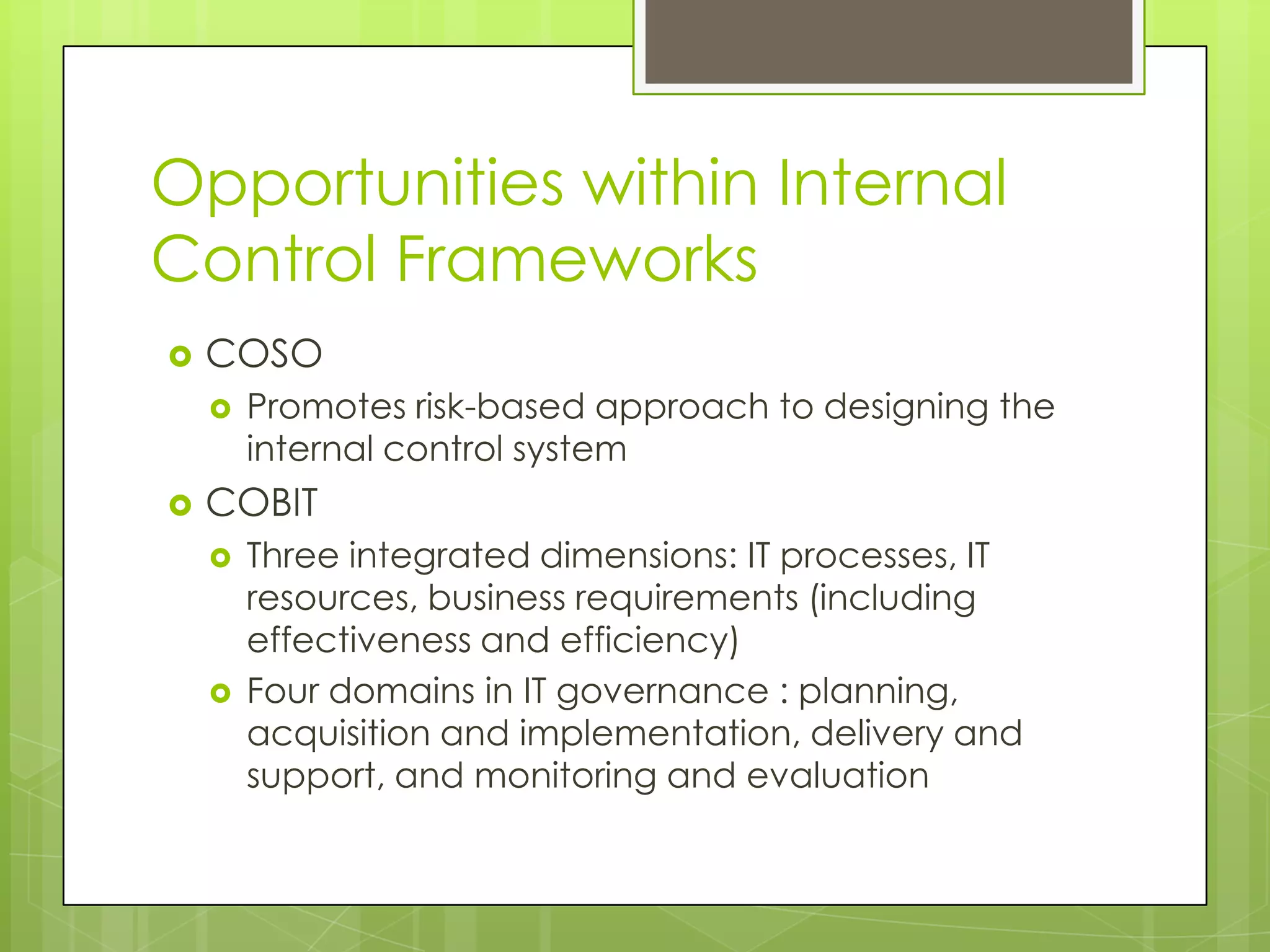

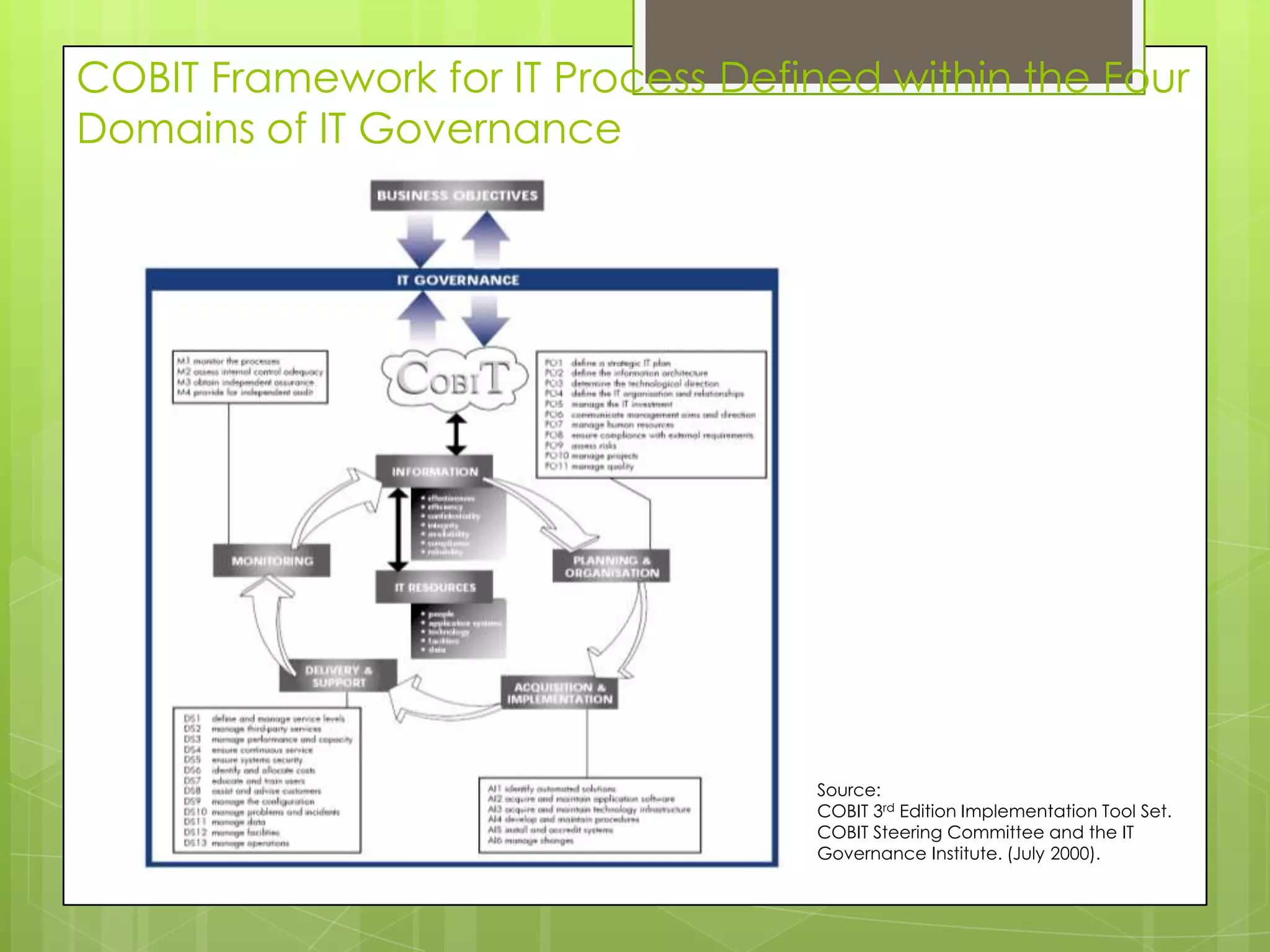

The document discusses the role of assurance professionals within assurance frameworks, highlighting the impact of the Sarbanes-Oxley Act (SOX) on internal control assessments and auditing practices. It emphasizes the benefits of SOX compliance, the importance of robust internal controls, and the utilization of methodologies such as COSO and COBIT for effective governance. Additionally, it addresses the evolving responsibilities of internal auditors and the demand for consulting services in audit and risk management.

![Vibe Coding vs. Spec-Driven Development [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/vibecodingvsspecdrivendevelopment-251209105622-43f455e7-thumbnail.jpg?width=640&height=640&fit=bounds)

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)