This document provides an overview of key concepts related to auditing, including:

- The objectives of an audit are to obtain reasonable assurance about whether financial statements are free from material misstatement and to report on the financial statements.

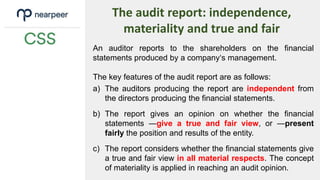

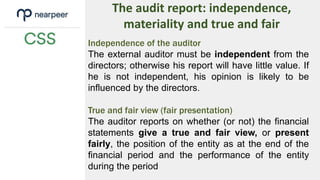

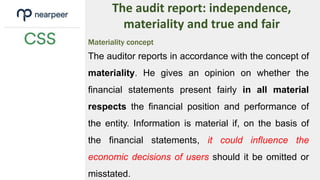

- An auditor must be independent, consider materiality, and determine if financial statements present a true and fair view.

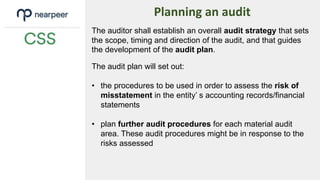

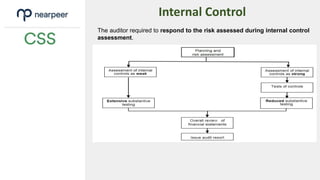

- Planning an audit involves assessing risks, developing an audit strategy and plan, and determining appropriate audit procedures.

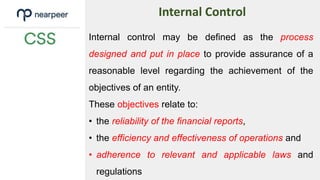

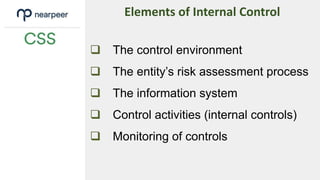

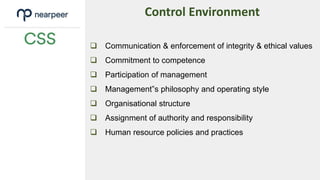

- Internal controls are evaluated to determine if they are properly designed and operating effectively.

![Brennan, Niamh [2003] Accounting in crisis: A story of auditing, accounting, ...](https://cdn.slidesharecdn.com/ss_thumbnails/0414brennanaccountingincrisisastoryofauditingaccountingcorporategovernanceandmarketfailures-121116102706-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)