Downloaded 27 times

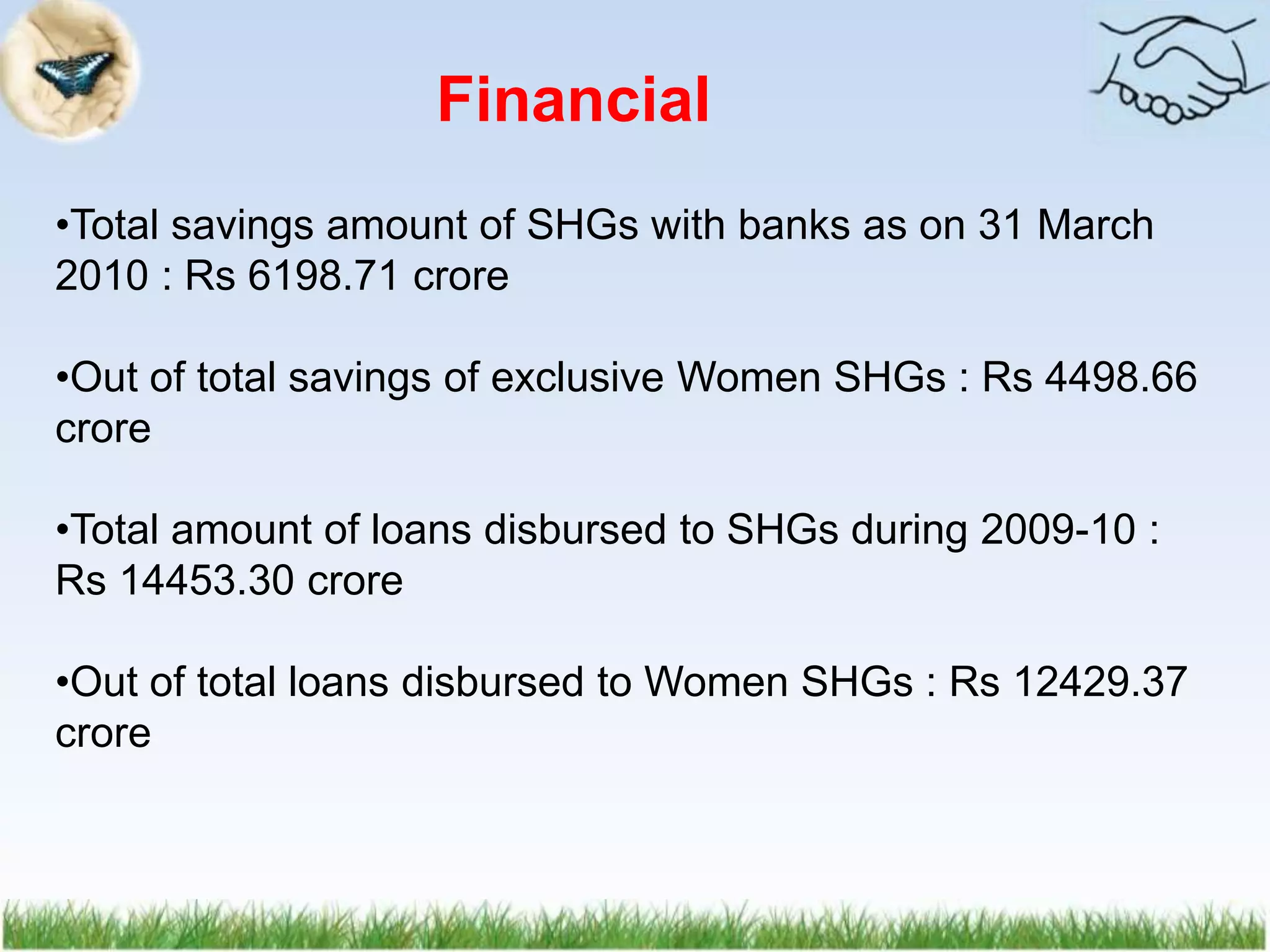

Self help groups (SHGs) play an important role in rural development by promoting savings, providing credit to members, and empowering women. SHGs are small voluntary groups that are formed to save money and provide loans to members. They help generate additional income, impart skills, and create financial inclusion in rural areas. Research studies have found that SHG membership increases members' monthly incomes, financial literacy, and decision making power. SHGs help alleviate poverty and empower rural communities through collective action.