This document provides an overview of Nigeria's roadmap to adopting International Financial Reporting Standards (IFRS) and converting from Statements of Accounting Standards (SAS) to IFRS. It discusses Nigeria's plan to adopt IFRS in 8 phases, beginning with objectives and qualitative characteristics. It also covers the conceptual framework and foundations of IFRS, benefits of IFRS adoption, and highlights of Nigeria's conversion process from SAS to IFRS. The document aims to guide Nigerian entities through understanding IFRS and transitioning reporting to align with global standards.

: ROADMAP TOIFRS ADOPTION IN

NIGERIA, CONVERSION FROM SAS

TO IFRS AND THE CONCEPTUAL

FRAMEWORK/FOUNDATION OF

IFRSs STANDARDS

Titus E. Osawe

Assistant Director, Monitoring, Enforcement and Notifications Dept.

Financial Reporting Council of Nigeria

1

2.

Content

1. BackgroundInformation on Global

Convergence

2. Conceptual Framework for Financial

Reporting

3. Nigerian Roadmap to IFRS

4. Briefs on First-Time Adoption

5. Highlights of Steps involved in Conversion

6. Over all Implications of IFRS Adoption

7. Pitfalls to avoid.

3.

BACKGROUND INFORMATION

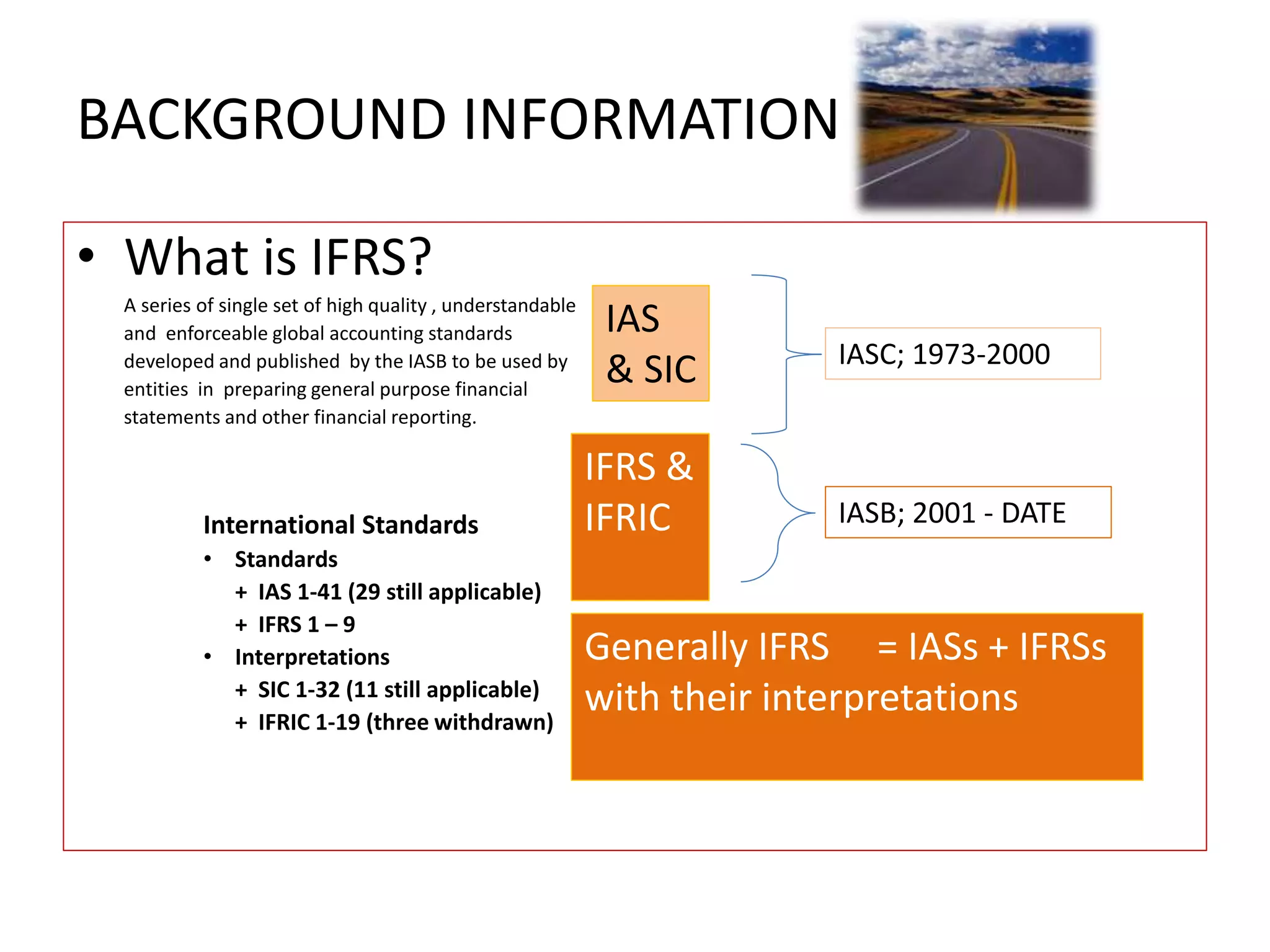

•What is IFRS?

A series of single set of high quality , understandable

and enforceable global accounting standards

developed and published by the IASB to be used by

entities in preparing general purpose financial

statements and other financial reporting.

International Standards

• Standards

+ IAS 1-41 (29 still applicable)

+ IFRS 1 – 9

• Interpretations

+ SIC 1-32 (11 still applicable)

+ IFRIC 1-19 (three withdrawn)

IAS

& SIC

IFRS &

IFRIC

IASC; 1973-2000

IASB; 2001 - DATE

Generally IFRS = IASs + IFRSs

with their interpretations

4.

A Changing GlobalFinancial

Reporting Environment

•Globally there is a remarkable movement towards a single

financial reporting language – International Financial Reporting

Standards (IFRS)

•Currently (by the end of 2011), about 150 jurisdictions permit or

require the use of IFRS

•In Africa – Ghana, South Africa, Egypt, Kenya, Morocco(Banks;p),

Namibia, Togo (p), Niger (p), Nigeria (Re: 2012)

•Regulatory trend

• International Accounting Standards Board (IASB) and the Financial Accounting

Standards Board (FASB) have reaffirmed convergence efforts

• Greater cooperation amongst regulators on IFRS application issues

4

5.

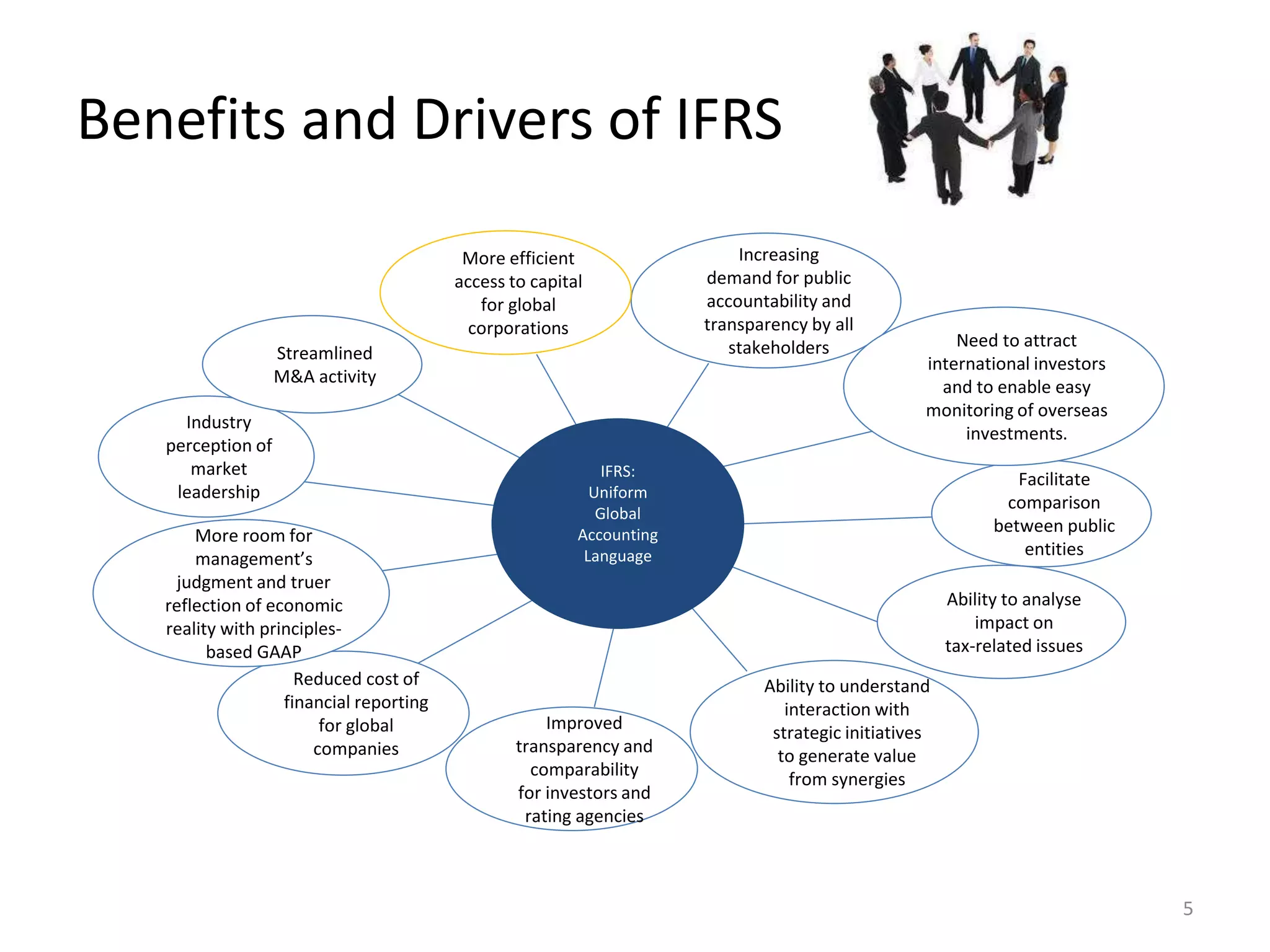

Benefits and Driversof IFRS

IFRS:

Uniform

Global

Accounting

Language

More room for

management’s

judgment and truer

reflection of economic

reality with principles-based

Reduced cost of

financial reporting

for global

companies

GAAP

Industry

perception of

market

leadership

Improved

transparency and

comparability

for investors and

rating agencies

international investors

and to enable easy

monitoring of overseas

Ability to understand

interaction with

strategic initiatives

to generate value

from synergies

Streamlined

M&A activity

Increasing

demand for public

accountability and

transparency by all

stakeholders

Need to attract

investments.

Facilitate

comparison

between public

entities

More efficient

access to capital

for global

corporations

Ability to analyse

impact on

tax-related issues

5

6.

THE IASB’S CONCEPTUALFRAMEWORK

• The conceptual framework aims at providing a sound foundation for future

accounting standards that are principles –based, internally consistent and

internationally converged.

• The Framework sets out the concepts that underlie the preparation and

presentation of financial statements for external users. Its purpose is to:

– Assist IASB in developing accounting standards and assist preparers of

financial statements in applying IFRSs and in dealing with topics that have

yet to form the subject of an IFRS

– Assist users of financial statements in interpreting the information

contained in financial statements prepared in conformity with IFRSs

– Provide those who are interested in the work of IASB with information

about its approach to the formulation of IFRSs

• The framework was first published in July 1989 and adopted in April 2001.

7.

• In July2006 IASB produced a discussion paper-preliminary

views on an improved conceptual

framework for financial reporting.

– The paper covers the first two chapters of a proposed

conceptual framework:

• Chapter 1: The objective of financial reporting

• Chapter 2: Qualitative characteristics of decision-useful financial

reporting information

• In September 2010 the IASB approved the Conceptual

Framework for Financial Reporting 2010 (the IFRS

Framework), dealing with these first two chapters.

8.

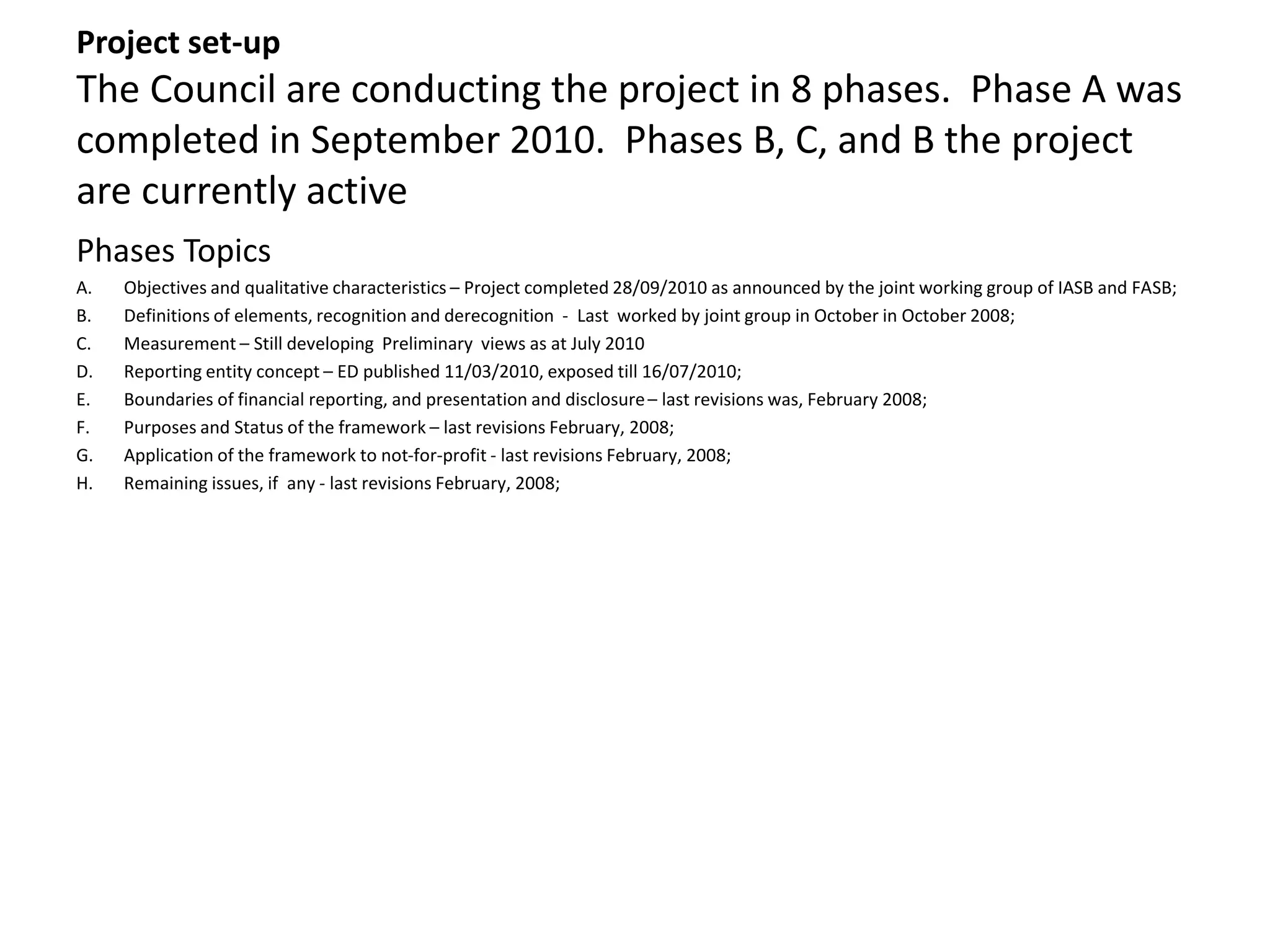

Project set-up

TheCouncil are conducting the project in 8 phases. Phase A was

completed in September 2010. Phases B, C, and B the project

are currently active

Phases Topics

A. Objectives and qualitative characteristics – Project completed 28/09/2010 as announced by the joint working group of IASB and FASB;

B. Definitions of elements, recognition and derecognition - Last worked by joint group in October in October 2008;

C. Measurement – Still developing Preliminary views as at July 2010

D. Reporting entity concept – ED published 11/03/2010, exposed till 16/07/2010;

E. Boundaries of financial reporting, and presentation and disclosure – last revisions was, February 2008;

F. Purposes and Status of the framework – last revisions February, 2008;

G. Application of the framework to not-for-profit - last revisions February, 2008;

H. Remaining issues, if any - last revisions February, 2008;

9.

• In theabsence of a Standard or an Interpretation that

applies specifically to a transaction, management must

use its judgement in developing and applying an

accounting policy that results in information that is

relevant and reliable.

– In doing this, IAS 8 (Accounting Polices, changes and

Accounting Estimates and Errorsrequires management to

consider the definitions, recognition criteria, and

measurement concepts for assets, liabilities, income, and

expenses as contained in the IFRS Framework.

10.

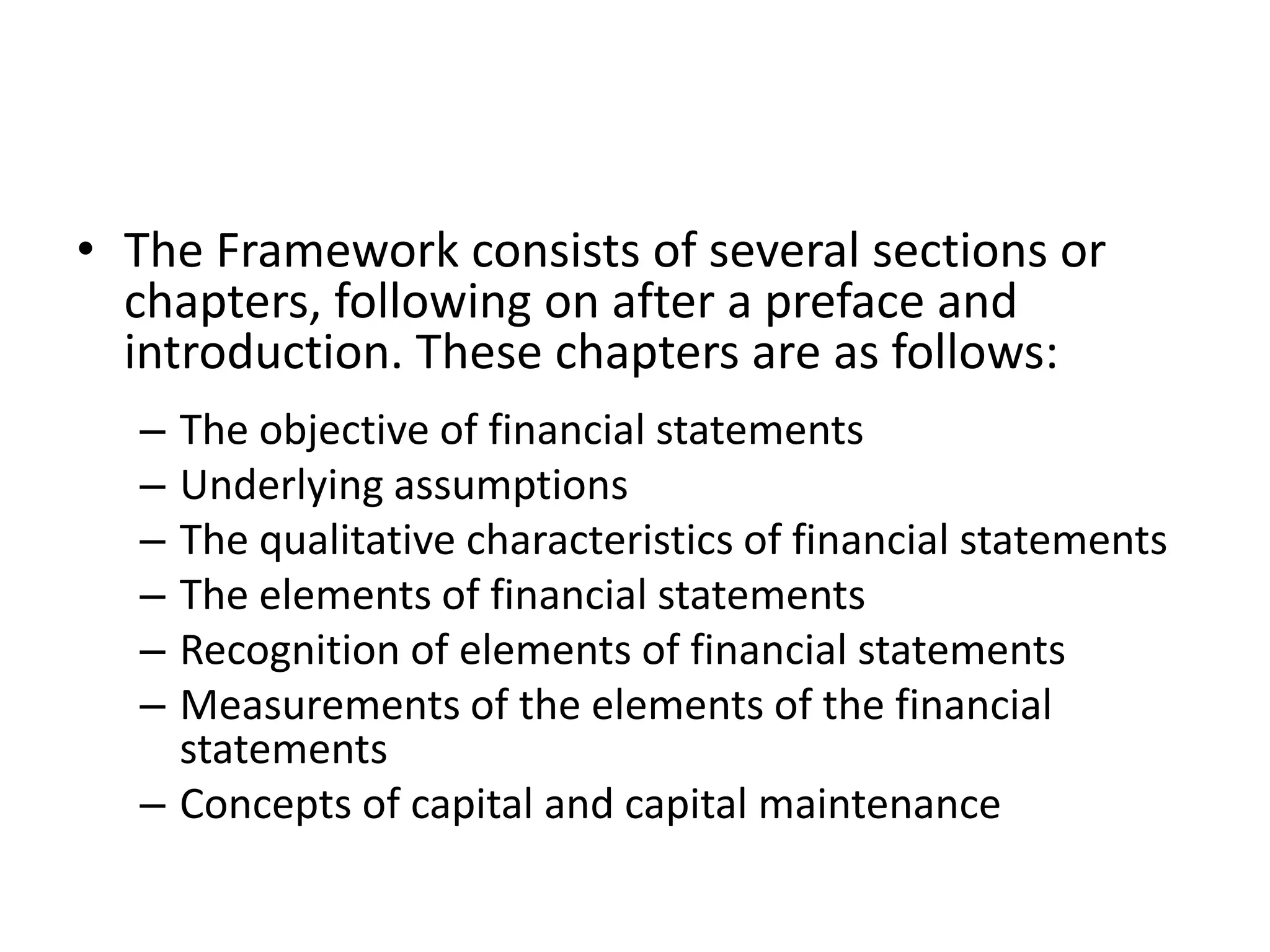

• The Frameworkconsists of several sections or

chapters, following on after a preface and

introduction. These chapters are as follows:

– The objective of financial statements

– Underlying assumptions

– The qualitative characteristics of financial statements

– The elements of financial statements

– Recognition of elements of financial statements

– Measurements of the elements of the financial

statements

– Concepts of capital and capital maintenance

11.

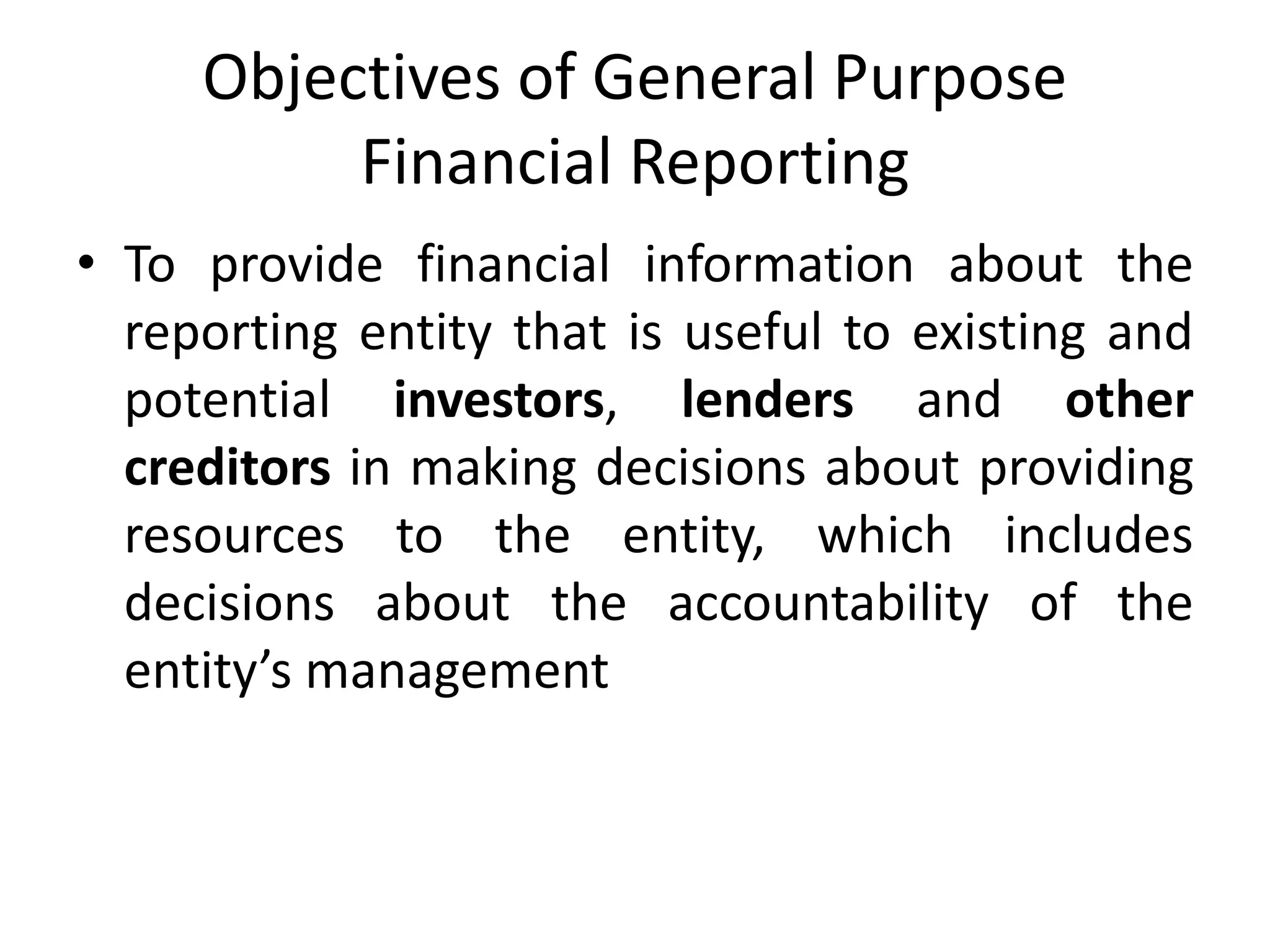

Objectives of GeneralPurpose

Financial Reporting

• To provide financial information about the

reporting entity that is useful to existing and

potential investors, lenders and other

creditors in making decisions about providing

resources to the entity, which includes

decisions about the accountability of the

entity’s management

12.

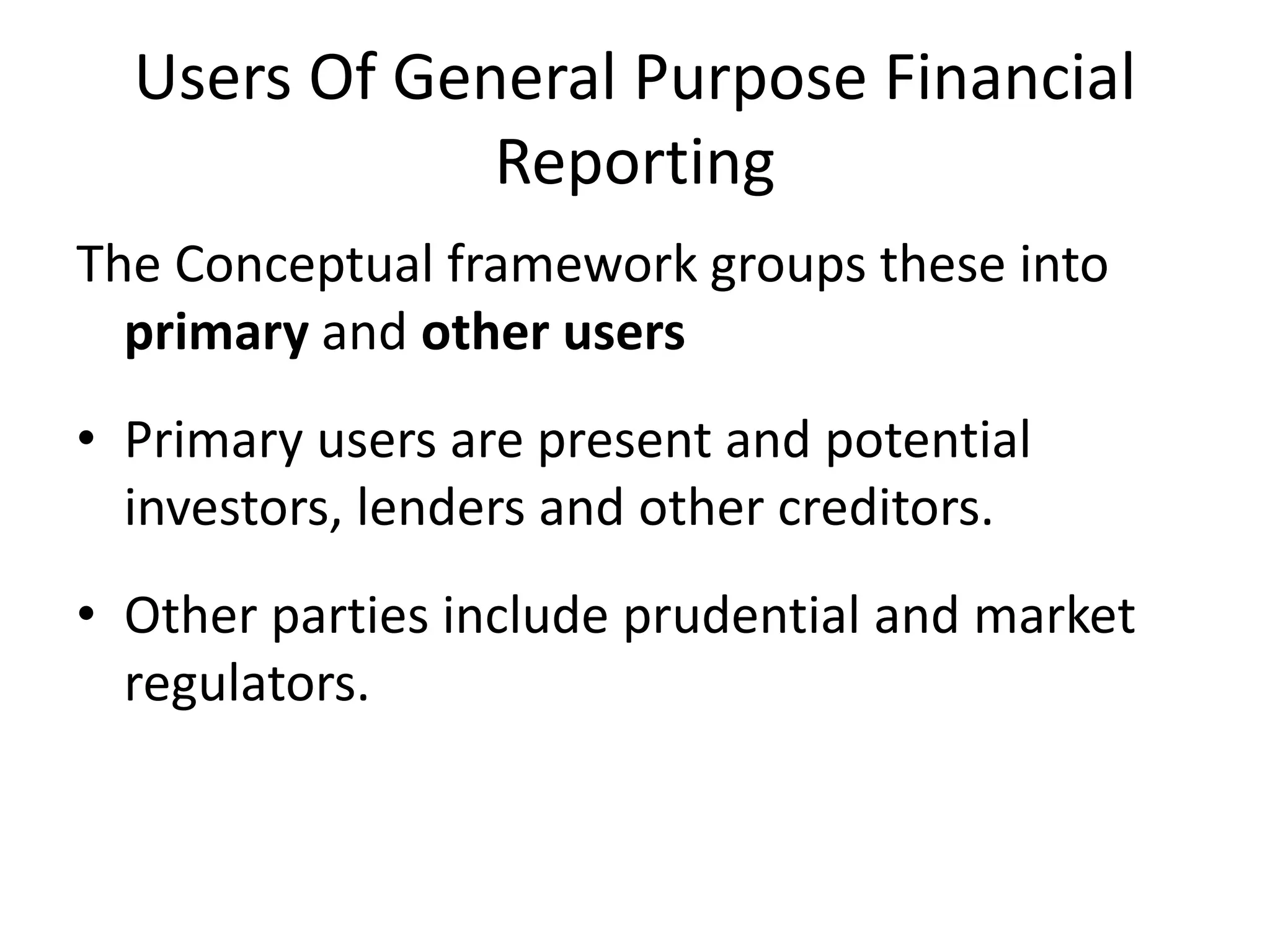

Users Of GeneralPurpose Financial

Reporting

The Conceptual framework groups these into

primary and other users

• Primary users are present and potential

investors, lenders and other creditors.

• Other parties include prudential and market

regulators.

13.

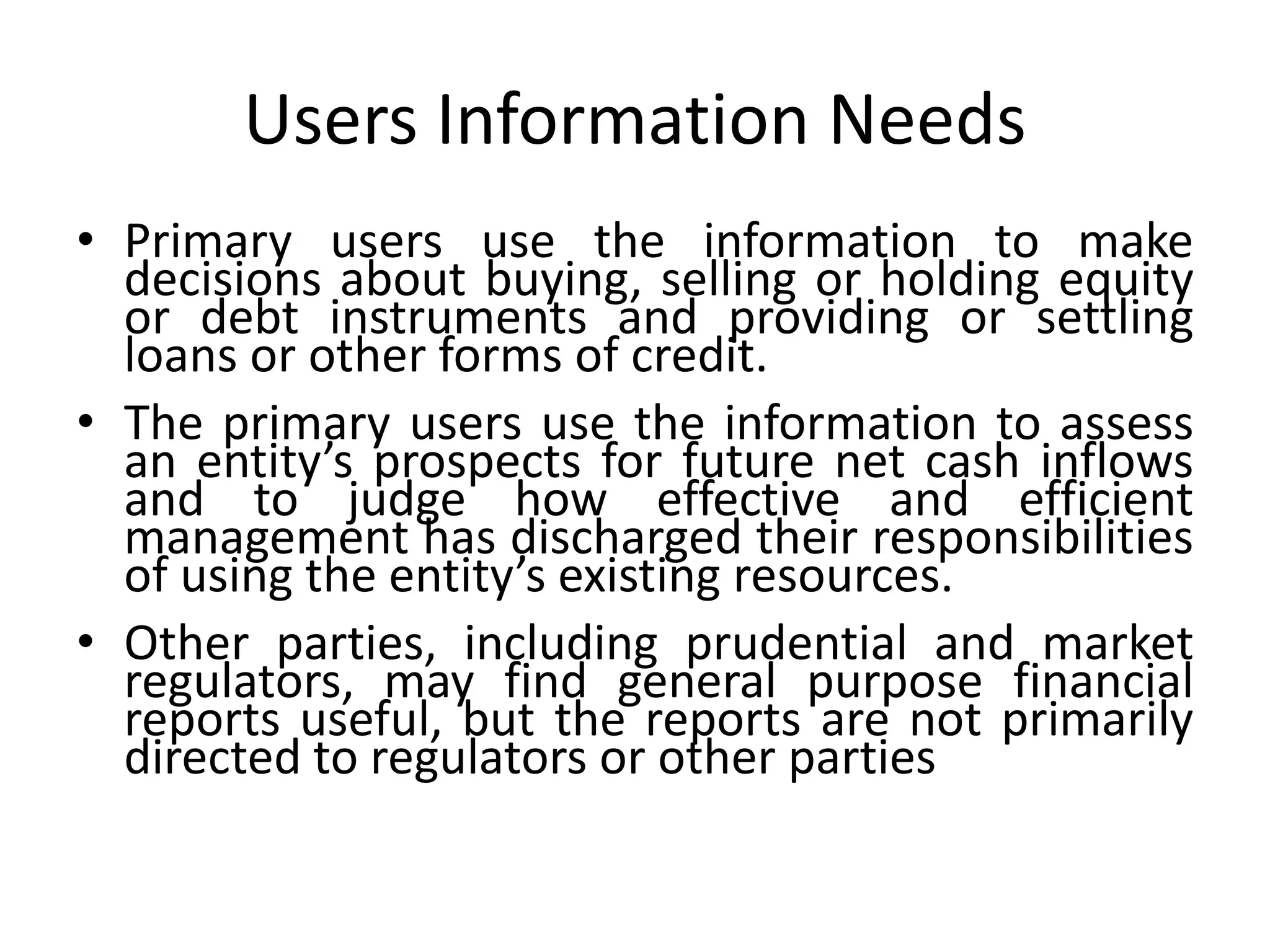

Users Information Needs

• Primary users use the information to make

decisions about buying, selling or holding equity

or debt instruments and providing or settling

loans or other forms of credit.

• The primary users use the information to assess

an entity’s prospects for future net cash inflows

and to judge how effective and efficient

management has discharged their responsibilities

of using the entity’s existing resources.

• Other parties, including prudential and market

regulators, may find general purpose financial

reports useful, but the reports are not primarily

directed to regulators or other parties

14.

Economic Resources AndClaims

• A reporting entity’s economic resources and claims are

reported in the statement of financial position

• Information about the nature and amounts assists

users to assess an entity’s

– financial strengths and weaknesses;

– liquidity and solvency, and

– its need and ability to obtain financing.

• Information about the claims and payment

requirements assists users to predict how future cash

flows will be distributed among those with a claim on

the reporting entity.

15.

Qualitative Characteristics ofFinancial

Statements

Qualitative characteristics are the attributes that

make the information provided in financial

statements useful to users. They are majorly

categorised as:

• - Fundamental qualitative characteristics-relevance

and faithful representation and

• The enhancing qualitative characteristics that

distinguish more useful information from less

useful information -comparability, timeliness,

verifiability and understandability.

16.

Relevance

• Relevantfinancial information is capable of making a

difference in the decisions made by users. Financial

information is capable of making a difference in decisions if

it has predictive value, confirmatory value, or both. The

predictive value and confirmatory value of financial

information are interrelated

• Materiality is an entity-specific aspect of relevance based

on the nature or magnitude (or both) of the items to which

the information relates in the context of an individual

entity’s financial report

• Information is material if its omission or misstatement

could influence the economic decisions of users taken on

the basis of the financial statements

17.

Faithful Representation

•General purpose financial reports represent

economic phenomena in words and numbers, To

be useful, financial information must not only be

relevant, it must also represent faithfully the

phenomena it purports to represent.

• This fundamental characteristic seeks to

maximise the underlying characteristics of

completeness, neutrality and freedom from error.

• Information must be both relevant and faithfully

represented if it is to be useful

18.

Comparability

• Informationabout a reporting entity is more

useful if it can be compared with a similar

information about other entities and with

similar information about the same entity for

another period or another date.

• Comparability enables users to identify and

understand similarities in, and differences

among, items

19.

Verifiability

• Verifiabilityhelps to assure users that

information represents faithfully the economic

phenomena it purports to represent.

• Verifiability means that different

knowledgeable and independent observers

could reach consensus, although not

necessarily complete agreement, that a

particular depiction is a faithful representation

20.

Timeliness

• Timelinessmeans that information is available

to decision-makers in time to be capable of

influencing their decisions

21.

Understandability

• Classifying,characterising and presenting information

clearly and concisely makes it understandable.

• While some phenomena are inherently complex and

cannot be made easy to understand, to exclude such

information would make financial reports incomplete

and potentially misleading.

• Financial reports are prepared for users who have a

reasonable knowledge of business and economic

activities and who review and analyse the information

with diligence

22.

Information Irrelevance AndFaithful

Representation

• Enhancing qualitative characteristics (either

individually or collectively) render information

useful if that information is irrelevant or not

represented faithfully

23.

Cost Constraint OnUseful Financial

Reporting

• Cost is a pervasive constraint on the reporting entity’s

ability to provide useful information in general purpose

financial reporting.

• Reporting such information imposes costs and those costs

should be justified by the benefits of reporting that

information.

• The IASB assesses costs and benefits in relation to financial

reporting generally, and not solely in relation to individual

reporting entities.

• The IASB will consider whether different sizes of entities

and other factors justify different reporting requirements in

certain situations.

24.

Constraints on Relevantand Reliable

Information

• Timeliness

– If there is undue delay in the reporting of information it

may lose its relevance. Management may need to balance

the relative merits of timely reporting and the provision of

reliable information

• Balance between benefit and cost

– The benefits derived from information should exceed the

cost of providing it

• Balance between qualitative characteristics

– In practice a balancing, or trade-off, between qualitative

characteristics is often necessary. Generally the aim is to

achieve an appropriate balance among the characteristics

in order to meet the objective of financial statements

25.

The Reporting Entity-This is currently

a discussion paper.

• The conceptual framework describes rather than

precisely define a reporting entity as a

circumscribed area of business activity of interest

to present and potential equity investors, lenders

and other capital providers.

– Examples of reporting entities are:

• Sole trader

• Corporation

• Trust

• Partnership

• Associations, and

• Group

26.

The Parent EntityFinancial Reporting

• Two issues considered here are:

– The parent company approach to consolidated financial

statements.

– Whether parent only financial statements and consolidated

financial statements meet the objective of financial reporting

and whether both are needed.

• IASB preliminary conclusion is:

– That consolidated financial statements should be presented

from the perspective of group reporting entity not, the parent

company shareholders

– That the consolidated financial statements meet the objective

of financial reporting, but that parent only financial statements

maybe presented provided they are included in the same

financial report as consolidated financial statements.

27.

Underlying Assumptions

•Accrual basis

– In order to meet their objectives, financial statements are

prepared on the accrual basis of accounting

• Going concern

– The financial statements are normally prepared on the

assumption that an entity is a going concern and will continue in

operation for the foreseeable future

28.

Elements of FinancialStatements

• Financial statements portray the financial effects of transactions

and other events by grouping them into broad classes according to

their economic characteristics

• These broad classes are termed the elements of financial

statements

• Elements directly related to the measurement of financial position

in the balance sheet are assets, liabilities and equity

• The elements directly related to the measurement of performance

in the income statement are income and expenses

• The statement of changes in financial position usually reflects

income statement elements and changes in balance sheet elements

29.

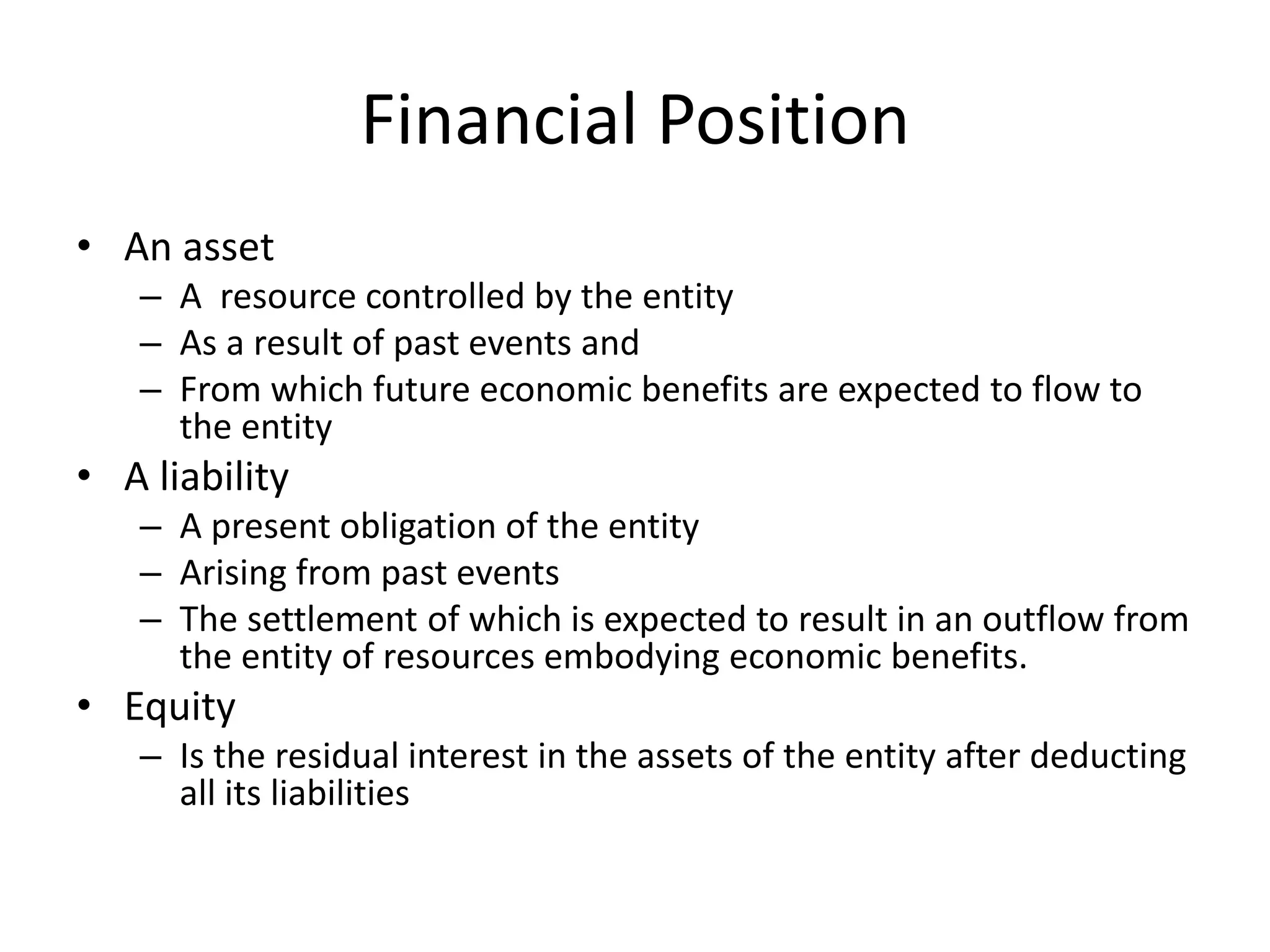

Financial Position

•An asset

– A resource controlled by the entity

– As a result of past events and

– From which future economic benefits are expected to flow to

the entity

• A liability

– A present obligation of the entity

– Arising from past events

– The settlement of which is expected to result in an outflow from

the entity of resources embodying economic benefits.

• Equity

– Is the residual interest in the assets of the entity after deducting

all its liabilities

30.

Performance

• Profitis frequently used as a measure of

performance or as the basis for other measures,

such as return on investment or earnings per

share.

• The elements directly related to the

measurement of profit are income and expenses.

The recognition and measurement of income and

expenses, and hence profit, depends in part on:

– The concepts of capital

– Capital maintenance used by the entity

31.

Income and Expenses

Income

• Increases in economic benefits during the accounting

period in the form of inflows or enhancements of assets or

decreases of liabilities that result in increases in equity,

other than those relating to contributions from equity

participants

Expenses

• Decreases in economic benefits during the accounting

period in the form of outflows or depletions of assets or

incurrences of liabilities that result in decreases in equity,

other than those relating to distributions to equity

participants.

32.

Capital Maintenance Adjustments

• The revaluation or restatement of assets and

liabilities gives rise to increases or decreases in

equity

• While these increases or decreases meet the

definition of income and expenses, they are not

included in the income statement under certain

concepts of capital maintenance

• Instead these items are included in equity as

capital maintenance adjustments or revaluation

reserves.

33.

Recognition Of TheElements Of

Financial Statements

• Recognition is the process of incorporating in the

financial statements

– An item that meets the definition of an element; and

– Satisfies the criteria for recognition

• An item that meets the definition of an element

should be recognised if:

– It is probable that any future economic benefit

associated with the item will flow to or from the

entity

– The item has a cost or value that can be measured

with reliability.

34.

Measurement of theElements of

Financial Statements

• Measurement is the process of determining the

monetary amounts at which the elements of the

financial statements are to be recognised and

carried in the balance sheet and income

statement

• Bases of measurement include:

– Historical cost

– Current cost

– Realisable (settlement) value

– Present value

35.

NIGERIAN ROADMAP TOIFRS ADOPTION

Adoption of IFRS in Nigeria:

a trip down memory lane

• What is SAS?

Just like the IASB’s pronouncements (developing & publishing) of IFRS the NASB (now FRC) issues

prescribeds and pronounce accounting rules to be used by entities in preparing general purpose

financial statements, to ensure transparency and compatibility.

• 32 SASs developed and published so far

• 7 Industry Specific Standards

• 1 SORP- Statement of Recommended Practice on Employees’

Retirement and Termination Benefits for Public Sector Entities

• In the earlier years, NASB’s SAS had many similarities

with IASB’s standards. (but the SASs never matched the

pace of the IASs in terms of review and updates)

35

36.

Adoption of IFRSin Nigeria:

a trip down memory lane

• Adaptation was reiterated in Nigeria between

2002 – mid 2008.

• Closer harmonisation of SAS with IFRS took place

in 2007 with the release of SASs 25, 27, 28, 29, 30.

• Strong signals from CBN, SEC, NSE and other

regulators suggesting adoption of IFRS.

37.

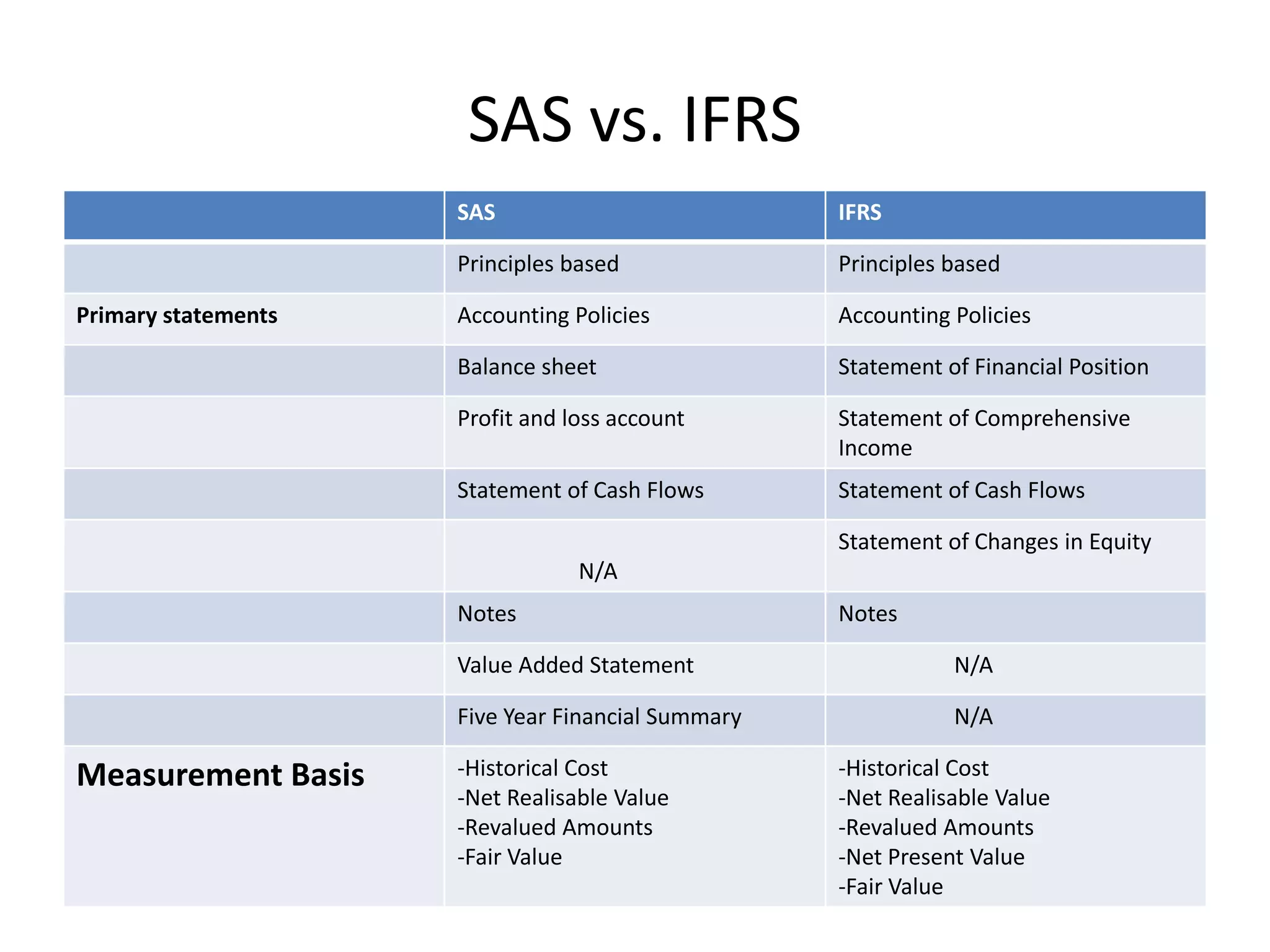

SAS vs. IFRS

SAS IFRS

Principles based Principles based

Primary statements Accounting Policies Accounting Policies

Balance sheet Statement of Financial Position

Profit and loss account Statement of Comprehensive

Income

Statement of Cash Flows Statement of Cash Flows

N/A

Statement of Changes in Equity

Notes Notes

Value Added Statement N/A

Five Year Financial Summary N/A

Measurement Basis -Historical Cost

-Net Realisable Value

-Revalued Amounts

-Fair Value

-Historical Cost

-Net Realisable Value

-Revalued Amounts

-Net Present Value

-Fair Value

38.

Adoption of IFRSin Nigeria

• A Road map committee was inaugurated on

October 22, 2009.

• The Road Map committee’s report was

submitted January 26, 2010.

• The Federal Government took a decision on

July 28, 2010 to adopt IFRS effective January 1,

2012 .

38

39.

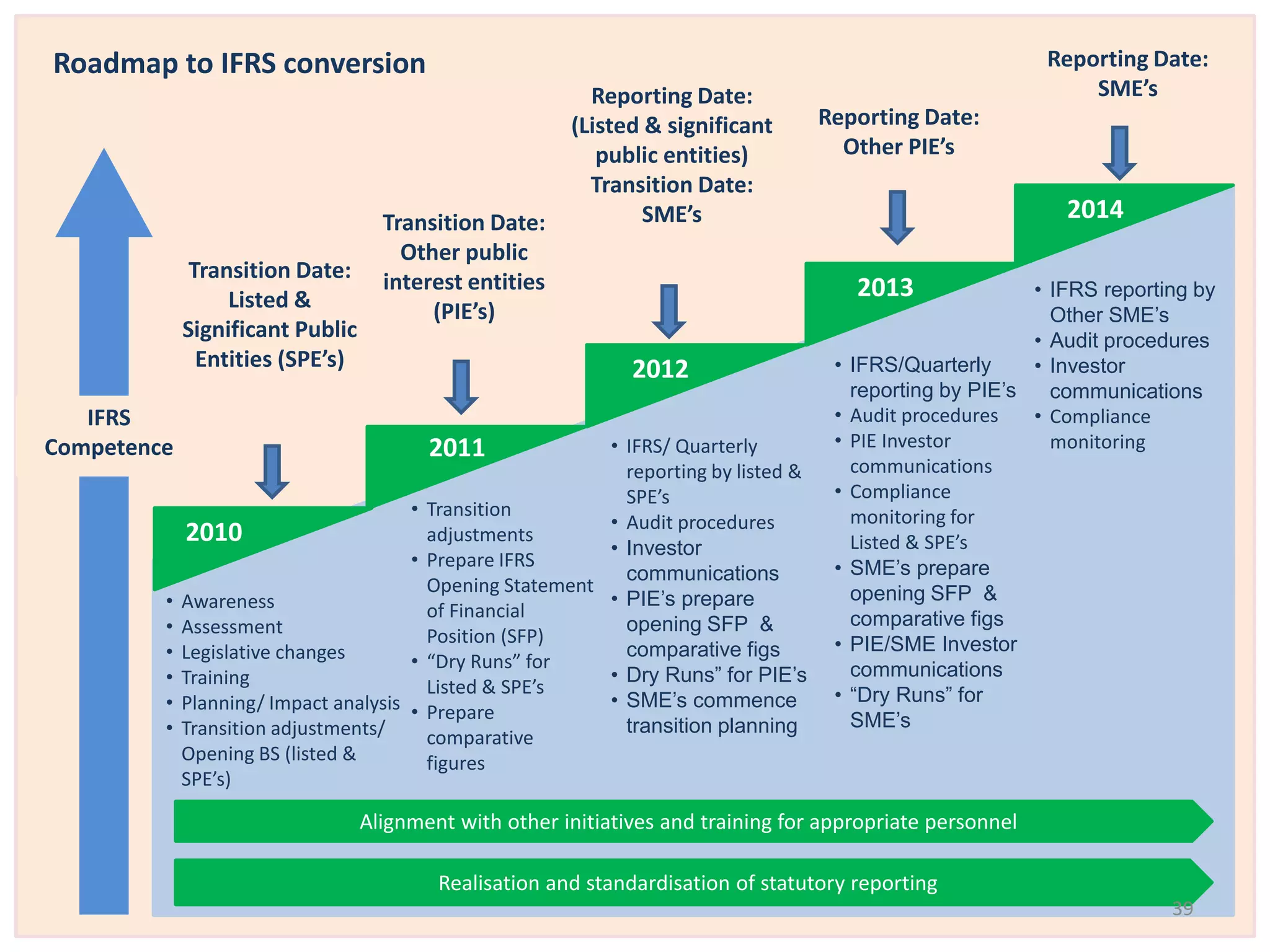

IFRS

Competence

2010

Transition Date:

Other public

interest entities

(PIE’s)

2011

2012

Reporting Date:

Other PIE’s

2013

Alignment with other initiatives and training for appropriate personnel

Realisation and standardisation of statutory reporting

• Awareness

• Assessment

• Legislative changes

• Training

• Planning/ Impact analysis

• Transition adjustments/

Opening BS (listed &

SPE’s)

• Transition

adjustments

• Prepare IFRS

Opening Statement

of Financial

Position (SFP)

• “Dry Runs” for

Listed & SPE’s

• Prepare

comparative

figures

• IFRS/ Quarterly

reporting by listed &

SPE’s

• Audit procedures

• Investor

communications

• PIE’s prepare

opening SFP &

comparative figs

• Dry Runs” for PIE’s

• SME’s commence

transition planning

• IFRS/Quarterly

reporting by PIE’s

• Audit procedures

• PIE Investor

communications

• Compliance

monitoring for

Listed & SPE’s

• SME’s prepare

opening SFP &

comparative figs

• PIE/SME Investor

communications

• “Dry Runs” for

SME’s

Roadmap to IFRS conversion

Transition Date:

Listed &

Significant Public

Entities (SPE’s)

Reporting Date:

(Listed & significant

public entities)

Transition Date:

Reporting Date:

SME’s

SME’s 2014

• IFRS reporting by

Other SME’s

• Audit procedures

• Investor

communications

• Compliance

monitoring

39

40.

Significant public interestentities

• This means

• government business entities,

• all entities that have their equities or debt instruments

listed and traded in a public market i.e.

• a domestic or foreign Stock Exchange or

• an Over the Counter market, including local and regional markets

• such other organisations, though unquoted, are required

by law to file returns with

• regulatory authorities and this excludes private companies that

routinely file returns only with Corporate Affairs Commission and

the Federal Inland Revenue Service. Examples of entities meeting

these criteria include financial and other credit institutions and

insurance companies.

40

41.

Other Public InterestEntities

• This refers to those entities, other than listed

entities (unquoted, private companies)

– which are of significant public interest because

• of their nature of business,

• size

• number of employees

• their corporate status which require wide range of

stakeholders.

– Examples of entities meeting these criteria are

• large not for profit entities such as charities and pension

funds and may include publicly owned entities

• other entities where there is a potentially significant effect

on financial stability.

41

42.

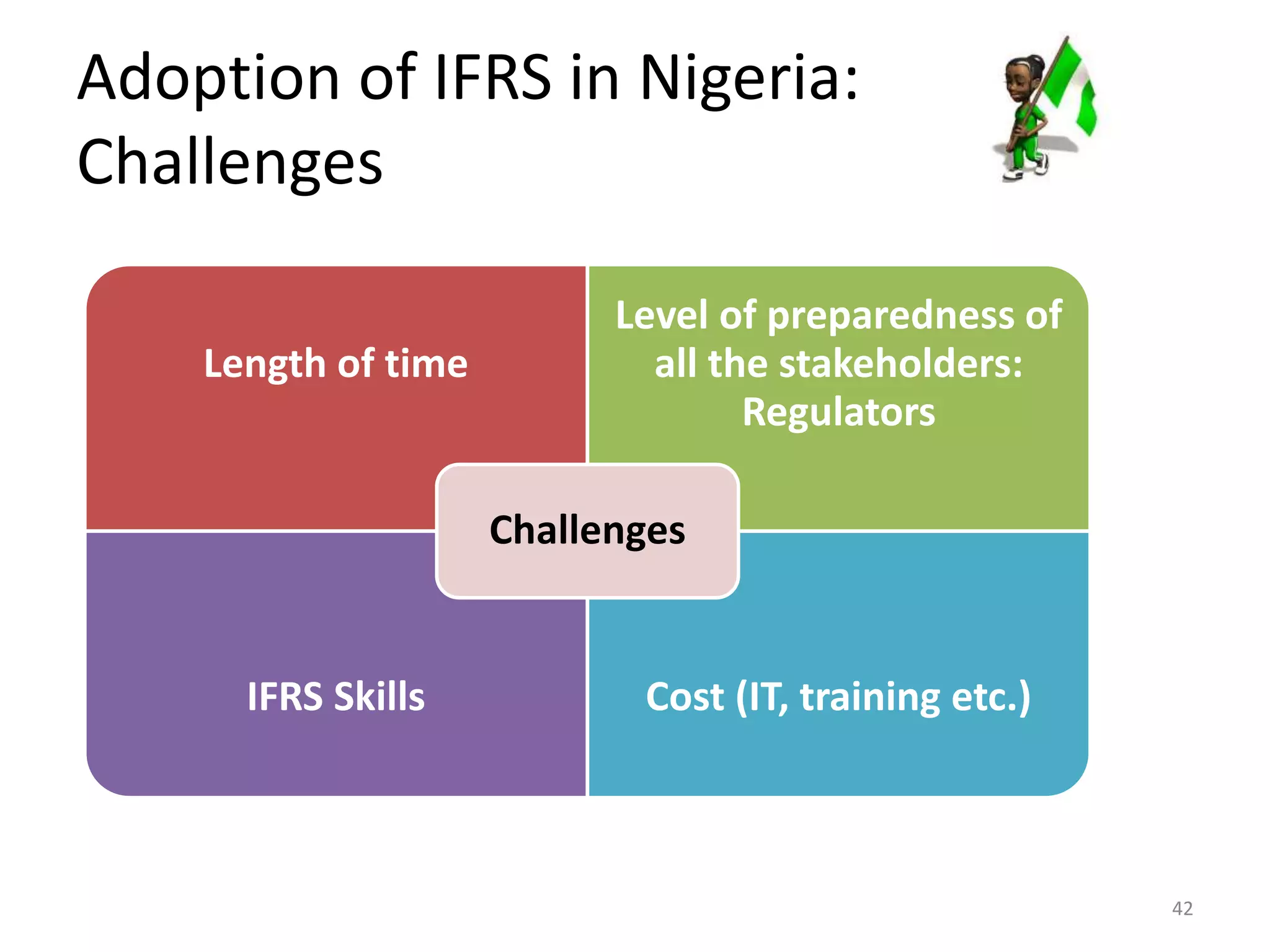

Adoption of IFRSin Nigeria:

Challenges

Length of time

Level of preparedness of

all the stakeholders:

Regulators

Challenges

IFRS Skills Cost (IT, training etc.)

42

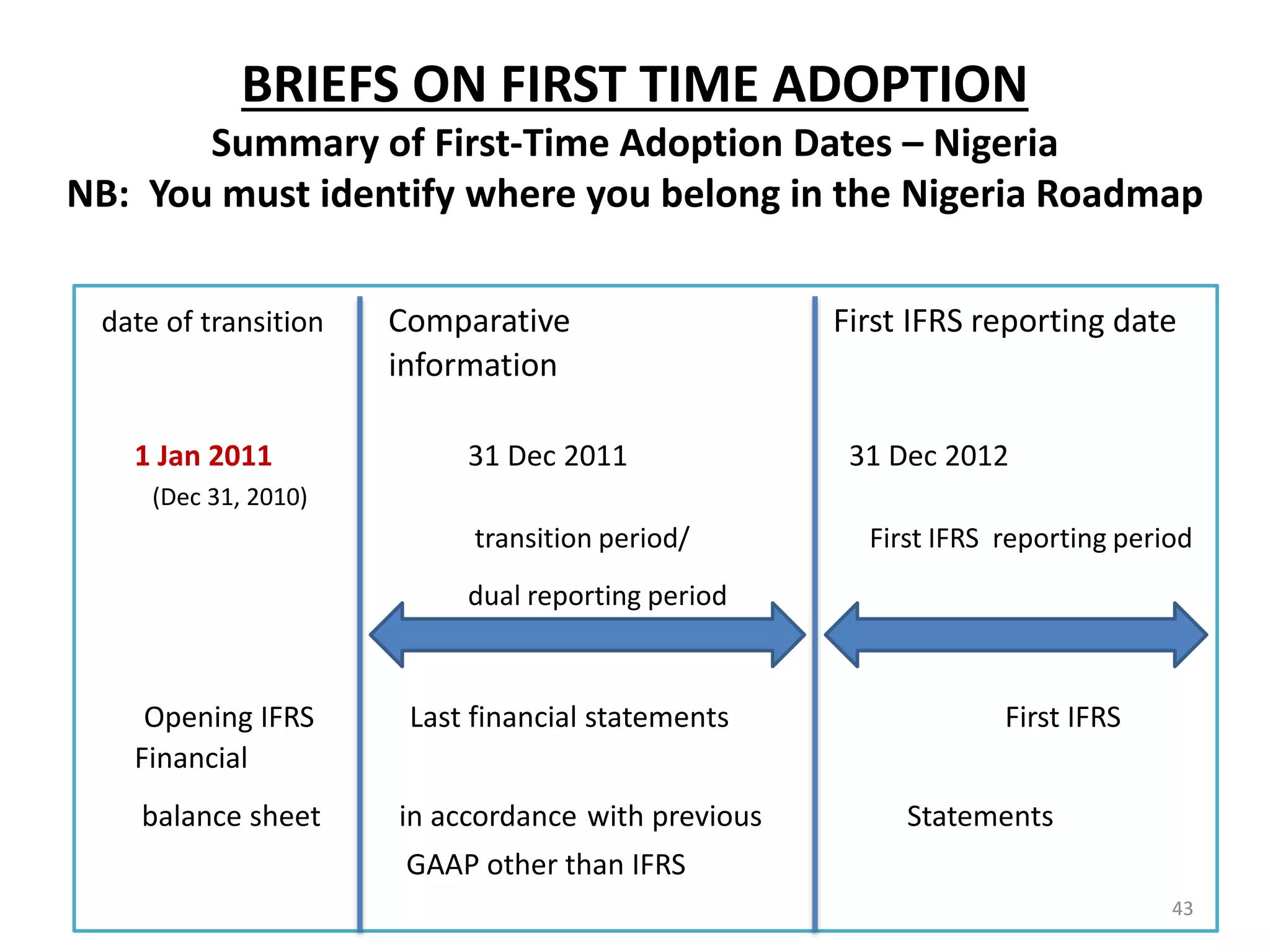

43.

BRIEFS ON FIRSTTIME ADOPTION

Summary of First-Time Adoption Dates – Nigeria

NB: You must identify where you belong in the Nigeria Roadmap

date of transition Comparative First IFRS reporting date

information

1 Jan 2011 31 Dec 2011 31 Dec 2012

(Dec 31, 2010)

transition period/ First IFRS reporting period

dual reporting period

Opening IFRS Last financial statements First IFRS

Financial

balance sheet in accordance with previous Statements

GAAP other than IFRS

43

44.

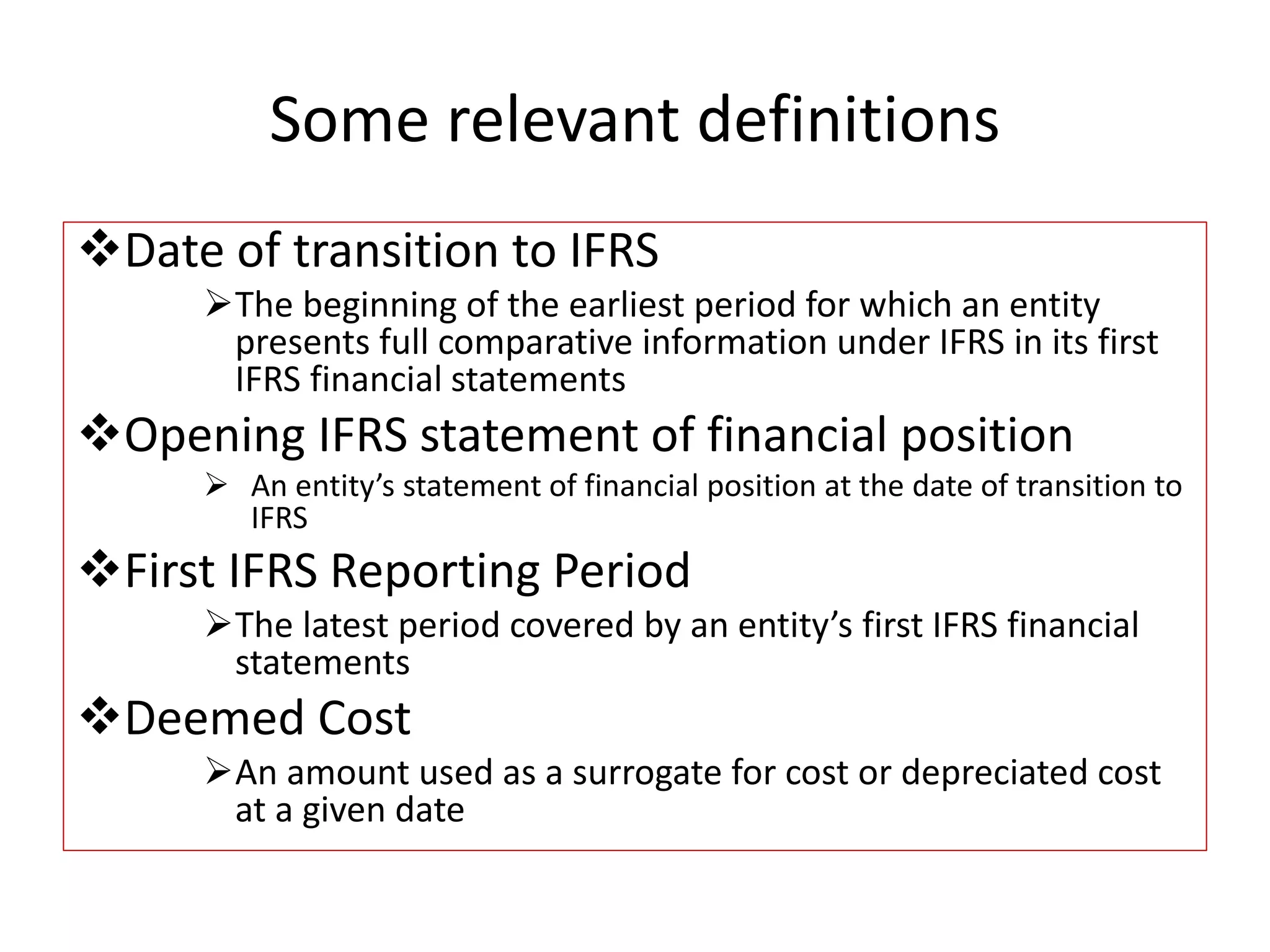

Some relevant definitions

Date of transition to IFRS

The beginning of the earliest period for which an entity

presents full comparative information under IFRS in its first

IFRS financial statements

Opening IFRS statement of financial position

An entity’s statement of financial position at the date of transition to

IFRS

First IFRS Reporting Period

The latest period covered by an entity’s first IFRS financial

statements

Deemed Cost

An amount used as a surrogate for cost or depreciated cost

at a given date

45.

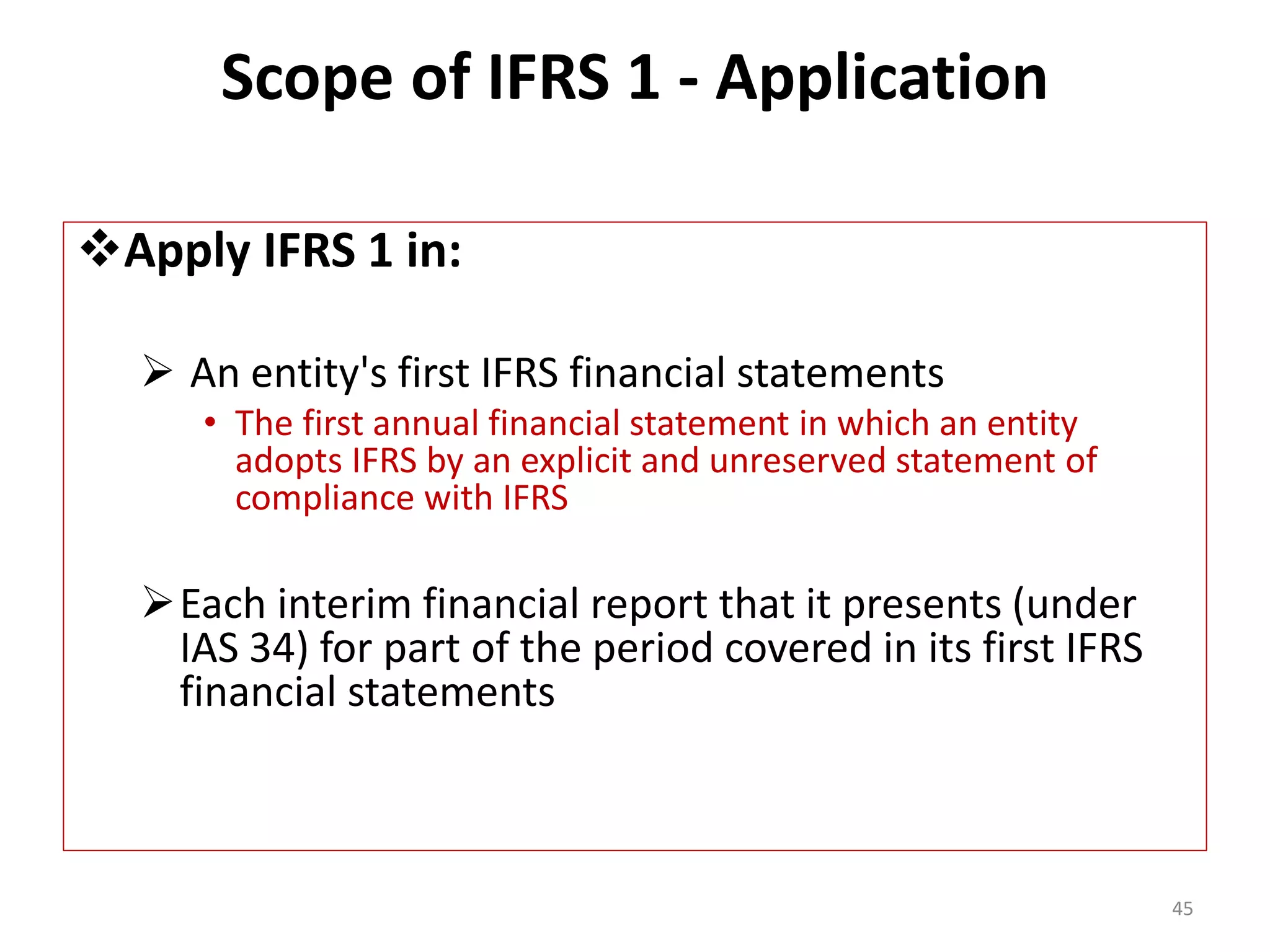

Scope of IFRS1 - Application

Apply IFRS 1 in:

An entity's first IFRS financial statements

• The first annual financial statement in which an entity

adopts IFRS by an explicit and unreserved statement of

compliance with IFRS

Each interim financial report that it presents (under

IAS 34) for part of the period covered in its first IFRS

financial statements

45

46.

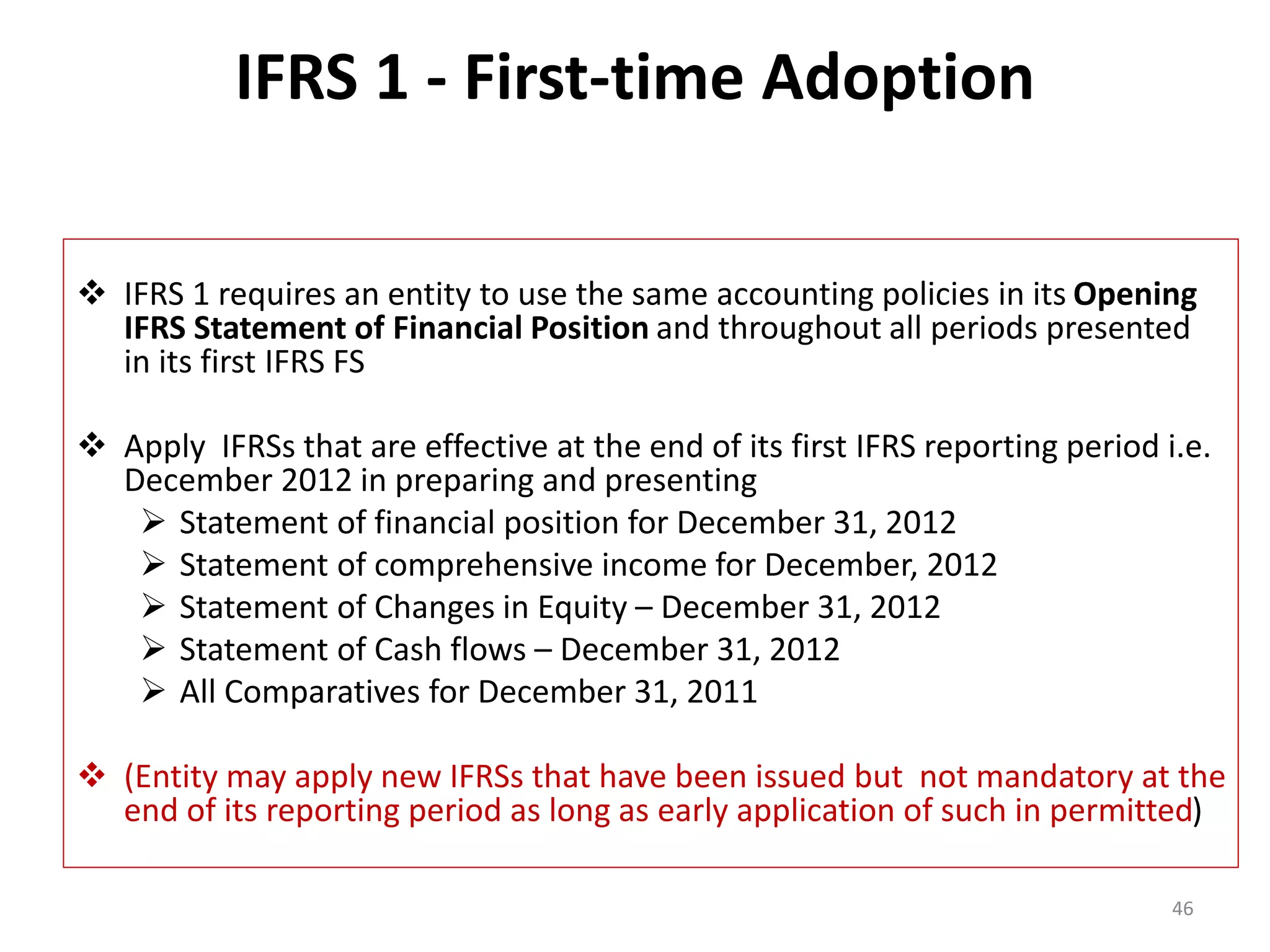

IFRS 1 -First-time Adoption

IFRS 1 requires an entity to use the same accounting policies in its Opening

IFRS Statement of Financial Position and throughout all periods presented

in its first IFRS FS

Apply IFRSs that are effective at the end of its first IFRS reporting period i.e.

December 2012 in preparing and presenting

Statement of financial position for December 31, 2012

Statement of comprehensive income for December, 2012

Statement of Changes in Equity – December 31, 2012

Statement of Cash flows – December 31, 2012

All Comparatives for December 31, 2011

(Entity may apply new IFRSs that have been issued but not mandatory at the

end of its reporting period as long as early application of such in permitted)

46

47.

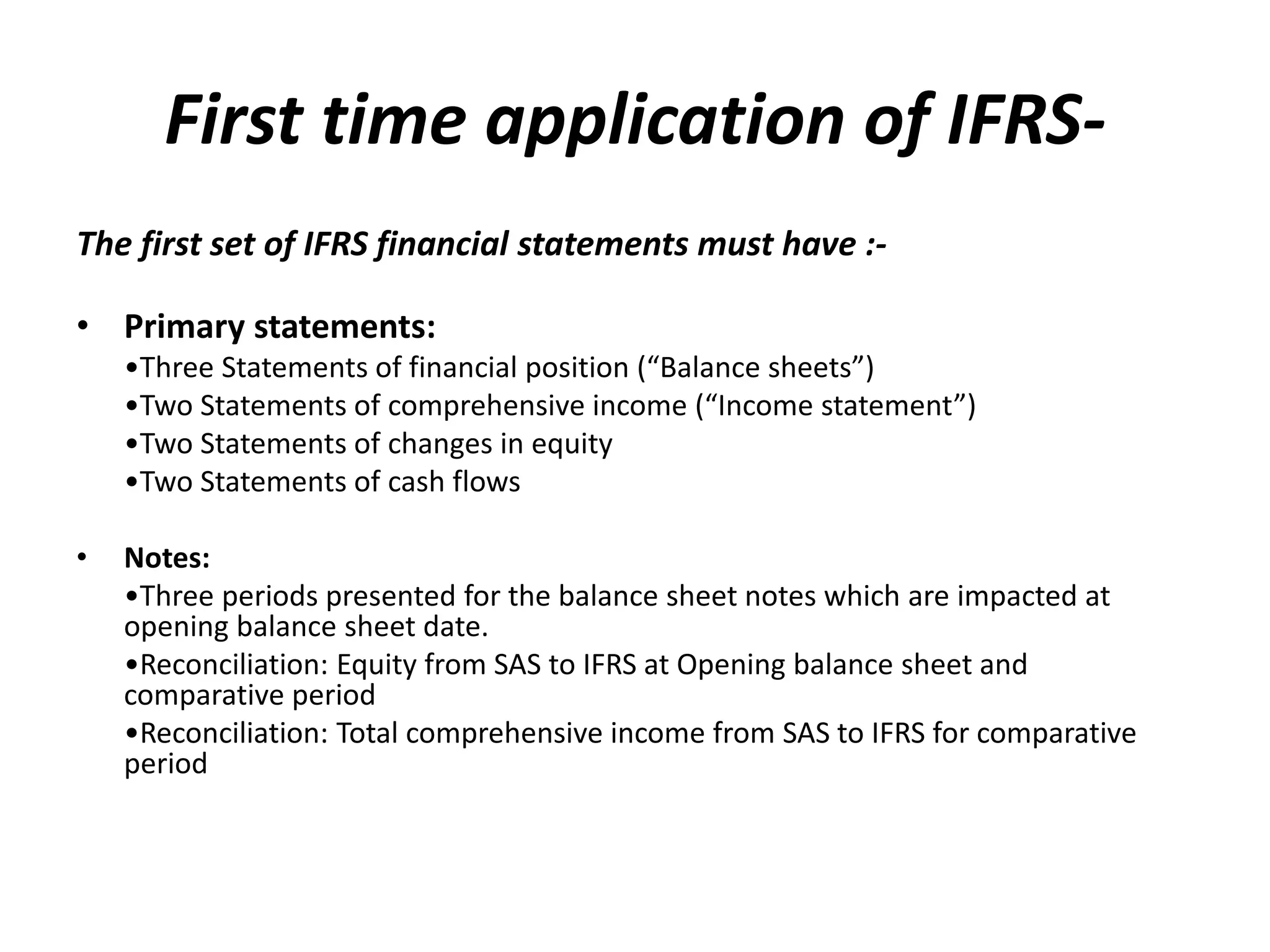

First time applicationof IFRS-The

first set of IFRS financial statements must have :-

• Primary statements:

•Three Statements of financial position (“Balance sheets”)

•Two Statements of comprehensive income (“Income statement”)

•Two Statements of changes in equity

•Two Statements of cash flows

• Notes:

•Three periods presented for the balance sheet notes which are impacted at

opening balance sheet date.

•Reconciliation: Equity from SAS to IFRS at Opening balance sheet and

comparative period

•Reconciliation: Total comprehensive income from SAS to IFRS for comparative

period

48.

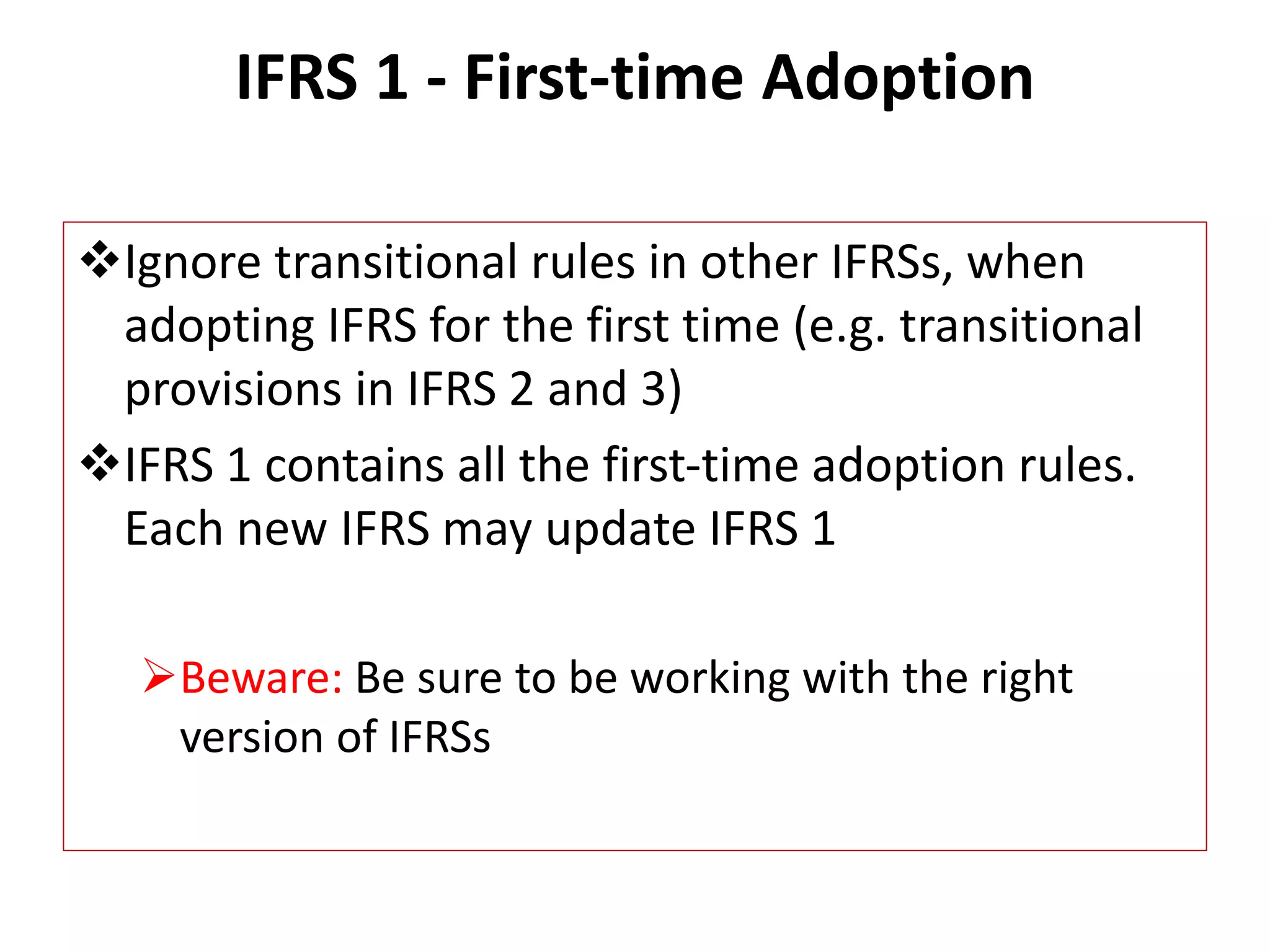

IFRS 1 -First-time Adoption

Ignore transitional rules in other IFRSs, when

adopting IFRS for the first time (e.g. transitional

provisions in IFRS 2 and 3)

IFRS 1 contains all the first-time adoption rules.

Each new IFRS may update IFRS 1

Beware: Be sure to be working with the right

version of IFRSs

49.

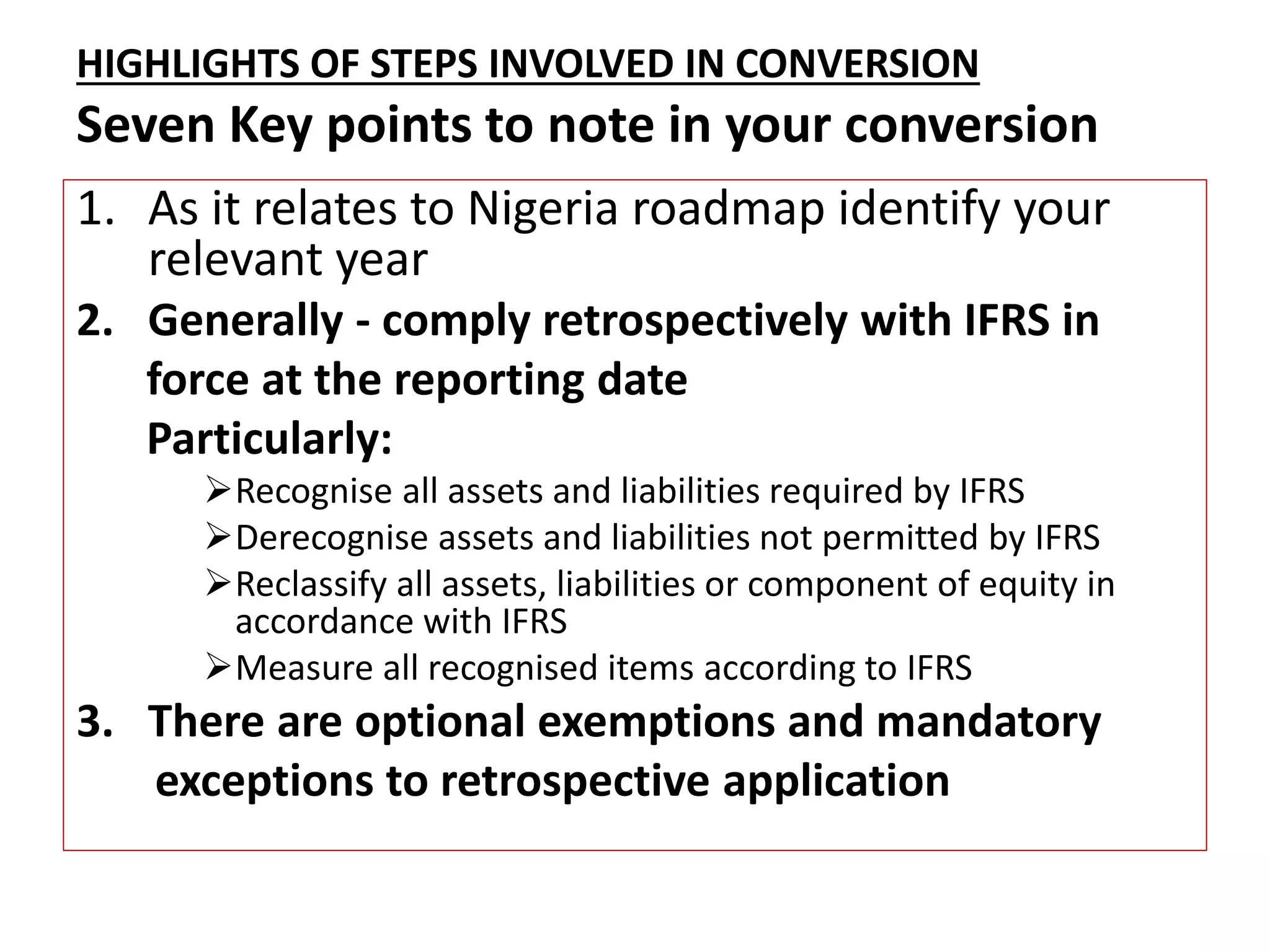

HIGHLIGHTS OF STEPSINVOLVED IN CONVERSION

Seven Key points to note in your conversion

1. As it relates to Nigeria roadmap identify your

relevant year

2. Generally - comply retrospectively with IFRS in

force at the reporting date

Particularly:

Recognise all assets and liabilities required by IFRS

Derecognise assets and liabilities not permitted by IFRS

Reclassify all assets, liabilities or component of equity in

accordance with IFRS

Measure all recognised items according to IFRS

3. There are optional exemptions and mandatory

exceptions to retrospective application

OVERALL IMPLICATIONS

Implicationon Financial reporting

• New Assets coming onto the balance sheet

• Potential for greater volatility from increased use of

fair value

• Increased use of management judgment

• Transition elections and exemptions - potential

impact on retained earnings

• Significant increase in disclosures

• Improved annual reports and accounts in terms of

quality and quantity

51

52.

Implication on financialreporting (contd.)

• Transparent and comparable data

• Implications for debt covenants and other

legal requirements

• Additional valuation costs

• The entity’s business process (all aspect of the

organisation). Complete change of system,

process and people.

52

53.

PITFALLS TO AVOID

Don’t think it’s not an enterprise-wide issue.

53

• Poor stakeholder management

• Last minute implementation from poor planning

• Late engagement of business units

– where data is captured; or

– where customers are impacted

• Not embedding accounting solutions into underlying systems

• Internal reporting backing into legacy GAAP

• Slow to move on developing and retaining resources

• Push down of centralized accounting decisions without appropriate

consultation

• Underestimation of data required and support processes to get them