1) The document presents on responsibility accounting, which assigns responsibility for controlling costs to individuals in an organization.

2) Responsibility accounting divides an organization into responsibility centers like divisions, departments, and product lines. Managers of these centers are responsible for achieving goals and tasks are assigned to employees.

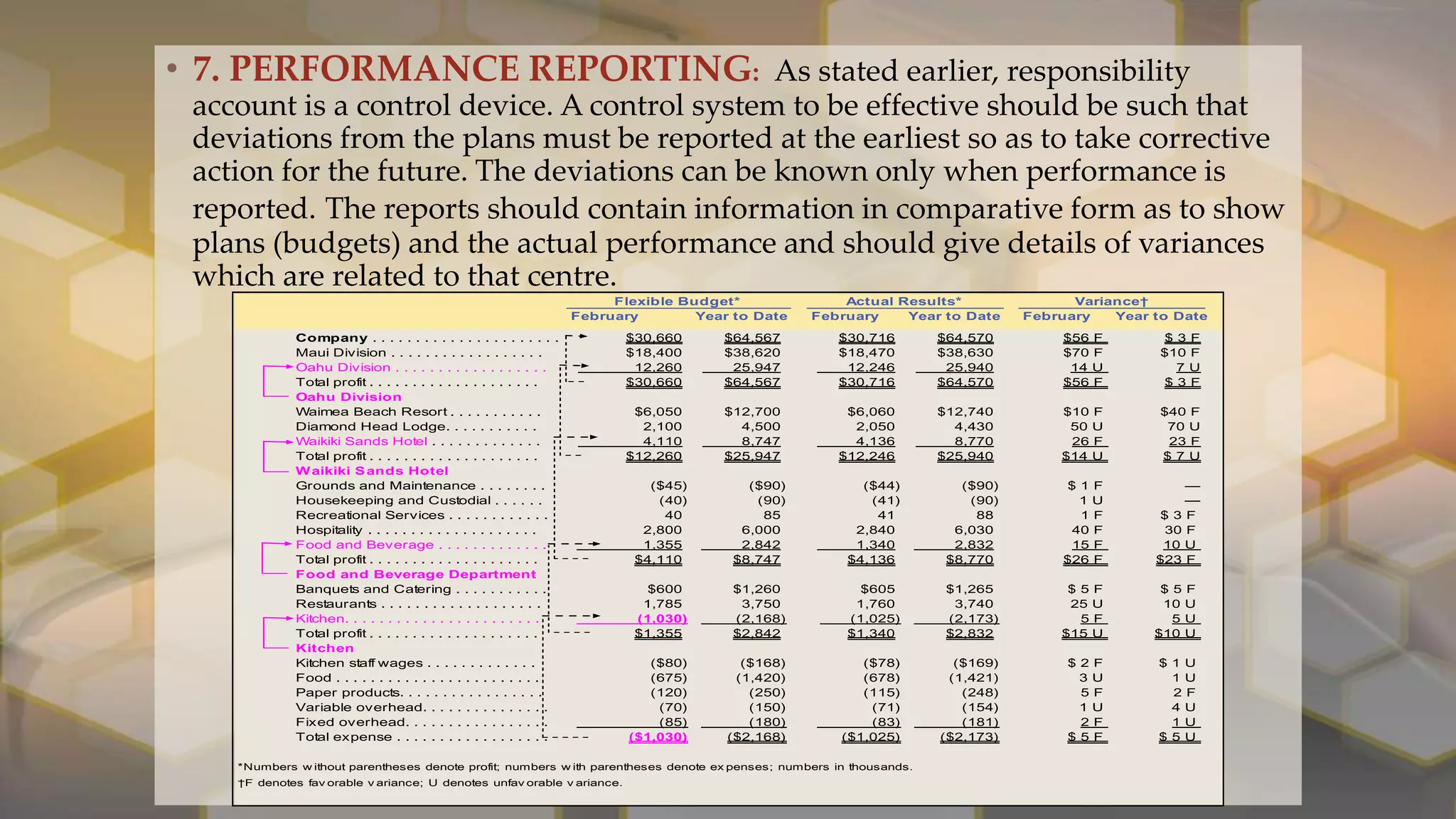

3) Key features of responsibility accounting include using budgets, identifying responsibility centers like cost, profit, and investment centers, and reporting performance and variances from budgets.

![Cost and management accounting I_Ch._1[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/costich-240403083325-418be587-thumbnail.jpg?width=640&height=640&fit=bounds)