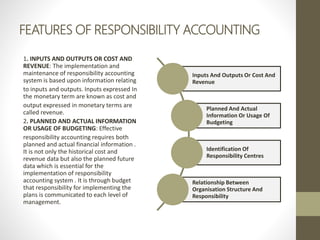

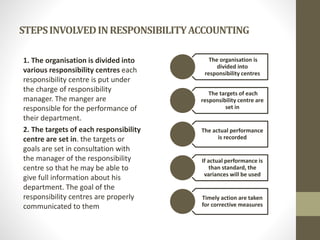

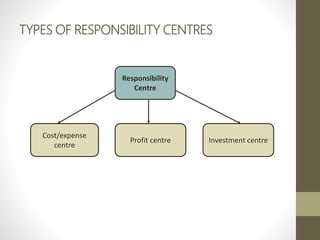

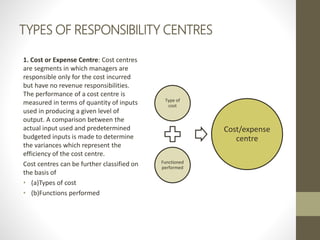

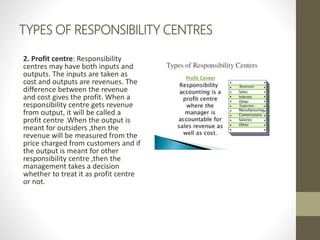

Responsibility accounting involves dividing an organization into responsibility centers and assigning costs and revenues to each center. The key types of responsibility centers are cost centers, which managers are responsible for costs, profit centers where managers are responsible for both costs and revenues, and investment centers where managers are responsible for costs, revenues, and capital employed. Effective responsibility accounting requires setting targets for each center, tracking actual performance against targets, reporting variances to management, and taking corrective actions. It aims to evaluate performance and provide feedback to improve future operations.