Downloaded 52 times

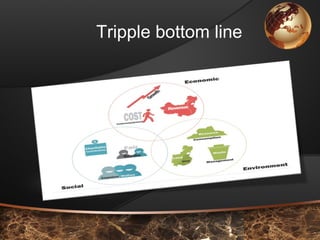

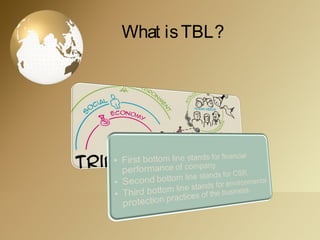

Recent trends in corporate reporting covers many topics including intangible assets reporting, triple bottom line reporting, human resource accounting, forensic accounting, and corporate social responsibility. The key topics discussed are: - Intangible assets now constitute 75-90% of company value so accurate reporting is important under IFRS standards. - Triple bottom line reporting requires companies to report on their environmental and social impacts, not just financial performance, to promote sustainability. - Human resource accounting aims to identify and measure human capital to provide feedback to managers and support employee morale and loyalty. - Forensic accounting integrates accounting, auditing, and investigation skills for dispute resolution in courts or to detect internal issues not found through