The document discusses process costing systems used in manufacturing. Process costing is used for continuous production of similar goods and involves accumulating costs by department. Key points include:

1. Costs are accumulated by department and a unit cost is calculated for each department by dividing total costs by units produced.

2. Costs and units are transferred between departments until reaching finished goods.

3. Inventory of work in process is tracked and assigned costs for incomplete units.

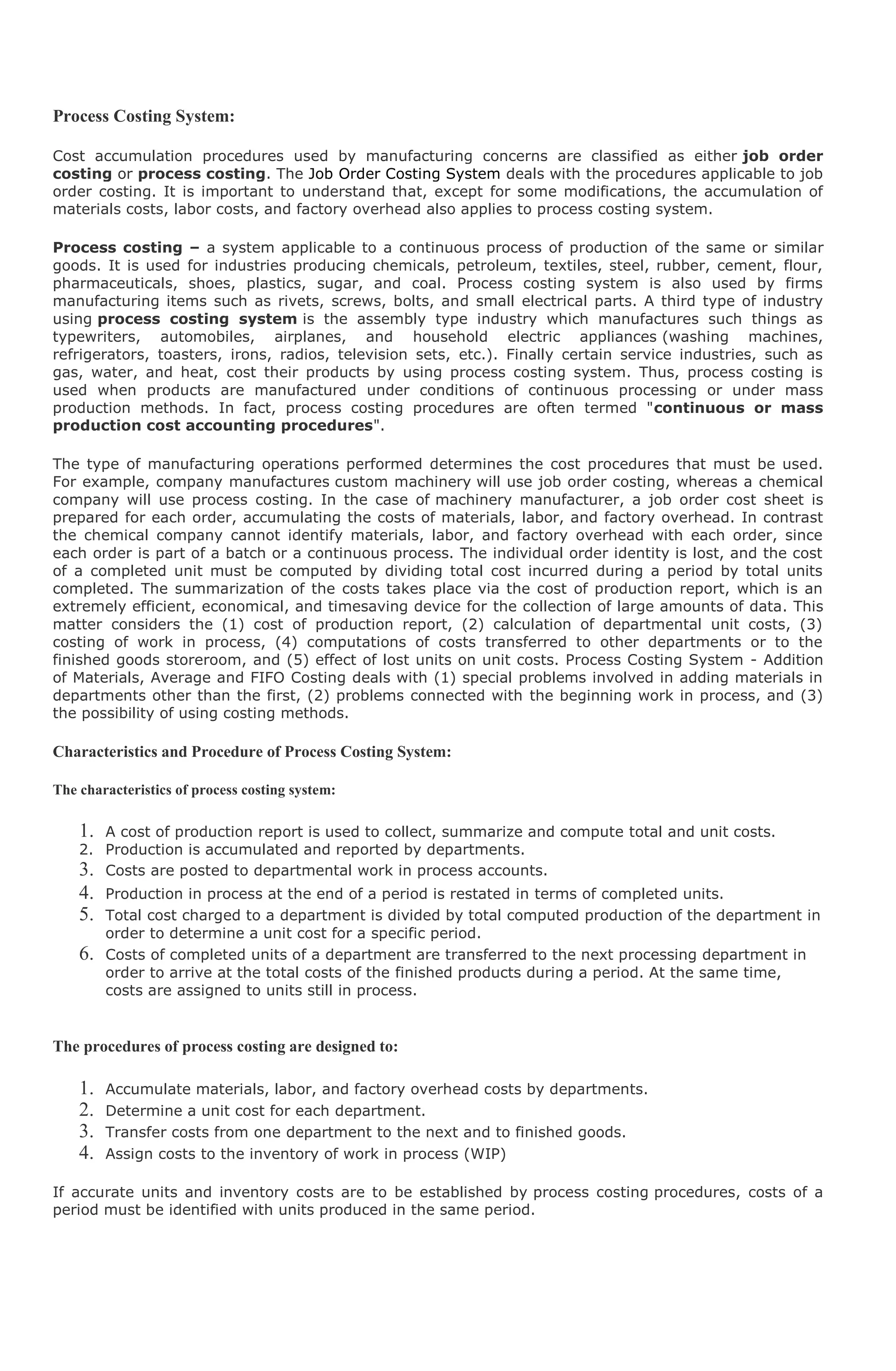

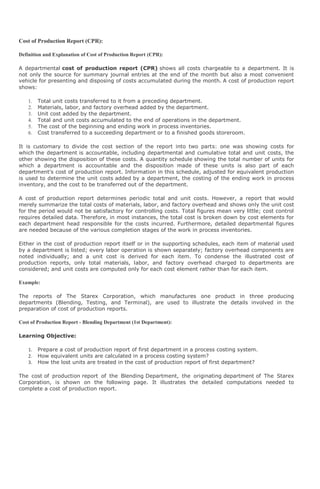

![Cost Charged To the Department: Total unit

Cost Cost

Cost from preceding department:

Transferred in during the month P77,400 P1.72

Cost added by the department:

Labor 29,140 0.91

Factory Overhead (FOH) 28,200 0.80

------- -----

Total cost added P81,840 P1.71

Adjusted for lost units 0.08*

------- ------

Total cost to be accounted for P147,510 P3.51

====== ======

Cost Accounted for as Follows:

Transferred to next department (40,000 × P3.51) P140,400

Work in process - ending inventory:

Adjusted cost from preceding department [3,000 ×

(P1.72 + P0.08)] P5,400

Labor (4,000 × 1/2 × P0.60) 910

Factory Overhead (4,000 × 1/2 × P0.60) 800 7,110

------ ------

Total cost accounted for P147,510

======

Additional Computations

Equivalent Production:

Labor and factory overhead = 40,000 + 3,000 / 3 = 41,000 units

Unit Costs:

Labor = P37,310 / 41,000 = P0.91 per unit

Factory overhead = P32,800 / 41,000 = 0.80 per unit

*Adjustment for lost units:

Method No.1: P77,400 / 43,000 = P1.80; P1.80 - P1.72 = P0.08 per unit

Method No.2: 2,000 units × P1.72 = P3,440; P3,440 / 43,000 = P0.08 per unit

Explanation:

The Blending Department (first department) transferred 45,000 units to the Testing Department, where

labor and factory overhead were added before the units were transferred to the Terminal Department](https://image.slidesharecdn.com/processcosting-111110040320-phpapp01/85/Process-costing-9-320.jpg)

![(third or final department). Costs incurred in the testing department resulted in

the additional departmental as well as cumulative unit costs.

The cost of production report of the testing department differ from that of the Blending Department

(first department) in several respects. Several additional calculations are made, for which space has

been provided on the report. The additional information deals with:

1. Cost received from the preceding department.

2. An adjustment of the preceding department's unit cost because of lost units.

3. Cost received from the preceding department to be included in the cost of ending work

in process inventory.

The quantity schedule of the Testing Department shows that the 45,000 units received from

the Blending Department (first department) were accounted for as follows:

1. 40,000 units sent to terminal department.

2. 3,000 units still in process.

3. 2,000 units lost.

An analysis of the work in process (WIP) indicates that units in process are but one third complete as to

labor and factory overhead. Unit costs, P0.91 for labor and P0.80 for factory overhead, were calculated

as follows:

Equivalent production of the testing department is 41,000 units [40,000 + P1/3 × (3,000)], the labor

unit cost is P0.91 (P37,310 / 41,000), and the factory overhead unit cost P0.80 (P32,800 / 41,000).

There is no materials unit cost, since no materials were added by the department. The department unit

cost is P1.71, the sum of the labor unit cost of P0.91 and the factory overhead unit cost of P0.80.

The testing department is responsible for the labor and factory overhead used as well as for the cost of

units received from the Blending Department (first department). This latter cost is inserted as a cost

charged to the department under the title "cost from preceding department" which is immediately

above the section of the report dealing with cost added bythe department. The cost transferred in was

P77,400, previously shown in the cost report of the Blending Department (first department) as cost

transferred out of that department by this journal entry:

Work in process - Testing department 77,400

Work in process - Blending department 77,400

The work in process account of the testing department is charged with cost received from the preceding

department and with P70,110 of departmental labor and factory overhead (FOH), a total cost of

P147,510 to be accounted for by the department.

Units Lost in the Department Subsequent to the First:

The Blending Department (first department) unit cost was P1.72 when 45,000 units were transferred to

the Testing Department. However, because 2,000 of these 45,000 units were lost during processing in

the Testing Department, the P1.72 unit cost figure no longer applies and must be adjusted. The total

cost of the units transferred remains at P77,400, but 43,000 units must now absorb this total cost,

causing an increase of P0.08 in the cost per unit due to the loss of 2,000 units in the testing

department.

The lost units cost can be computed by one of two methods.

Method No.1:

Determines a new unit cost work done in the preceding department and subtracts the preceding

departments old unit costs figure from the adjusted unit cost figure. The difference between the two

figures is the additional cost due to the lost units. P1.80 new adjusted unit cost for work done in the

preceding department is obtained by dividing the remaining good units, 43,000 (45,000 - 2,000), into

the cost transferred in, P77,400. The old unit cost figure of P1.72 is subtracted from the revised unit

cost to arrive at the adjustment of P0.08.](https://image.slidesharecdn.com/processcosting-111110040320-phpapp01/85/Process-costing-10-320.jpg)

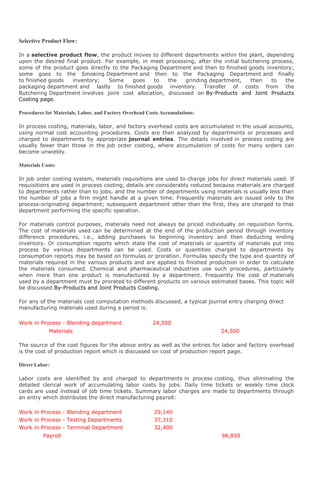

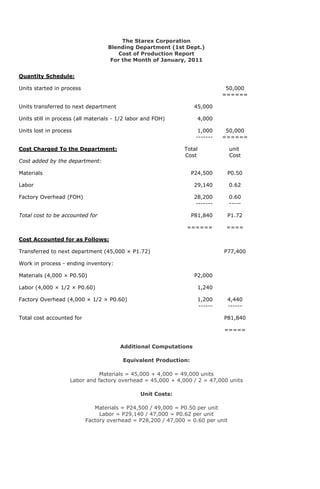

![Cost Accounted for as Follows:

Transferred to next department [(40,000 × P140,720

P3.51+P0.167)]*

Work in process - ending inventory:

From preceding department (3,000 × P1.72) P5,160

Labor (3,000 × 1/3 × P0.87) 870

Factory Overhead (3,000 × 1/2 × P0.76) 760 6,790

------ ------

Total cost accounted for P147,510

======

Additional Computations:

Equivalent Production:

Labor and factory overhead = 40,000 + 3,000 / 3 + 2,000 lost units = 41,000 units

Unit Costs:

Labor = P37,310 / 43,000 = P0.87 per unit

Factory overhead = P32,800 / 43,000 = P0.76 per unit

Lost unit cost = P3.35 × 2,000 units = P6,700 + 40,000 units P0.1675 per unit to be

added to P3.35 to make the transfer cost P3.5175.

*40,000 units P3.5175 = P140,700. To avoid a decimal discrepancy, the cost transferred

is computed: P147,510 - P6,790 = P140,720.

A comparison of the differences between the two cost of production reports for the testing departments

as to amounts for costs of units transferred and work in process inventory is shown below the

production report. Not the offsetting increases and decreases.

In this illustration, the assumption has been made that the lost units, identified at the end of the

process, were complete as to all costs. In sum companies, members of the quality control or inspection

departments make production checks prior to the end of the process. Such a procedure uncovers lost

units that are not complete when the loss is incurred or the spoilage discovered and yet the loss may

pertain only to units completed and not to units still in process. In such a case the lost units should be

adjusted for their equivalent stage of completion. For example, 2,000 units lost at the 90% stage of

conversion would appear as 1,800 equivalent units with regard to labor and factory overhead costs.

Normal Vs Abnormal Loss of units:

Units are lost through evaporation, shrinkage, substandard yields, spoiled work, poor work man ship, or

inefficient equipment. In many instances the nature of operations makes certain losses normal or

unavoidable, because they are considered with in normal tolerance limits for human and machine

errors. The cost of these normally lost units does not appear as a separate item of cost but is spread

over the remaining good units.

A different situation is created by abnormal or avoidable spoilage or losses that are not expected to

arise under normal, efficient operating conditions. The cost of such abnormal spoilage or losses is

charged either to factory overhead as shown below, thereby appearing as an additional unfavorable

able factory overhead variance, or directly to a current period expense account and reported as a

separate item in the cost of goods sold statement.

Factory Overhead Control 6,700

Work in process - Testing Department 6,700

(lost units)](https://image.slidesharecdn.com/processcosting-111110040320-phpapp01/85/Process-costing-12-320.jpg)

![The cost of production report would show the abnormal spoilage or loss as follows:

Transferred to next department (40,000 units × P3.35) ..............P134,020*

Transferred to factory overhead [40,000 units × P0.1675) or

(2,000 lost units × P3.35)].......................................................6,700

*40,000 units × P3.35 = P134,000. To avoid decimal discrepancy, the cost transferred is computed:

P147,510 - P6,790 ending inventory - P6,700 = P134,020

If the lost units were only partially complete, equivalent production calculations should consider their

stage of completion when lost or spoiled, and the costing of the abnormal loss should be weighted

accordingly. If one part of the loss is normal and another abnormal, each portion must be treated in

accordance with the above discussion. The critical factor in distinguishing between normal and

abnormal spoilage or loss is the degree of controllability. Normal or unavoidable spoilage or loss is

produced by the process under efficient operating conditions, referred to as uncontrollable. Abnormal or

avoidable spoilage or loss is considered unnecessary, because the conditions resulting in the loss are

controllable. For this reason, within the limits set by the state of the art of production, the difference is

a short-run condition; in the long run, management should adjust and control all factors of production

and eliminate all abnormal conditions.

The cost of production report at the beginning of this page shows a total cost of P147,510 to be

accounted for by the Testing department. The department completed and transferred 40,000 units to

the Terminal Department (third or final department) at a cost of P140,000 (40,000 × P3.51). The

remaining cost is assigned to the work in process inventory. This balance is broken down by the various

costs in process. When computing the cost of the ending work in process inventory of any department

subsequent to the first, costs received from the preceding departments must be included.

The 3,000 units still in process, completed by the Blending Department (first department) at a unit cost

of P1.72, were later adjusted by P0.08 (to P1.80) because of the loss of some of the units transferred.

Therefore, the Blending Department's (first department) cost of the 3,000 units still in process is

P5,400 figure is not broken down further , since such information is not pertinent to the Testing

Department's operations. However, the amount is listed separately in the cost of production report,

because it is part of the Testing Department's ending work in process inventory.

Materials (if any), labor, and factory overhead (FOH) added by a department are costed separately in

order to arrive at total work in process (WIP). In the testing department, no materials were added to

the units received; thus, the ending inventory shows no materials in the process. However, labor and

factory overhead costs were incurred. The work in process analysis stated that labor and factory

overhead used on the units in process were sufficient to complete 1,000 units. The cost of labor in

process is P910 (1,000 × P0.91) and factory overhead is process is P800 (1,000 × P0.80). The total cost

of the 3,000 units in process is P7,110 (P5,400 + P910 + P800). This cost, added to that transferred to

the Terminal Department (third or final department), P140,400, accounts for the total cost of P147,510

charged to the Testing Department.

Cost of Production Report - Terminal Department (3rd - Final Department):

The cost of production report of 3rd and final department is illustrated below:

The Starex Corporation

Terminal Department (3rd Dept.)

Cost of Production Report

For the Month of January, 2011

Quantity Schedule:

Units received from the preceding department 40,000

======

Units transferred to finished goods storeroom 35,000

Units still in process (1/4 labor and FOH) 4,000

Units lost in process 1,000 40,000

======

Cost Charged To the Department: Total unit

Cost Cost

Cost from preceding department:

Transferred in during the month P140,400 P3.51](https://image.slidesharecdn.com/processcosting-111110040320-phpapp01/85/Process-costing-13-320.jpg)

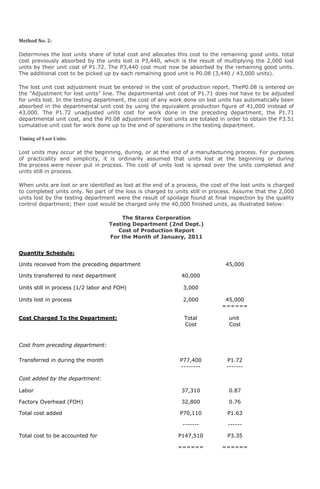

![Cost added by the department:

Labor 32,400 0.90

Factory Overhead (FOH) 19,800 0.55

------- -----

Total cost added P52,500 P1.45

Adjusted for lost units 0.09*

------- ------

Total cost to be accounted for P192,600 P5.05

====== ======

Cost Accounted for as Follows:

Transferred to finished goods storeroom (35,000 × P176,750

P5.05)

Work in process - ending inventory:

Adjusted cost from preceding department [4,000 ×

(P3.51 + P0.09)] P14,400

Labor (4,000 × 1/4 × P0.90) 900

Factory Overhead (4,000 × 1/4 × P0.55) 550 15,850

------ ------

Total cost accounted for P192,600

======

Additional Computations:

Equivalent Production:

Labor and factory overhead = 35,000 + 4,000 / 4 = 36,000 units

Unit Costs:

Labor = P32,400 / 36,000 = P0.90 per unit

Factory overhead = P19,800 / 36,000 = 0.55 per unit

*Adjustment for lost units:

Method No.1: P140,400 / 39,000 = P3.60; P3.60 - P3.51 = P0.09 per unit

Method No.2: 1,000 units × P3.51 = P3,510; P3,510 / 39,000 = P0.09 per unit

Explanation:

Total and unit cost figures were derived by using procedures discussed for the cost of production report

of the Testing Department. The work completed is transferred to thefinished goods storeroom; thus,

the title "Transferred to finished goods storeroom" is used in place of the title "Transferred to

next department." Cost charged to the Terminal Departmentcome from the payroll distribution and the

department's expense analysis sheet. The journal entry transferring costs from the

Testing Department follows:

Work in process - Terminal Department 140,000

Work in process - Testing Department 140,000

The entry to transfer finished units to the finished goods storeroom is presented below:

Finished Goods 176,750

Work in process - Terminal Department 176,750

Combined Cost of Production Report (CPR) - Process Costing:

The three cost of production reports for the Starex Corpora have been discussed and computed

separately.](https://image.slidesharecdn.com/processcosting-111110040320-phpapp01/85/Process-costing-14-320.jpg)

![These reports would most likely be consolidated in a single report summarizing manufacturing

operations of the firm for a specific period. Such a report, as illustrated below, should be reviewed in

order to observe the interrelationship of the various department reports.

The Starex Corporation

Cost of Production Report

All Producing Departments

For the Month of January, 2011

Quantity Schedule: Blending Testing Terminal

1stDepartment 2ndDepartment 3rdDepartment

Units started in process 50,000

======

Units received from the 45,000 40,000

preceding department ====== ======

Units transferred to next department 45,000 40,000

Units transferred to finished goods 35,000

storeroom

Units still in process 4,000 3,000 4,000

Units lost in process 1,000 2,000 1,000

------- ------- -------

50,000 45,000 40,000

====== ====== ======

Cost Charged To the Department: Total unit Total unit Total cost unit

Cost cost cost Cost Cost

Cost from preceding department:

Transferred in during the month P77,400 P1.72 P140,400 P3.51

-------- ----- -------- -----

Cost added by the department:

Materials P24,500 P.50

Labor 29,140 .62 P37,310 P.91 P32,400 P.90

Factory Overhead (FOH) 28,200 .60 32,800 .80 19,800 .55

------- ---- ----- ---- ------- ----

Total cost added P81,840 P1.72 P70,110 P1.71 P52,200 P1.45

Adjusted for lost units P.08 P.09

------- ---- ------- ----- -------- ----

Total cost to be accounted for P81,840 P1.72 P147,510 P3.51 P192,600 P5.05

====== === ====== === ====== ===

Cost Accounted for as Follows:

Transferred to next department P77,400 P140,400

Transferred to finished goods P176,750

storeroom (35,000 × P5.05)

Work in process - ending inventory:

Adjusted cost from

preceding department [4,000 × (P3.51 P5,400 P14,400

+ P0.09)]

Materials P2,000

Labor (4,000 × 1/4 × P0.90) 1,240 910 900

Factory Overhead (4,000 × 1/4 × 1,200 800 550

P0.55) ------ ------ ------

4,440 7,110 15,850

-------- ------ --------

Total cost accounted for P81,840 P147,510 P192,600

====== ====== ======](https://image.slidesharecdn.com/processcosting-111110040320-phpapp01/85/Process-costing-15-320.jpg)