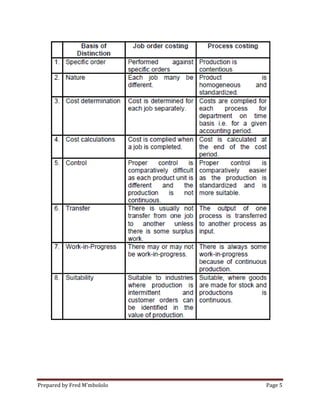

The document discusses process costing, which is used to assign costs to standardized products produced continuously. It describes the five steps of process costing: 1) analyzing physical unit flow, 2) computing equivalent units, 3) computing equivalent unit costs, 4) summarizing total costs, and 5) assigning costs to completed units and work-in-process. The two main methods are weighted average and FIFO. Examples show journal entries to record costs and calculations to assign costs using equivalent units and cost per equivalent unit.