Download to read offline

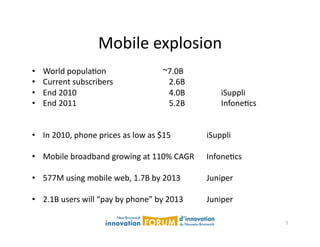

This document provides a summary of the mobile app market and trends: - Mobile phones have become the 7th mass media platform due to their widespread adoption globally, with over 5 billion subscribers expected by 2011. - Smartphones now run full operating systems and allow third party applications to be downloaded, making the software more important than the hardware. - The mobile app market is dominated by Apple's iOS and Google's Android operating systems, though RIM, Microsoft and others still have shares of the market. - Constant hardware innovation and the emergence of new manufacturers from Asia is driving the development of new types of powerful yet affordable smartphones.

![Pharma times mobile[2]](https://cdn.slidesharecdn.com/ss_thumbnails/pharmatimesmobile2-120522030647-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)