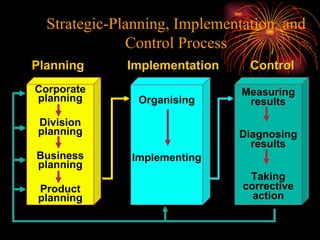

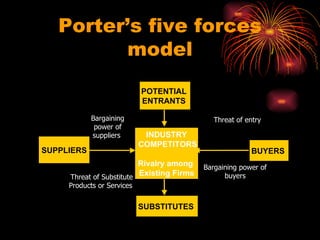

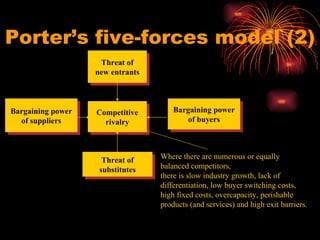

This document provides an overview of strategic planning and marketing concepts. It discusses various strategic planning frameworks including the BCG matrix, GE/McKinsey multifactor matrix, and Ansoff's growth vector matrix. It also covers topics like corporate, business, and marketing strategy, strategic-planning processes, Porter's five forces model, and approaches to turnaround strategies, restructuring, and entry strategies like acquisitions and joint ventures.

![Hofers Method Of Business Portfolio Analysis[1].Ppt2003](https://cdn.slidesharecdn.com/ss_thumbnails/hofersmethodofbusinessportfolioanalysis1-ppt2003-091006110519-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Ge Final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/ge-final11249-thumbnail.jpg?width=640&height=640&fit=bounds)