1.value5.00 pointsExercise 6-4 Income effects of inventory .docxfredellsberry

1.

value:

5.00 points

Exercise 6-4 Income effects of inventory methods L.O. A1

Park Company reported the following March purchases and sales data for its only product.

Date

Activities

Units Acquired at Cost

Units Sold at Retail

Mar.

1

Beginning inventory

150

units

@ $7.00

=

$

1,050

Mar.

10

Sales

90

units

@$15

Mar.

20

Purchase

220

units

@ $6.00

=

1,320

Mar.

25

Sales

145

units

@$15

Mar.

30

Purchase

90

units

@ $5.00

=

450

Totals

460

units

$

2,820

235

units

Park uses a perpetual inventory system. For specific identification, ending inventory consists of 225 units, where 90 are from the March 30 purchase, 80 are from the March 20 purchase, and 55 are from beginning inventory.

1.

Complete comparative income statements for the month of March for Park Company for the four inventory methods. Assume expenses are $1,600, and that the applicable income tax rate is 30%.

(

Round per unit costs to three decimal places.

Round your answers to the nearest dollar amounts. Input all amounts as positive values. Omit the "$" sign in your response.)

PARK COMPANY

Income Statements

For Month Ended March 31

Specific

Identification

Weighted

Average

FIFO

LIFO

Sales

$ [removed]

$ [removed]

$ [removed]

$ [removed]

Cost of goods sold

[removed]

[removed]

[removed]

[removed]

Gross profit

[removed]

[removed]

[removed]

[removed]

Expenses

[removed]

[removed]

[removed]

[removed]

Income before taxes

[removed]

[removed]

[removed]

[removed]

Income tax expense

[removed]

[removed]

[removed]

[removed]

Net income

$ [removed]

$ [removed]

$ [removed]

$ [removed]

2.

Which method yields the highest net income?

[removed]

FIFO

[removed]

Weighted average

[removed]

Specific identification

[removed]

LIFO

3.

Does net income using weighted average fall between that using FIFO and LIFO?

[removed]

Yes

[removed]

No

4.

If costs were rising instead of falling, which method would yield the highest net income?

[removed]

Weighted average

[removed]

Specific identification

[removed]

LIFO

[removed]

FIFO

Problem 6-1A Alternative cost flows-perpetual L.O. P1

[The following information applies to the questions displayed below.]

Anthony Company uses a perpetual inventory system. It entered into the following purchases and sales transactions for March.

Date

Activities

Units Acquired at Cost

Units Sold at Retail

Mar.

1

Beginning inventory

50

units

@ $50/unit

Mar.

5

Purchase

200

units

@ $55/unit

Mar.

9

Sales

210

units

@ $85/unit

Mar.

18

Purchase

60

units

@ $60/unit

Mar.

25

Purchase

100

units

@ $62/unit

Mar.

29

Sales

80

units

@ $95/unit

Totals

410

units

290

units

references

2.

value:

3.00 points

Problem 6-1A Part 1

Required:

1.

Compute cost of goods available f.

Laker Company reported the following January purchases and sales data.pdfmohammedfootwear

Laker Company reported the following January purchases and sales data for its only product.

Activities Units Acquired at Cost Date Jan. 1Beginning inventory Jan. 10 Sales Jan. 20 Purchase

Jan. 25 Sales Jan. 30 Purchase 220 units 170 units 370 units $14.50$ 3,190 $13.502,295

$13.004,810 Units sold at Retalil 170 units $23.50 200 units @ $23.50 370 units Totals 760 units

$10,295 The company uses a periodic inventory system. For specific identification, ending

inventory consists of 390 units, where 370 are from the January 30 beginning inventory value:

2.00 points Required 1. Complete the table to determine the cost assigned to ending inventory

and to cost of goods sold using specific identification. (Round cost per uni Specific Identification

Cost of Goods Available for Sale Cost of Goods Sold Ending Inventory per Cost ofof units Cost

per Ending # of units | Cost per Cost of Goods Availableforl#of units cost unit Goods Sold in

ending inventory sold unit Inventory Sale Beginning inventory Purchases Jan. 20 Jan. 30 Total

Solution

Answers

FIFO,

LIFO,

Specific Identification,

Weighted Average.

FIFO

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 14.50

$ 3,190.00

220

$ 14.50

$ 3,190.00

0

$ 14.50

$ -

Purchases:

20-Jan

170

$ 13.50

$ 2,295.00

150

$ 13.50

$ 2,025.00

20

$ 13.50

$ 270.00

30-Jan

370

$ 13.00

$ 4,810.00

0

$ 13.00

$ -

370

$ 13.00

$ 4,810.00

TOTAL

760

$ 10,295.00

370

$ 5,215.00

390

$ 5,080.00

LIFO

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 14.50

$ 3,190.00

$ 14.50

$ -

220

$ 14.50

$ 3,190.00

Purchases:

20-Jan

170

$ 13.50

$ 2,295.00

$ 13.50

$ -

170

$ 13.50

$ 2,295.00

30-Jan

370

$ 13.00

$ 4,810.00

370

$ 13.00

$ 4,810.00

0

$ 13.00

$ -

TOTAL

760

$ 10,295.00

370

$ 4,810.00

390

$ 5,485.00

Specific Identification

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 14.50

$ 3,190.00

200

$ 14.50

$ 2,900.00

20

$ 14.50

$ 290.00

Purchases:

20-Jan

170

$ 13.50

$ 2,295.00

170

$ 13.50

$ 2,295.00

0

$ 13.50

$ -

30-Jan

370

$ 13.00

$ 4,810.00

0

$ 13.00

$ -

370

$ 13.00

$ 4,810.00

TOTAL

760

$ 10,295.00

370

$ 5,195.00

390

$ 5,100.00

Average Method

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 14.50

$ 3,190.00

Purchases:

20-Jan

170

$ 13.50

$ 2,295.00

30-Jan

370

$ 13.00

$ 4,810.00

TOTAL

760

13.55

$ 10,295.00

370

13.55

$ 5,013.50

390

$ 13.55

$ 5,284.50

FIFO

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 1.

1.value5.00 pointsExercise 6-4 Income effects of inventory .docxfredellsberry

1.

value:

5.00 points

Exercise 6-4 Income effects of inventory methods L.O. A1

Park Company reported the following March purchases and sales data for its only product.

Date

Activities

Units Acquired at Cost

Units Sold at Retail

Mar.

1

Beginning inventory

150

units

@ $7.00

=

$

1,050

Mar.

10

Sales

90

units

@$15

Mar.

20

Purchase

220

units

@ $6.00

=

1,320

Mar.

25

Sales

145

units

@$15

Mar.

30

Purchase

90

units

@ $5.00

=

450

Totals

460

units

$

2,820

235

units

Park uses a perpetual inventory system. For specific identification, ending inventory consists of 225 units, where 90 are from the March 30 purchase, 80 are from the March 20 purchase, and 55 are from beginning inventory.

1.

Complete comparative income statements for the month of March for Park Company for the four inventory methods. Assume expenses are $1,600, and that the applicable income tax rate is 30%.

(

Round per unit costs to three decimal places.

Round your answers to the nearest dollar amounts. Input all amounts as positive values. Omit the "$" sign in your response.)

PARK COMPANY

Income Statements

For Month Ended March 31

Specific

Identification

Weighted

Average

FIFO

LIFO

Sales

$ [removed]

$ [removed]

$ [removed]

$ [removed]

Cost of goods sold

[removed]

[removed]

[removed]

[removed]

Gross profit

[removed]

[removed]

[removed]

[removed]

Expenses

[removed]

[removed]

[removed]

[removed]

Income before taxes

[removed]

[removed]

[removed]

[removed]

Income tax expense

[removed]

[removed]

[removed]

[removed]

Net income

$ [removed]

$ [removed]

$ [removed]

$ [removed]

2.

Which method yields the highest net income?

[removed]

FIFO

[removed]

Weighted average

[removed]

Specific identification

[removed]

LIFO

3.

Does net income using weighted average fall between that using FIFO and LIFO?

[removed]

Yes

[removed]

No

4.

If costs were rising instead of falling, which method would yield the highest net income?

[removed]

Weighted average

[removed]

Specific identification

[removed]

LIFO

[removed]

FIFO

Problem 6-1A Alternative cost flows-perpetual L.O. P1

[The following information applies to the questions displayed below.]

Anthony Company uses a perpetual inventory system. It entered into the following purchases and sales transactions for March.

Date

Activities

Units Acquired at Cost

Units Sold at Retail

Mar.

1

Beginning inventory

50

units

@ $50/unit

Mar.

5

Purchase

200

units

@ $55/unit

Mar.

9

Sales

210

units

@ $85/unit

Mar.

18

Purchase

60

units

@ $60/unit

Mar.

25

Purchase

100

units

@ $62/unit

Mar.

29

Sales

80

units

@ $95/unit

Totals

410

units

290

units

references

2.

value:

3.00 points

Problem 6-1A Part 1

Required:

1.

Compute cost of goods available f.

Laker Company reported the following January purchases and sales data.pdfmohammedfootwear

Laker Company reported the following January purchases and sales data for its only product.

Activities Units Acquired at Cost Date Jan. 1Beginning inventory Jan. 10 Sales Jan. 20 Purchase

Jan. 25 Sales Jan. 30 Purchase 220 units 170 units 370 units $14.50$ 3,190 $13.502,295

$13.004,810 Units sold at Retalil 170 units $23.50 200 units @ $23.50 370 units Totals 760 units

$10,295 The company uses a periodic inventory system. For specific identification, ending

inventory consists of 390 units, where 370 are from the January 30 beginning inventory value:

2.00 points Required 1. Complete the table to determine the cost assigned to ending inventory

and to cost of goods sold using specific identification. (Round cost per uni Specific Identification

Cost of Goods Available for Sale Cost of Goods Sold Ending Inventory per Cost ofof units Cost

per Ending # of units | Cost per Cost of Goods Availableforl#of units cost unit Goods Sold in

ending inventory sold unit Inventory Sale Beginning inventory Purchases Jan. 20 Jan. 30 Total

Solution

Answers

FIFO,

LIFO,

Specific Identification,

Weighted Average.

FIFO

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 14.50

$ 3,190.00

220

$ 14.50

$ 3,190.00

0

$ 14.50

$ -

Purchases:

20-Jan

170

$ 13.50

$ 2,295.00

150

$ 13.50

$ 2,025.00

20

$ 13.50

$ 270.00

30-Jan

370

$ 13.00

$ 4,810.00

0

$ 13.00

$ -

370

$ 13.00

$ 4,810.00

TOTAL

760

$ 10,295.00

370

$ 5,215.00

390

$ 5,080.00

LIFO

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 14.50

$ 3,190.00

$ 14.50

$ -

220

$ 14.50

$ 3,190.00

Purchases:

20-Jan

170

$ 13.50

$ 2,295.00

$ 13.50

$ -

170

$ 13.50

$ 2,295.00

30-Jan

370

$ 13.00

$ 4,810.00

370

$ 13.00

$ 4,810.00

0

$ 13.00

$ -

TOTAL

760

$ 10,295.00

370

$ 4,810.00

390

$ 5,485.00

Specific Identification

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 14.50

$ 3,190.00

200

$ 14.50

$ 2,900.00

20

$ 14.50

$ 290.00

Purchases:

20-Jan

170

$ 13.50

$ 2,295.00

170

$ 13.50

$ 2,295.00

0

$ 13.50

$ -

30-Jan

370

$ 13.00

$ 4,810.00

0

$ 13.00

$ -

370

$ 13.00

$ 4,810.00

TOTAL

760

$ 10,295.00

370

$ 5,195.00

390

$ 5,100.00

Average Method

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 14.50

$ 3,190.00

Purchases:

20-Jan

170

$ 13.50

$ 2,295.00

30-Jan

370

$ 13.00

$ 4,810.00

TOTAL

760

13.55

$ 10,295.00

370

13.55

$ 5,013.50

390

$ 13.55

$ 5,284.50

FIFO

Cost of Goods available for sale

Cost of Goods Sold

Ending Inventory

Units

Cost/unit

COG for sale

Units sold

Cost/unit

COGS

Units

Cost/unit

Ending inventory

Beginning Inventory

220

$ 1.

I apologize this 1 question has numerous parts. I didnt want to s.pdfjeetumordhani

I apologize: this 1 question has numerous parts. I didn\'t want to split it up in to separate

questions and confuse others. Selected year-end financial statements of Cabot Corporation

follow. (All sales were on credit; selected balanoe sheet amounts at December 31, 2014, were

inventory, S53,900; total assets, $199,400; common stock, 588,000; and retained earnings,

344,392.) CABOT CORPORATION Income Statement For Year Ended December 31, 2015

Sales Cost of goods sold S453,600 298,850 Gross profit Operating expenses Interest expense

158,750 98,800 4,600 Income before taxes Income taxes 53,350 21,492 Net income S 31,858

CABOT CORPORATION Balance Sheet December 31, 2015 Assets Cash Short-term

investments Accounts receivable, net Notes receivable (trade) S 18,000 9,200 32,200 000 38,150

2,800 151,300 Liabilities and Equity Accounts payable Accrued Income taxes payable Long-

term note payable, secured S 17,500 4,800 4,700 wages payable 5, Prepaid expenses Plant assets,

net by mortgage on plant assets Common stod Retained earnings 83,400 88,000 76,250 Total

assets S254,650 Total liabilities and equity S254,650 These are short-term notes receivable

arising from customer (trade) sales. Required: Compute the following: (1) current ratio, (2) acid-

test ratio, (3) days sales uncollected, (4) inventory turnover, (5) days\' sales in inventory, (8)

debt-to-equity ratio, (7) times interest earned, (8) profit margin ratio, (9) total asset turnover, (10)

return on total assets, and (11) return on common stockholders\' equity Do not round

intermediate calculations.) Choose Numerator: | Choose Denominator: | = Current Ratio Current

ratio 2015 to 1

Solution

Answer to Part 1.

Current Ratio = Current Assets / Current Liabilities

Current Assets = Cash + Short Term Investments + Accounts Receivable, net + Notes

Receivable (Trade) + Merchandise Inventory + Prepaid Expenses

Current Assets = $16,000 + $9,200 + $32,200 + $5,000 + $38,150 + $2,800

Current Assets = $103,350

Current Liabilities = Accounts Payable + Accrued Wages Payable + Income Taxes Payable

Current Liabilities = $17,500 + $4,800 + $4,700

Current Liabilities = $27,000

Current Ratio = 103,350 / 27,000

Current Ratio = 3.83 to 1

Answer to Part 2.

Acid-Test Ratio = Quick Assets / Current Liabilities

Quick Assets = Current Assets – Merchandise Inventory – Prepaid Expenses

Quick Assets = $103,350 - $38,150 - $2,800

Quick Assets = $62,400

Acid-Test Ratio = 62,400 /27,000

Acid-Test Ratio = 2.31 to 1

Answer to Part 3.

Days Collected Sales = Current Receivable / Net Sales * 365

Current Receivable = $32,200 + $5,000 = $37,200

Days Collected Sales = 37,200 / 453,600 * 100

Days Collected Sales = 29.93 days

Answer to Part 4.

Inventory Turnover Ratio = Cost of goods sold / Average Inventory

Average Inventory = (38,150 + 53,900) / 2

Average Inventory = $46,025

Inventory Turnover Ratio = 296,850 / 46,025

Inventory Turnover Ratio = 6.45 times

Answer to Part 5.

Days’ Sales in Inventory = Average Inventory / Cost of Goods Sol.

“You can download this product from SlideTeam.net”

Select our professionally designed Finance Budgeting PowerPoint Presentation Slides to improve your profits, reduce costs, and increase return on investments. Keep track of your expenses and revenues with the help of our content ready budget forecast presentation deck. The topic-specific actual vs budget variance PowerPoint complete deck contains a set of self-explanatory templates such as actual cost vs budget, month-wise forecasting, overhead cost analysis, quarterly budget analysis, variance analysis, actual vs target variance, budget vs plan vs forecast, forecast, and projection, etc. Creating and monitoring a budget can keep your business profitable and successful. Manage your finances effectively using the ready-to-use budget projection PPT slides. Incorporate the professional-looking financial forecasting PPT visuals to showcase steps of developing and planning a budget. Furthermore, the visually appealing corporate budgeting and forecasting PowerPoint templates are also helpful in creating your financial plans. Thus, download the budget variance analysis PowerPoint presentation now and engage your viewers. A hearty chuckle is good for health. Our Finance Budgeting Powerpoint Presentation Slides are firm believers of the fact. https://bit.ly/3ETzaSC

This complete deck can be used to present to your team.It has PPT slides on various topics highlighting all the core areas of your business needs. This complete deck focuses on Finance Budgeting Powerpoint Presentation Slides and has professionally designed templates with suitable visuals and appropriate content. This deck consists of total of twentyone slides. All the slides are completely customizable for your convenience. You can change the colour, text and font size of these templates. You can add or delete the content if needed. Get access to this professionally designed complete presentation by clicking the download button below.

Montoure Company uses a perpetual inventory system. It entered into .pdfmccarthygaussvanst87

Montoure Company uses a perpetual inventory system. It entered into the following calendar-

year purchases and sales transactions. (For specific identification, units sold consist of 600 units

from beginning inventory, 300 from the February 10 purchase, 200 from the March 13 purchase,

50 from the August 21 purchase, and 250 from the September 5 purchase.) Date Activities Units

Acquired at Cost Units Sold at Retail Jan. 1 Beginning inventory 600 units @ $45.00 per unit

Feb. 10 Purchase 400 units @ $42.00 per unit Mar. 13 Purchase 200 units @ $27.00 per unit

Mar. 15 Sales 800 units @ $75.00 per unit Aug. 21 Purchase 100 units @ $50.00 per unit Sept. 5

Purchase 500 units @ $46.00 per unit Sept. 10 Sales 600 units @ $75.00 per unit Totals 1,800

units 1,400 units Required 1.Compute cost of goods available for sale and the number of units

available for sale. 2.Compute the number of units in ending inventory. 3.Compute the cost

assigned to ending inventory using (a) FIFO, (b) LIFO, (c) weighted average, and (d) specific

identification. (Round all amounts to cents.) Check (3) Ending inventory: FIFO, $18,400; LIFO,

$18,000; WA, $17,760 4.Compute gross profit earned by the company for each of the four

costing methods in part 3. (4) LIFO gross profit, $45,800

Solution

Answer

Purchase

Units

Rate

Amount

Feb-10

400

42

16800

Mar-13

200

27

5400

Aug-21

100

50

5000

Sep-05

500

46

23000

Total

1200

50200

Sales

Units

Rate

Amount

Mar-15

800

75

60000

Sep-10

600

75

45000

0

Total

1400

105000

Cost of Goods Available for Sale = Opening Inventory + Purchases

= 27000 + 50200 = $77,200

Closing Inventory = Opening Inventory + Purchased units - Sold Units

= 600 + 1200 – 1400 = 400 units

First, FIFO

FIFO

Opening + Purchases

Cost of Goods Sold

Closing Inventory

Opening Jan 1

600

45.00

27000

600

45.00

27000.00

Feb 10 Purchase

400

42.00

16800

600

45.00

27000.00

400

42.00

16800.00

Mar 13 Purchase

200

27.00

5400

600

45.00

27000.00

400

42.00

16800.00

200

27.00

5400.00

Mar 15 Sales

600

45.00

27000

200

42.00

8400.00

200

42.00

8400

200

27.00

5400.00

Aug 21 purchased

100

50.00

5000

200

42.00

8400.00

200

27.00

5400.00

100

50.00

5000.00

Sept 5 Purchase

500

46.00

23000

200

42.00

8400.00

200

27.00

5400.00

100

50.00

5000.00

500

46.00

23000.00

Sep 10 Sales

200

42.00

8400

400

46.00

18400.00

200

27.00

5400

100

50.00

5000

100

46.00

4600

TOTAL

1800

77200

1400

58800

400

18400.00

Units

Value

Cost of Goods Sold

1400

58800

Closing Inventory

400

18400

LIFO Method

LIFO

Opening + Purchases

Cost of Goods Sold

Closing Inventory

Opening Jan 1

600

45.00

27000

600

45.00

27000.00

Feb 10 Purchase

400

42.00

16800

600

45.00

27000.00

400

42.00

16800.00

Mar 13 Purchase

200

27.00

5400

600

45.00

27000.00

400

42.00

16800.00

200

27.00

5400.00

Mar 15 Sales

200

27.00

5400

400

45.00

18000.00

400

42.00

16800

0.00

200

45.00

9000

Aug 21 purchased

100

50.00

5000

400

45.00

18000.00

100

50.00

5000.00

0.00

Sept 5 Purchase

500

46.00

23000

400

45.00

18000.00

100

50.00

5000.00

500

46.00

23000.00

Sep 10 Sales

500

46.00

23000

400

4.

Yes of course, you can easily start mining pi network coin today and sell to legit pi vendors in the United States.

Here the telegram contact of my personal vendor.

@Pi_vendor_247

#pi network #pi coins #legit #passive income

#US

Seminar: Gender Board Diversity through Ownership NetworksGRAPE

Seminar on gender diversity spillovers through ownership networks at FAME|GRAPE. Presenting novel research. Studies in economics and management using econometrics methods.

Lecture slide titled Fraud Risk Mitigation, Webinar Lecture Delivered at the Society for West African Internal Audit Practitioners (SWAIAP) on Wednesday, November 8, 2023.

how to sell pi coins effectively (from 50 - 100k pi)DOT TECH

Anywhere in the world, including Africa, America, and Europe, you can sell Pi Network Coins online and receive cash through online payment options.

Pi has not yet been launched on any exchange because we are currently using the confined Mainnet. The planned launch date for Pi is June 28, 2026.

Reselling to investors who want to hold until the mainnet launch in 2026 is currently the sole way to sell.

Consequently, right now. All you need to do is select the right pi network provider.

Who is a pi merchant?

An individual who buys coins from miners on the pi network and resells them to investors hoping to hang onto them until the mainnet is launched is known as a pi merchant.

debuts.

I'll provide you the Telegram username

@Pi_vendor_247

Abhay Bhutada Leads Poonawalla Fincorp To Record Low NPA And Unprecedented Gr...Vighnesh Shashtri

Under the leadership of Abhay Bhutada, Poonawalla Fincorp has achieved record-low Non-Performing Assets (NPA) and witnessed unprecedented growth. Bhutada's strategic vision and effective management have significantly enhanced the company's financial health, showcasing a robust performance in the financial sector. This achievement underscores the company's resilience and ability to thrive in a competitive market, setting a new benchmark for operational excellence in the industry.

The European Unemployment Puzzle: implications from population agingGRAPE

We study the link between the evolving age structure of the working population and unemployment. We build a large new Keynesian OLG model with a realistic age structure, labor market frictions, sticky prices, and aggregate shocks. Once calibrated to the European economy, we quantify the extent to which demographic changes over the last three decades have contributed to the decline of the unemployment rate. Our findings yield important implications for the future evolution of unemployment given the anticipated further aging of the working population in Europe. We also quantify the implications for optimal monetary policy: lowering inflation volatility becomes less costly in terms of GDP and unemployment volatility, which hints that optimal monetary policy may be more hawkish in an aging society. Finally, our results also propose a partial reversal of the European-US unemployment puzzle due to the fact that the share of young workers is expected to remain robust in the US.

where can I find a legit pi merchant onlineDOT TECH

Yes. This is very easy what you need is a recommendation from someone who has successfully traded pi coins before with a merchant.

Who is a pi merchant?

A pi merchant is someone who buys pi network coins and resell them to Investors looking forward to hold thousands of pi coins before the open mainnet.

I will leave the telegram contact of my personal pi merchant to trade with

@Pi_vendor_247

The secret way to sell pi coins effortlessly.DOT TECH

Well as we all know pi isn't launched yet. But you can still sell your pi coins effortlessly because some whales in China are interested in holding massive pi coins. And they are willing to pay good money for it. If you are interested in selling I will leave a contact for you. Just telegram this number below. I sold about 3000 pi coins to him and he paid me immediately.

Telegram: @Pi_vendor_247

5 Tips for Creating Standard Financial ReportsEasyReports

Well-crafted financial reports serve as vital tools for decision-making and transparency within an organization. By following the undermentioned tips, you can create standardized financial reports that effectively communicate your company's financial health and performance to stakeholders.

2. Elemental Economics - Mineral demand.pdfNeal Brewster

After this second you should be able to: Explain the main determinants of demand for any mineral product, and their relative importance; recognise and explain how demand for any product is likely to change with economic activity; recognise and explain the roles of technology and relative prices in influencing demand; be able to explain the differences between the rates of growth of demand for different products.

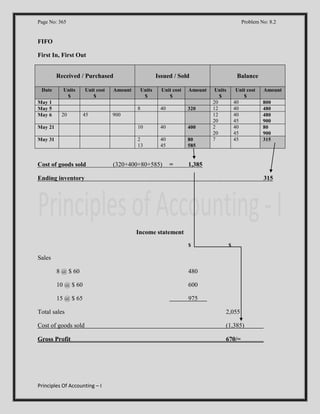

1. Page No: 365

Problem No: 8.2

FIFO

First In, First Out

Received / Purchased

Date

Unit cost

$

Amount

8

40

320

May 21

10

40

400

May 31

2

13

40

45

80

585

May 1

May 5

May 6

Units

$

20

Unit cost

$

45

Cost of goods sold

Amount

Issued / Sold

Units

$

900

(320+400+80+585)

=

Balance

Units

$

20

12

12

20

2

20

7

Unit cost

$

40

40

40

45

40

45

45

800

480

480

900

80

900

315

1,385

Ending inventory

315

Income statement

$

$

Sales

8 @ $ 60

480

10 @ $ 60

600

15 @ $ 65

975

Total sales

2,055

Cost of goods sold

(1,385)

Gross Profit

670/=

Principles Of Accounting – I

Amount

2. Page No: 365

Problem No: 8.2

LIFO

Last In, First Out

Received / Purchased

Date

Unit cost

$

Amount

8

40

320

May 21

10

45

450

May 31

10

5

45

40

450

200

May 1

May 5

May 6

Units

$

20

Unit cost

$

Issued / Sold

45

Cost of goods sold

Amount

Units

$

900

(320+450+450+200) =

Balance

Units

$

20

12

12

20

12

10

7

Unit cost

$

40

40

40

45

40

45

40

800

480

480

900

480

450

280

1,420

Ending inventory

280

Income statement

$

$

Sales

8 @ $ 60

480

10 @ $ 60

600

15 @ $ 65

975

Total sales

2,055

Cost of goods sold

(1,420)

Gross Profit

635/=

Principles Of Accounting – I

Amount

3. Page No: 365

Problem No: 8.2

W.A

Weighted Average Cost

Received / Purchased

Date

May 1

May 5

May 6

May 21

May 31

Units

$

Cost of goods sold

Amount

40

320

10

15

45

Amount

Unit cost

$

8

20

Unit cost

$

Issued / Sold

Units

$

43.125

43.125

431.125

646.875

900

Balance

Units

$

20

12

32

22

7

Unit cost

$

40

40

43.125

43.123

43.125

301.875

Income statement

$

$

Sales

8 @ $ 60

480

10 @ $ 60

600

15 @ $ 65

975

2,055

Cost of goods sold

(1,398.125)

Gross Profit

656.875/=

Principles Of Accounting – I

800

480

1,380

948.75

301.875

(320+431.125+646.875) = 1,398.125

Ending inventory

Total sales

Amount