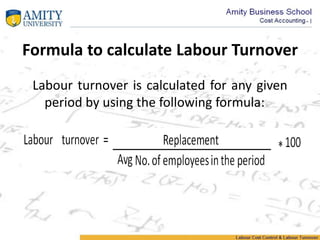

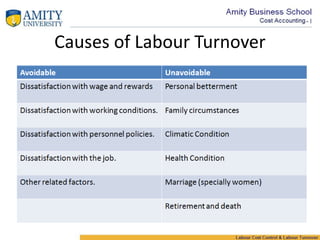

This document discusses labor costs and ways to control them. It defines direct and indirect labor costs and notes that labor costs are a significant percentage of total production costs. It emphasizes controlling costs through optimal productivity rather than reducing costs. Specific elements of labor costs mentioned include basic wages, overtime premiums, idle time, and labor turnover. The document then lists some methods for controlling labor costs, such as reviewing compensation levels, reducing employee turnover, automating tasks, eliminating redundancy, and monitoring and controlling labor turnover rates through calculating formulas and addressing causes and effects.