Downloaded 37 times

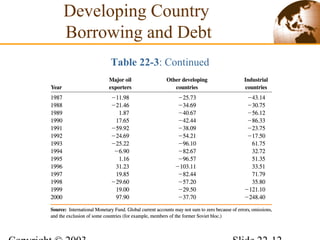

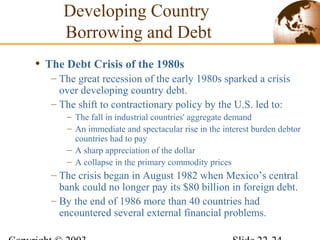

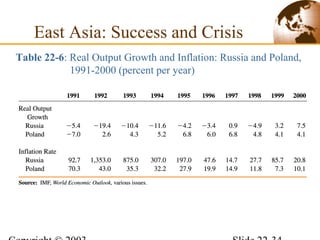

This document provides an overview of developing countries, including their economic growth, structural features, borrowing and debt issues, and experiences with financial crises. Some key points discussed include: - Developing countries have shown uneven economic convergence and growth rates compared to industrialized nations. - Common structural features of developing economies include government intervention, inflation, weak institutions, and reliance on commodity exports. - Developing country borrowing led to debt crises when borrowers defaulted due to factors like high interest rates and falling commodity prices. - Latin American countries experienced high inflation and debt crises in the 1980s while pursuing different stabilization strategies. - East Asian countries grew rapidly due to high savings and investment but