Downloaded 706 times

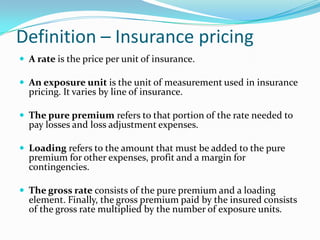

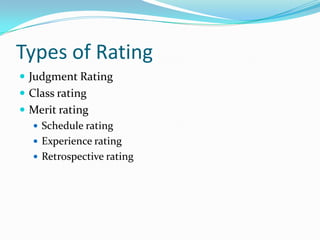

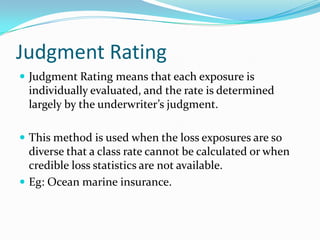

The document defines key terms related to insurance pricing such as rate, exposure unit, pure premium, and loading. It describes the objectives of insurance pricing from both regulatory and business perspectives. The types of rating discussed include judgment rating, class rating, merit rating, schedule rating, experience rating, and retrospective rating. Class rating and two methods for determining class rates, pure premium and loss ratio, are explained in detail with examples. Merit rating adjusts class rates based on individual risk characteristics and loss experience.