Downloaded 209 times

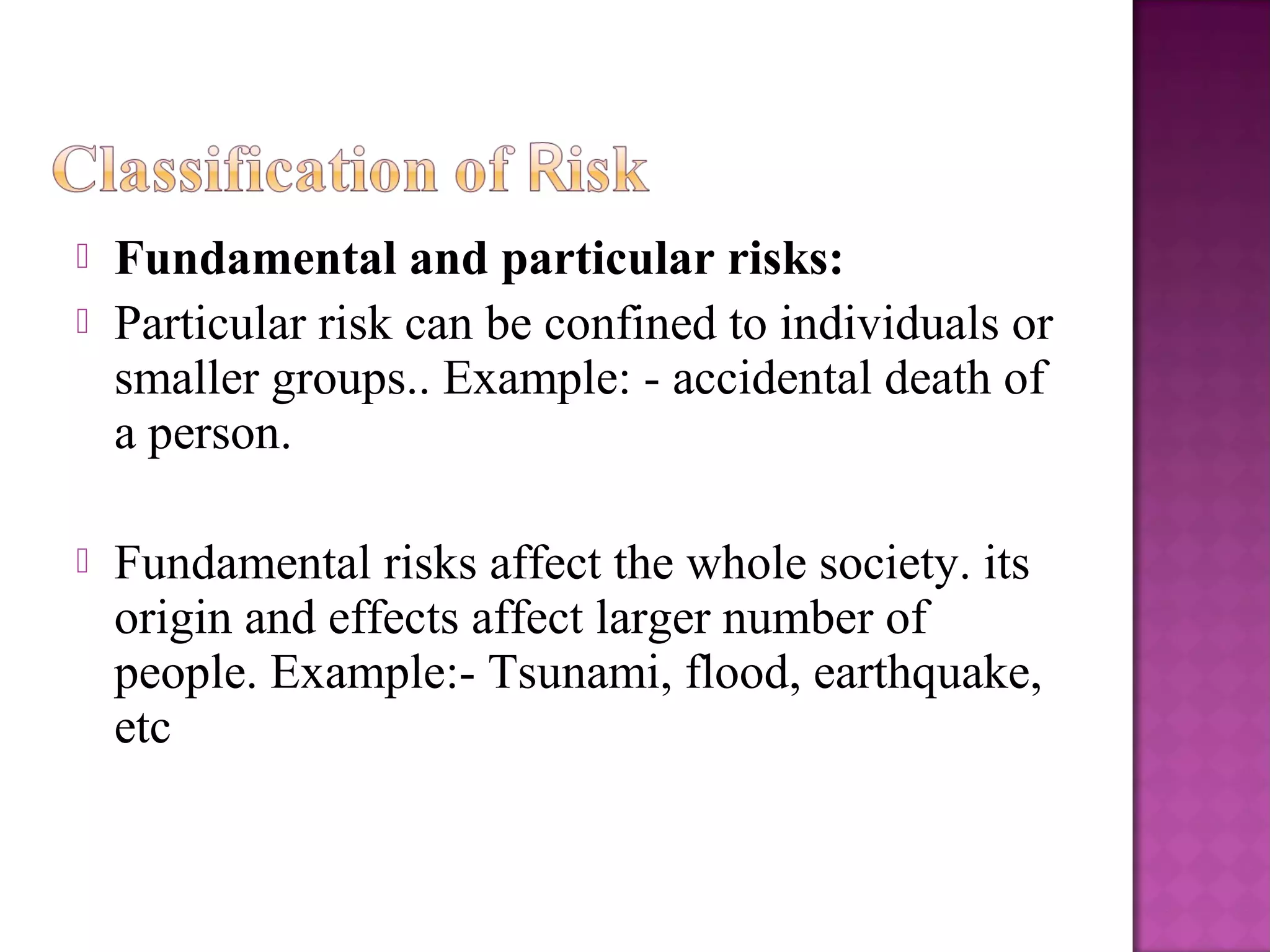

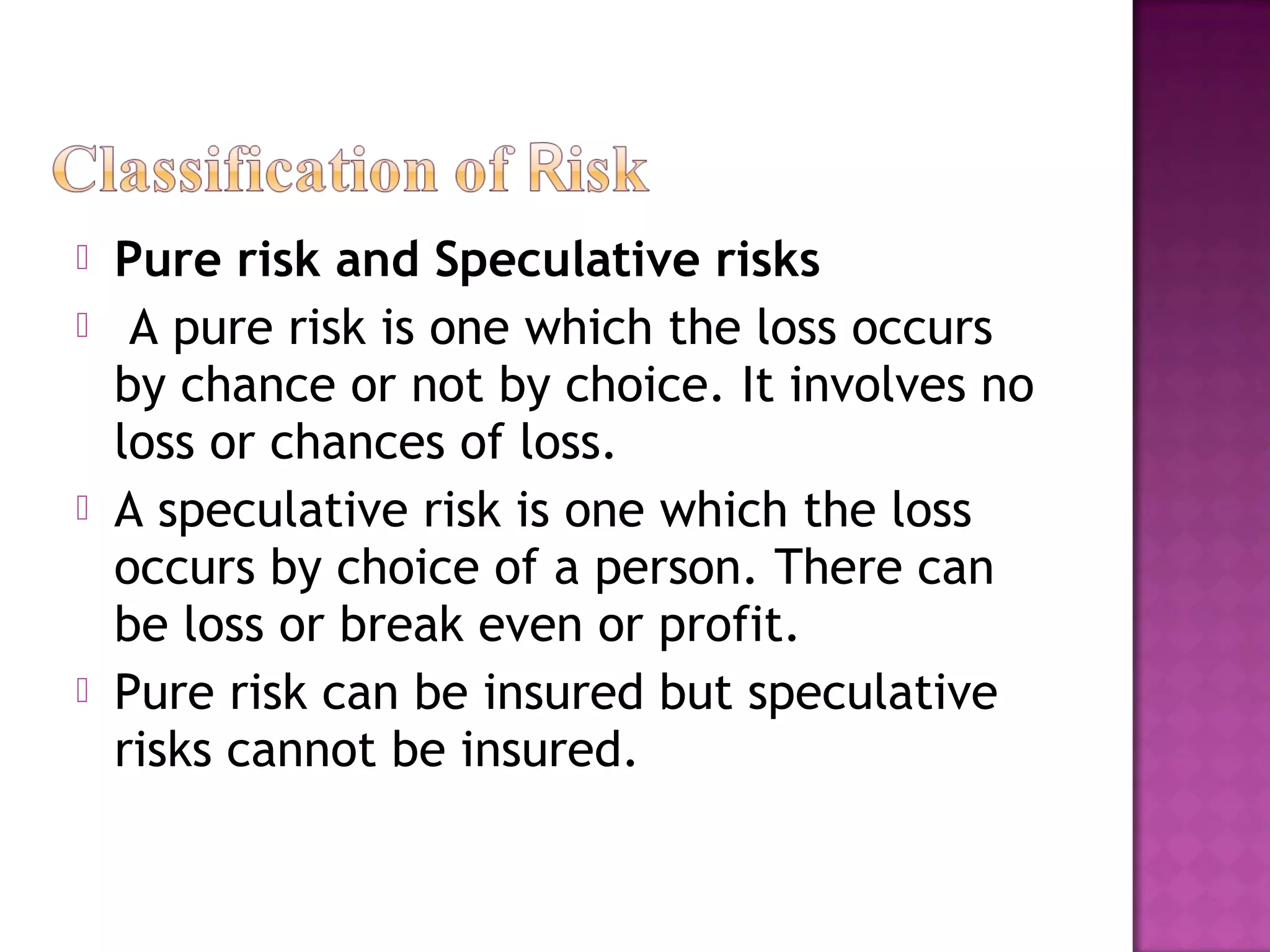

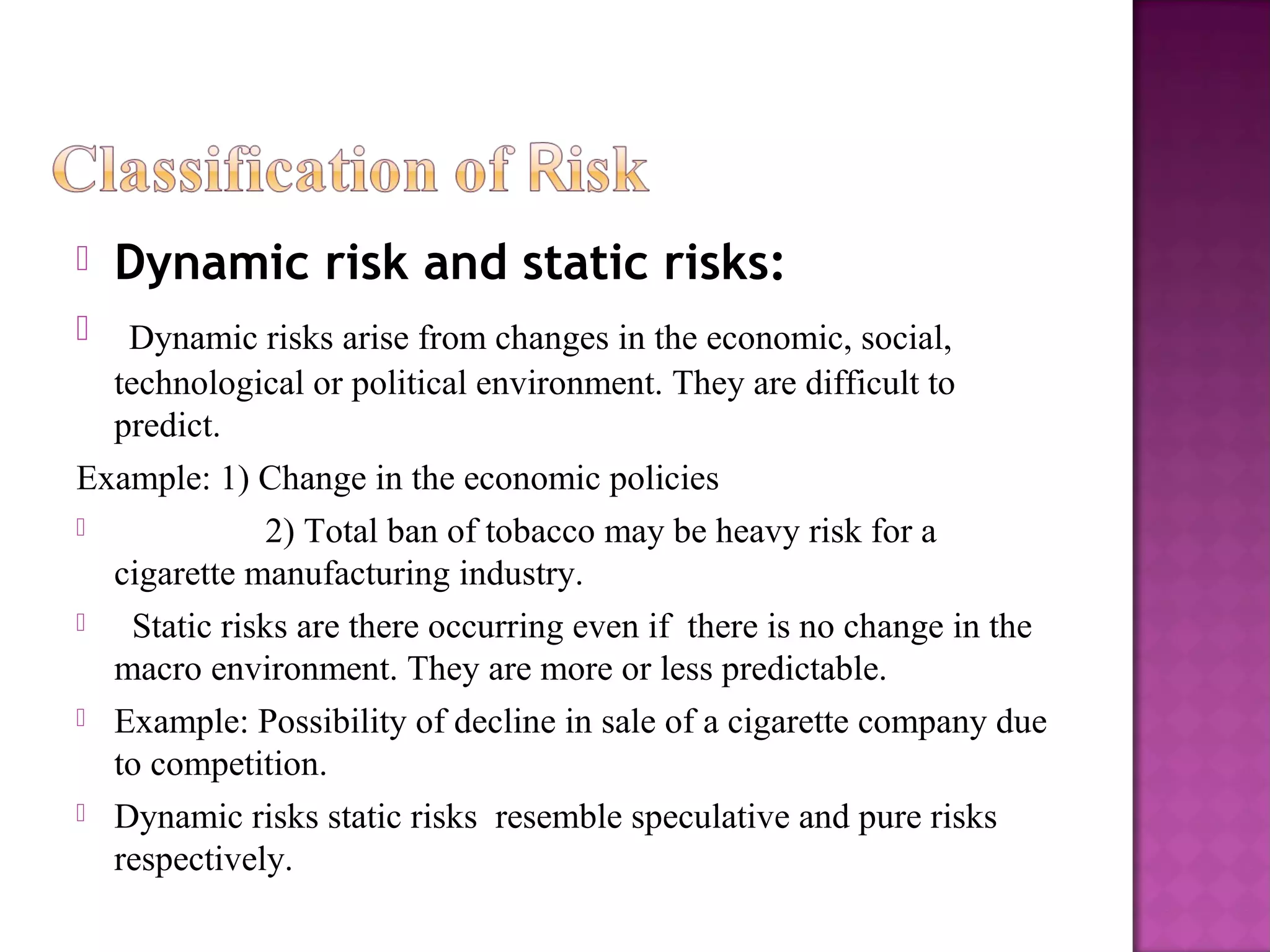

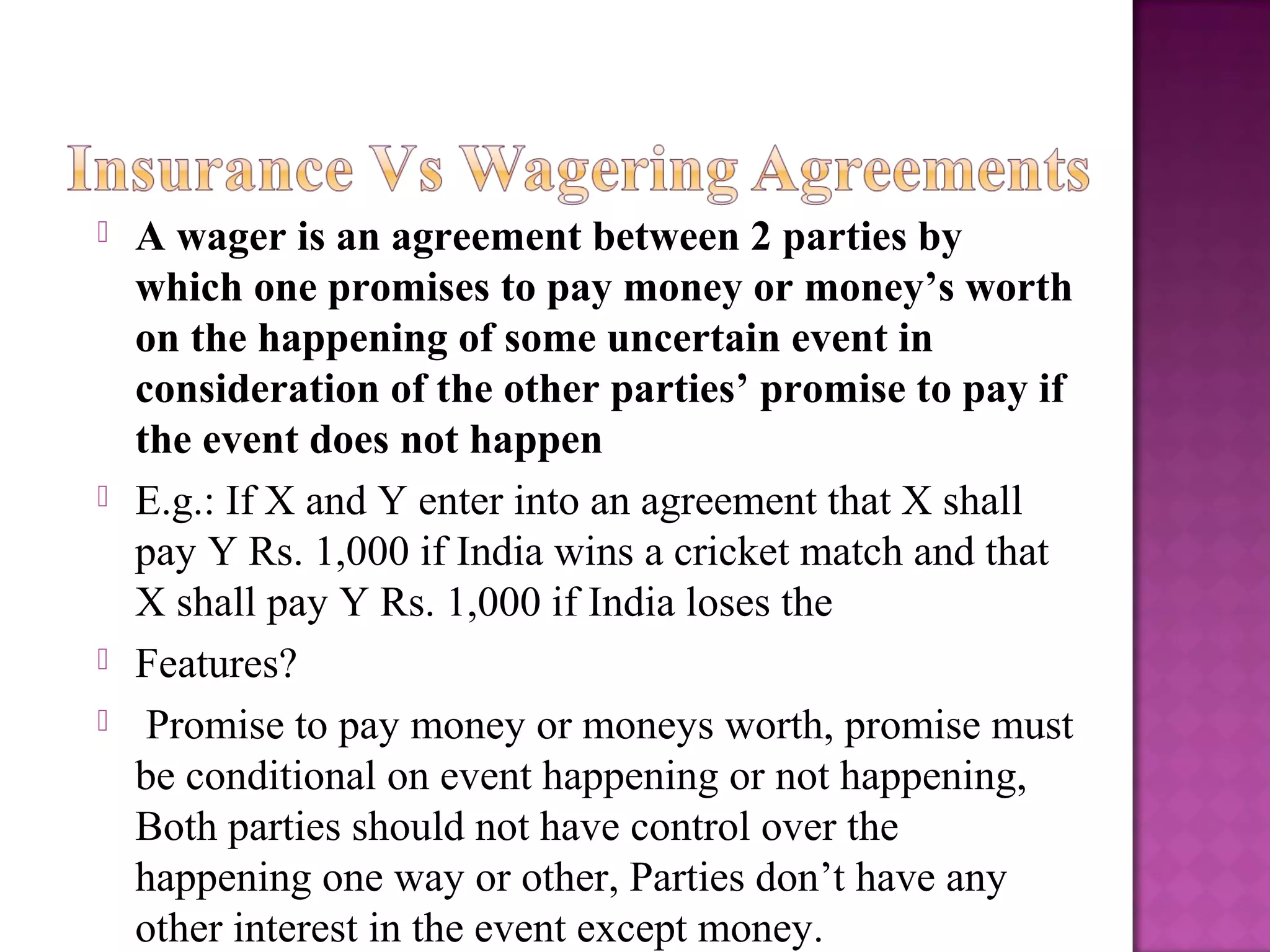

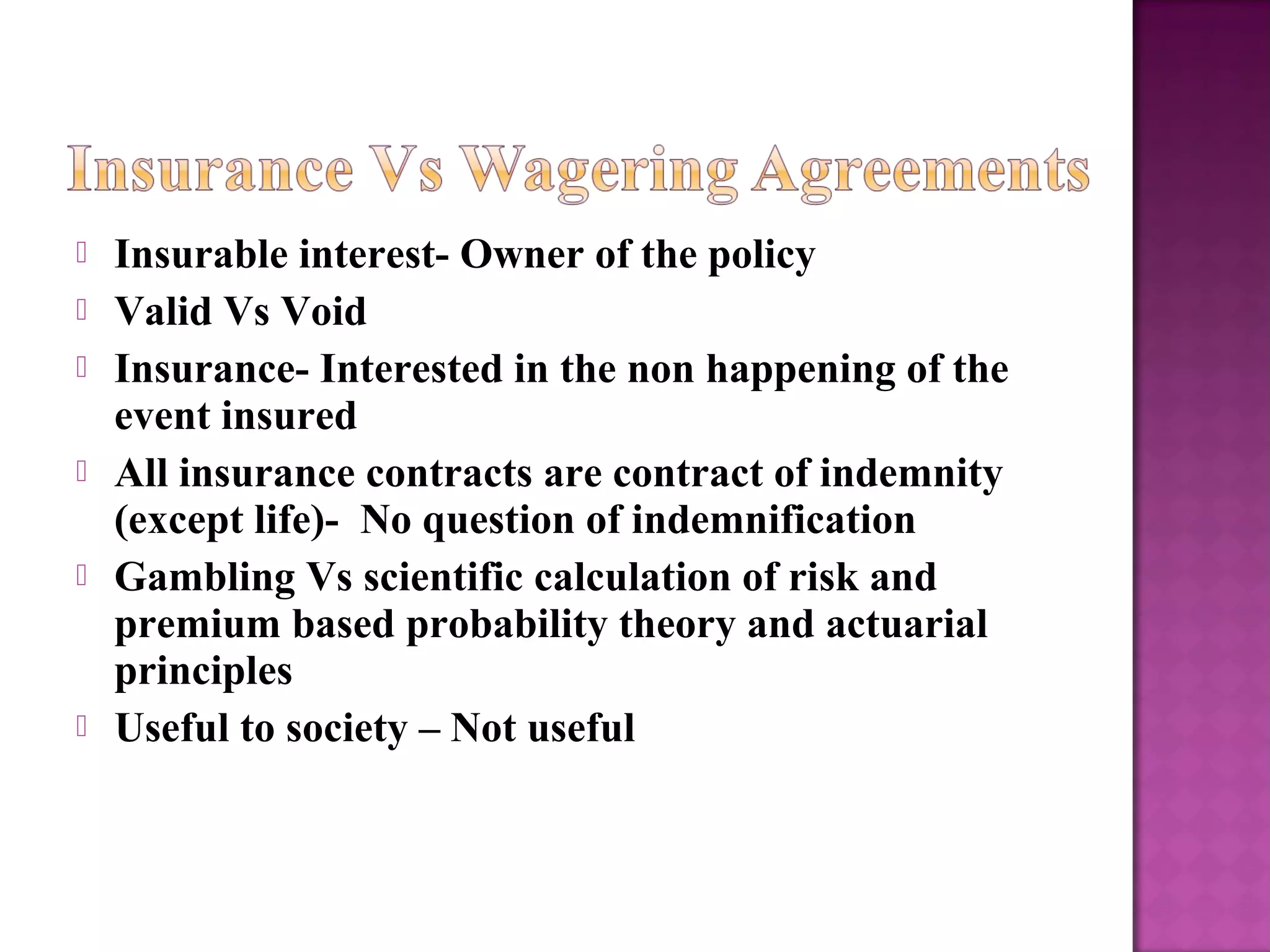

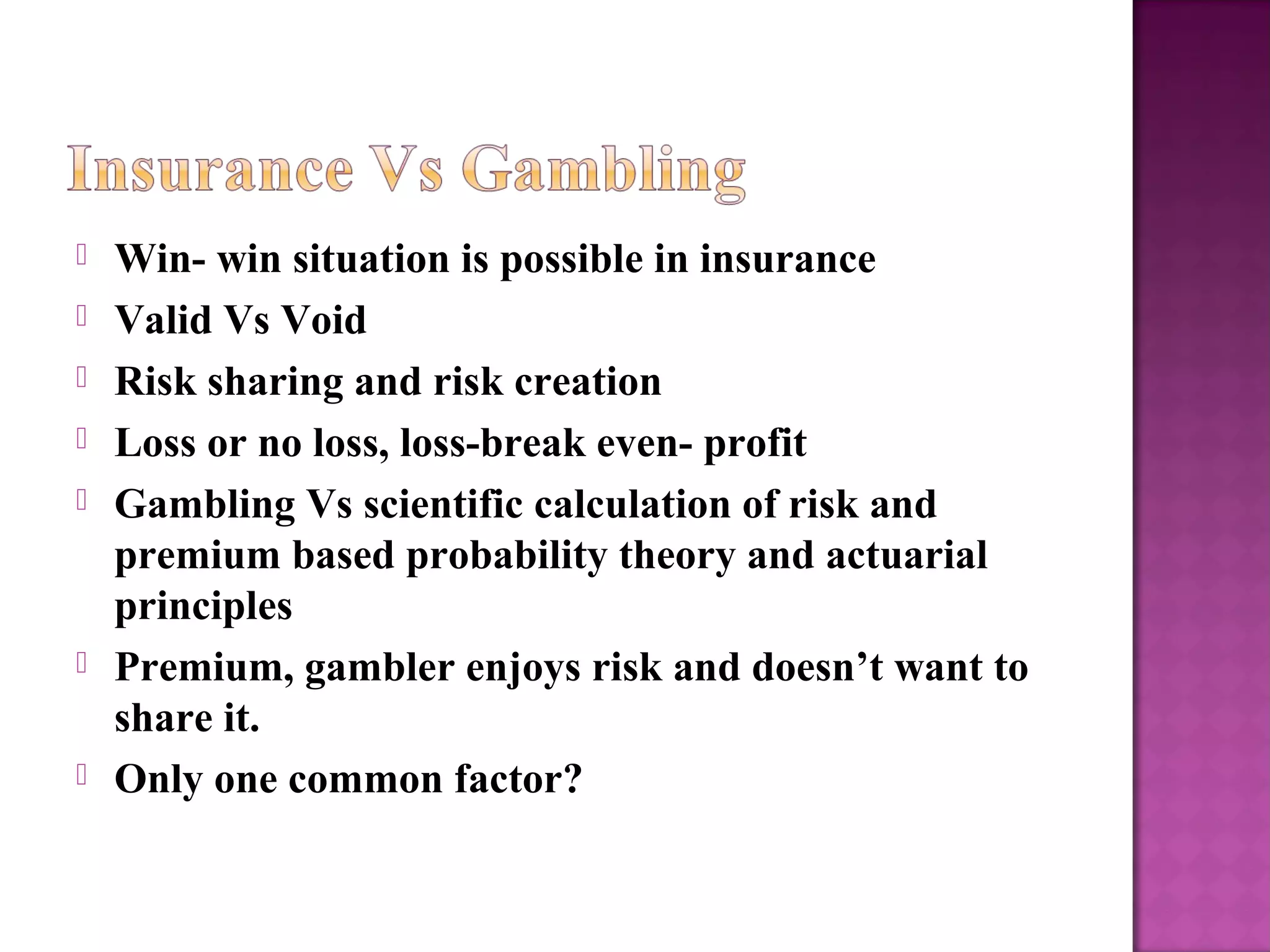

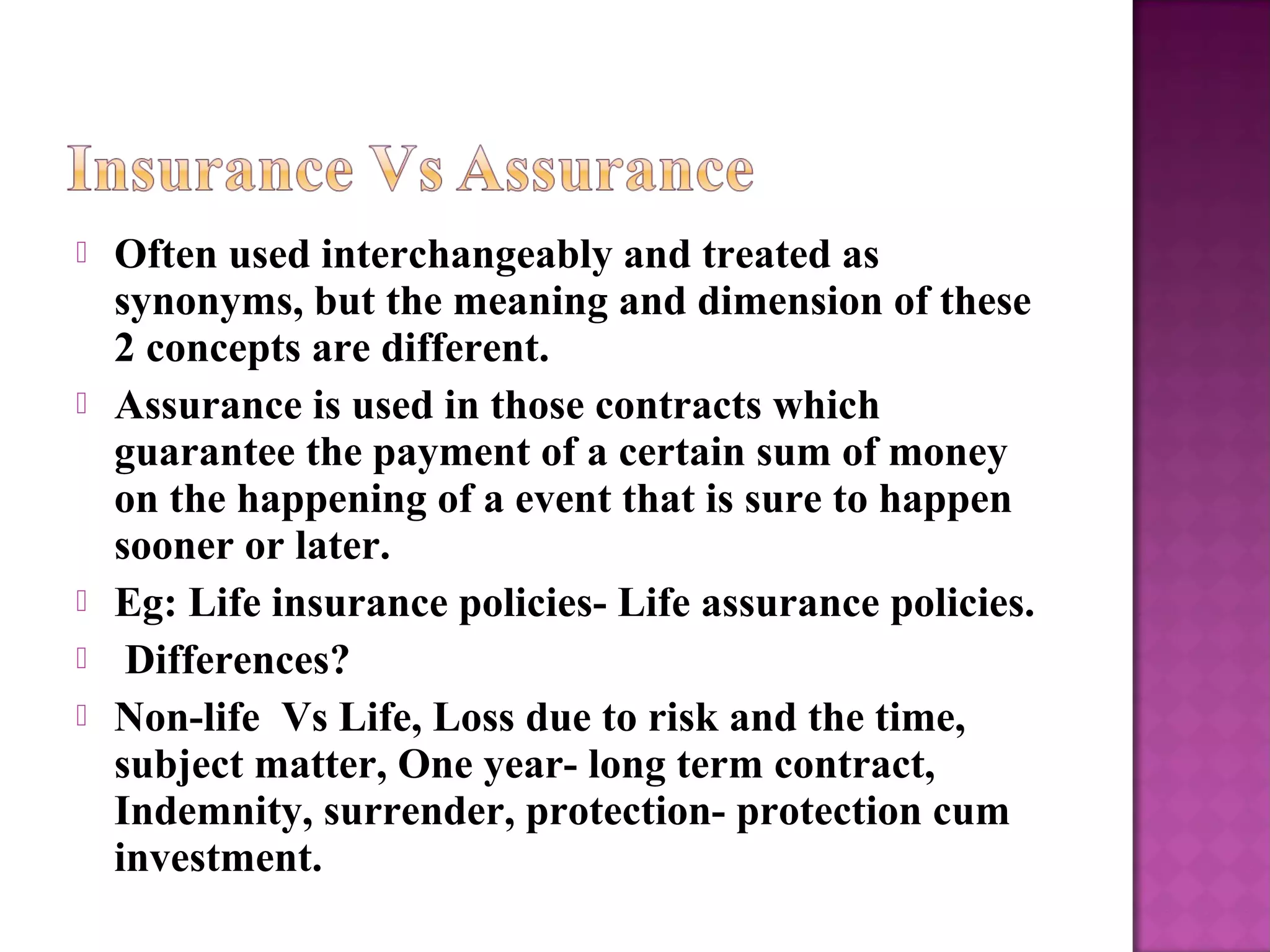

The document discusses the key differences between risk and peril, and defines various types of risks such as financial vs non-financial, quantifiable vs non-quantifiable, fundamental vs particular, pure vs speculative, and dynamic vs static risks. It also explains the differences between insurance, gambling, and wagering contracts. Insurance involves scientifically calculating risks and premiums based on probability, while gambling and wagers involve uncontrolled events with the goal of profit rather than risk sharing. Finally, it discusses the differences between insurance and assurance, noting that assurance guarantees payment on an event that is sure to happen, like death in a life insurance policy.

![Chapter 1[definition and nature of insurance]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter1definitionandnatureofinsurance-150912031826-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)